CapitaLand Investment (CLI) has released its CapitaLand Investment 1Q 2026 Business Update, and it paints a picture of a manager that is leaning hard into fee-based, capital-light growth while navigating a still-fragile macro backdrop. For me personally, CLI currently makes up 1.92% of my stock portfolio in terms of amount invested. With the share price closing at SGD 2.64 on 5 May 2026, I think it is worth taking a closer look at whether the latest numbers and strategic moves justify adding, holding, or trimming at this level.

In this CapitaLand Investment 1Q 2026 Business Update, we will explore the key highlights and insights to understand the company’s current standing.

The first quarter of 2026 has not been an easy environment for real estate or capital markets in general. Geopolitical developments, interest rate uncertainty and selective capital allocation have all weighed on investor sentiment. Yet CLI’s update shows that the group is still executing, still raising and deploying capital, and still growing its recurring fee base. That combination of resilience and discipline is exactly what I look for in a long-term compounder in the real assets space.

The CapitaLand Investment 1Q 2026 Business Update underscores the importance of strategic agility in today’s market.

Fee-related revenue continues to anchor the story

According to the latest CapitaLand Investment 1Q 2026 Business Update, fee-related revenue continues to be a core focus.

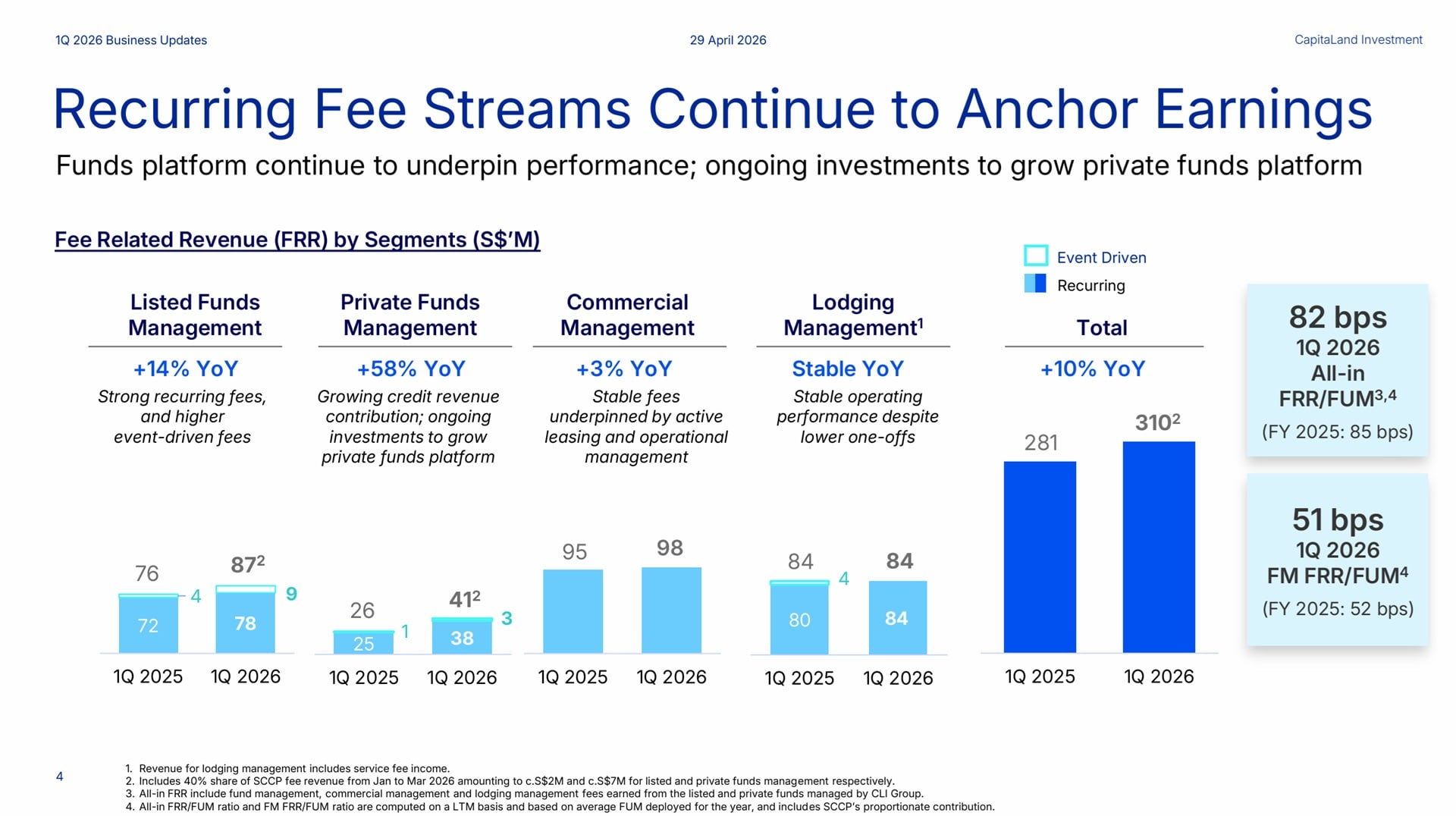

One of the clearest positives from the update is the strength of fee-related revenue (FRR). CLI reported fee-related revenue of S$310 million in 1Q 2026, up 10% year-on-year, underpinned by strong growth from its listed funds platform. This reflects the structural shift in CLI’s business model toward recurring, capital-light income streams that are less sensitive to property valuation swings.

This performance is a central theme in the CapitaLand Investment 1Q 2026 Business Update, highlighting operational strength.

The listed funds management segment delivered healthy growth, supported by both recurring management fees and higher event-driven fees. Private funds management did even better, with a sharp year-on-year increase driven by growing contributions from real estate credit strategies and ongoing investments to scale the platform. Commercial management fees were stable with modest growth, reflecting steady leasing and operational performance across CLI’s office, retail and business park assets. Lodging management revenue held steady as well, with solid operating performance offsetting lower one-off items.

Taken together, these fee streams form a diversified and resilient earnings base. In a world where asset values can be volatile and transaction volumes can slow, having a broad platform of recurring fees from listed funds, private funds, commercial management and lodging is a major strategic advantage.

