The opening of Jewel this year failed to act as a catalyst for OUE Hospitality Trust. I am expecting it to attract more tourists which can possibly give the hospitality segment a boost, but it didn’t.

OUE Hospitality Trust makes up 4% of my stock portfolio. OUE Hospitality Trust has announced their 2Q2019 financial results on 6th August 2019. Net Property Income (NPI) was lower by S$1.2 million mainly due to lower gross revenue from both the hospitality and retail segments. Distribution Per Unit was 1.06 cents, 9.4% lower y-o-y, mainly due to lower income and higher interest expense.

The current gearing ratio stood at 38.5% which I felt that it is not on the high side, but neither is it safe haven. The good thing is that there is no refinancing required until December 2020.

2Q2019 Financial Results

| 2Q2019 (S$’mil) |

2Q2018 (S$’mil) |

Change | |

| Gross Revenue | 29.4 | 30.7 | (4.4)% |

| Net Property Income | 25.3 | 26.5 | (4.5)% |

| Distributable Income | 19.4 | 21.3 | (8.6)% |

| Distribution Per Unit (“DPU”) (cents) | 1.06 | 1.17 | (9.4)% |

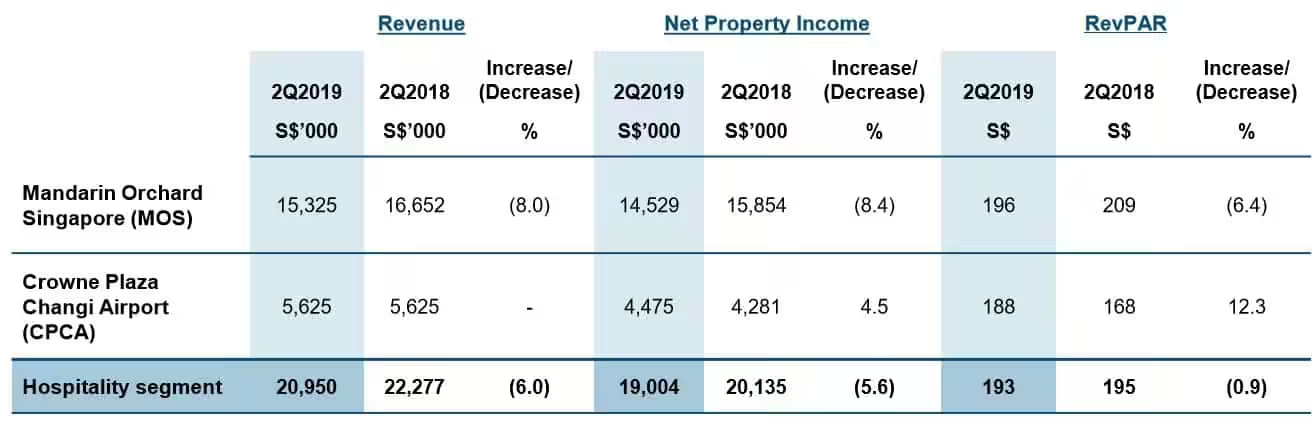

From the below financial results from the Hospitality segment, we can see that Revenue declined by 6%, Net Property Income declined by 5.6% and RevPAR fell slightly by 0.9%.

Mandarin Orchard Singapore (MOS) achieved a lower RevPAR of S$196 due to lower average room rates and lower demand from transient and corporate segments, as well as lower F&B sales.

Crowne Plaza Changi Airport (CPCA) continued to show improvement in its operating performance. In 2Q2019, Crowne Plaza Changi Airport (CPCA) recorded a 12.3% y-o-y increase in RevPAR to S$188. Minimum rent was received for the period for CPCA as the master lease income was below the minimum rent.

Conclusion

I like OUE Hospitality Trust for its quality assets (Mandarin Orchard Singapore, Crowne Plaza Changi Airport). However, OUE Hospitality Trust seems to have fell below my expectations on how it should have performed. The overall hospitality sentiments in Singapore seems weak and I am expecting OUE Hospitality Trust to end FY2019 with weak financial results. This is the only REIT that I have in my stock portfolio that is in the hospitality sector. Unless I find another alternative REIT, I shall be keeping OUE Hospitality Trust in my stock portfolio for diversification.