Revenue mix and capital efficiency reflect strategic priorities

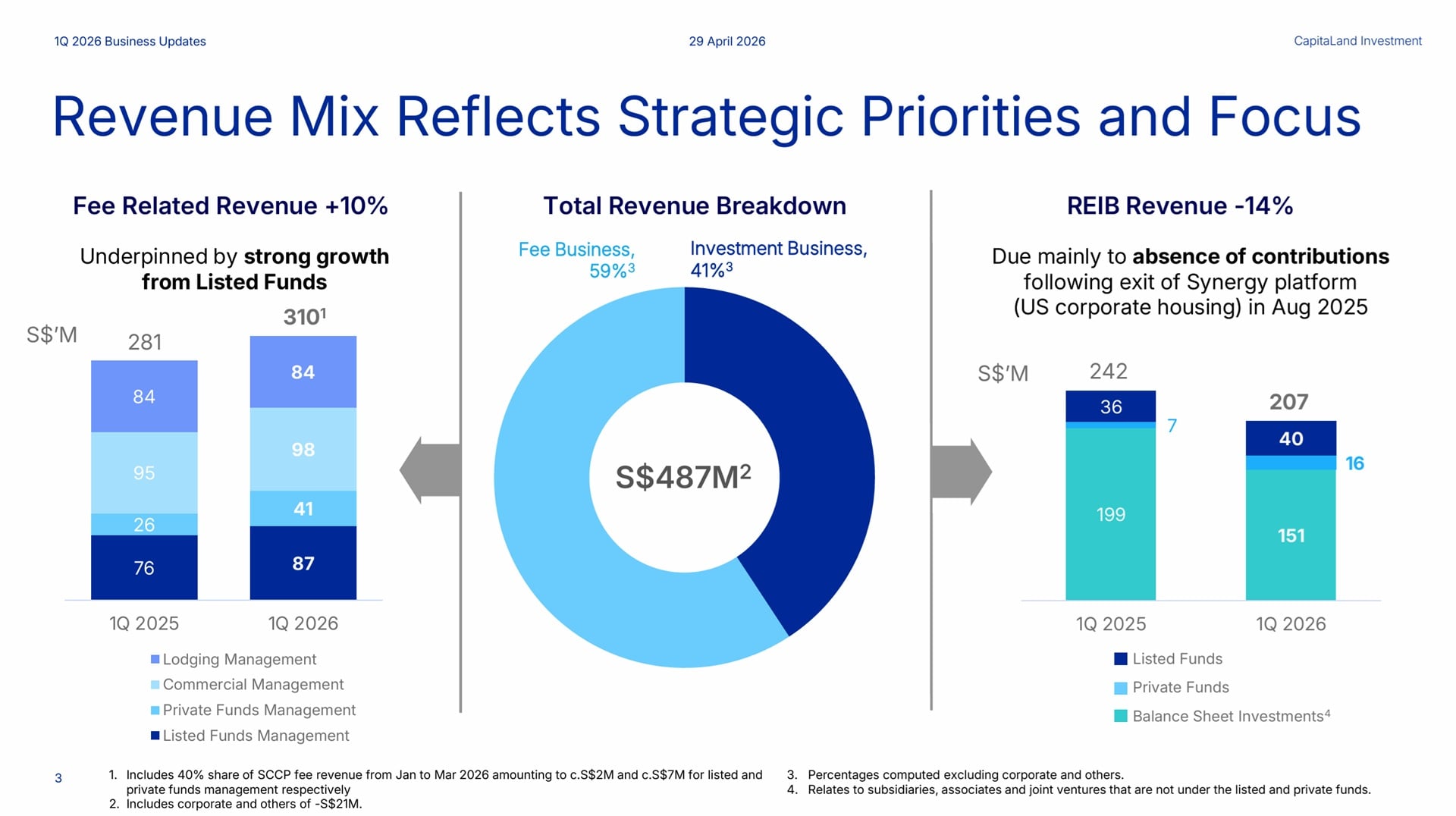

The revenue mix in 1Q 2026 clearly reflects CLI’s strategic priorities. Fee-related businesses contributed a larger share of total revenue compared to investment-related businesses, reinforcing the group’s identity as a global real estate investment manager rather than a traditional developer-owner. At the same time, revenue from the real estate investment business (REIB) declined year-on-year, mainly due to the absence of contributions from divested platforms and assets.

The insights from the CapitaLand Investment 1Q 2026 Business Update are crucial for understanding future performance.

This decline in REIB revenue is not necessarily a negative. It is the flip side of CLI’s capital recycling

strategy, where non-core or lower-conviction assets are sold and capital is redeployed into higher-quality, higher-conviction opportunities. The update highlights that CLI deployed around S$7.2 billion and divested about S$3.4 billion between 1 January and 28 April 2026. That level of activity in a cautious market environment shows that the group is still able to originate, execute and close deals at scale.

This reflects a proactive approach in the CapitaLand Investment 1Q 2026 Business Update that is commendable.

Capital efficiency has also improved. The value of effective stakes in listed funds, private funds and

balance sheet investments have trended lower in some areas due to divestments and valuation adjustments, but this is consistent with CLI’s asset-light, fee-focused strategy.

Scaling the REIT franchise and deepening capital partnerships

The CapitaLand Investment 1Q 2026 Business Update indicates a strong focus on scaling the REIT franchise.

CLI’s listed REITs remain a core pillar of its ecosystem. In the year-to-date period, the REIT platform

announced approximately S$6.9 billion of acquisitions, enhancing income resilience and supporting

fee-related earnings. These acquisitions span multiple geographies and asset classes: suburban and core retail in Singapore, logistics assets in the US, Spain and Singapore, and living and digital infrastructure assets in Japan. On the divestment front, about S$2.9 billion of assets were sold, including a Singapore CBD office and a suburban retail property.

Furthermore, this CapitaLand Investment 1Q 2026 Business Update showcases the company’s strategic acquisitions.

Beyond the existing REITs, CLI is also working toward a second C-REIT listing on the Shanghai Stock

Exchange, with an IPO portfolio of around RMB 4.8 billion. This is strategically important because it

deepens CLI’s presence in China’s public markets and expands its listed funds platform.

On the private funds side, CLI continues to build out a capital-efficient platform across high-conviction strategies. A notable highlight is the S$2.4 billion mandate secured with Income Insurance to manage its Singapore real estate portfolio. The APAC Credit Program II reached final close with about S$400 million of capital commitments, reflecting rising institutional demand for asset-backed real estate credit strategies. In addition, a separately managed account was secured for a Singapore business park, raising roughly S$109 million from a foreign sovereign wealth fund.

Lodging: asset-light growth with improving RevPAU

Specifically, the lodging segment in the CapitaLand Investment 1Q 2026 Business Update is noteworthy.

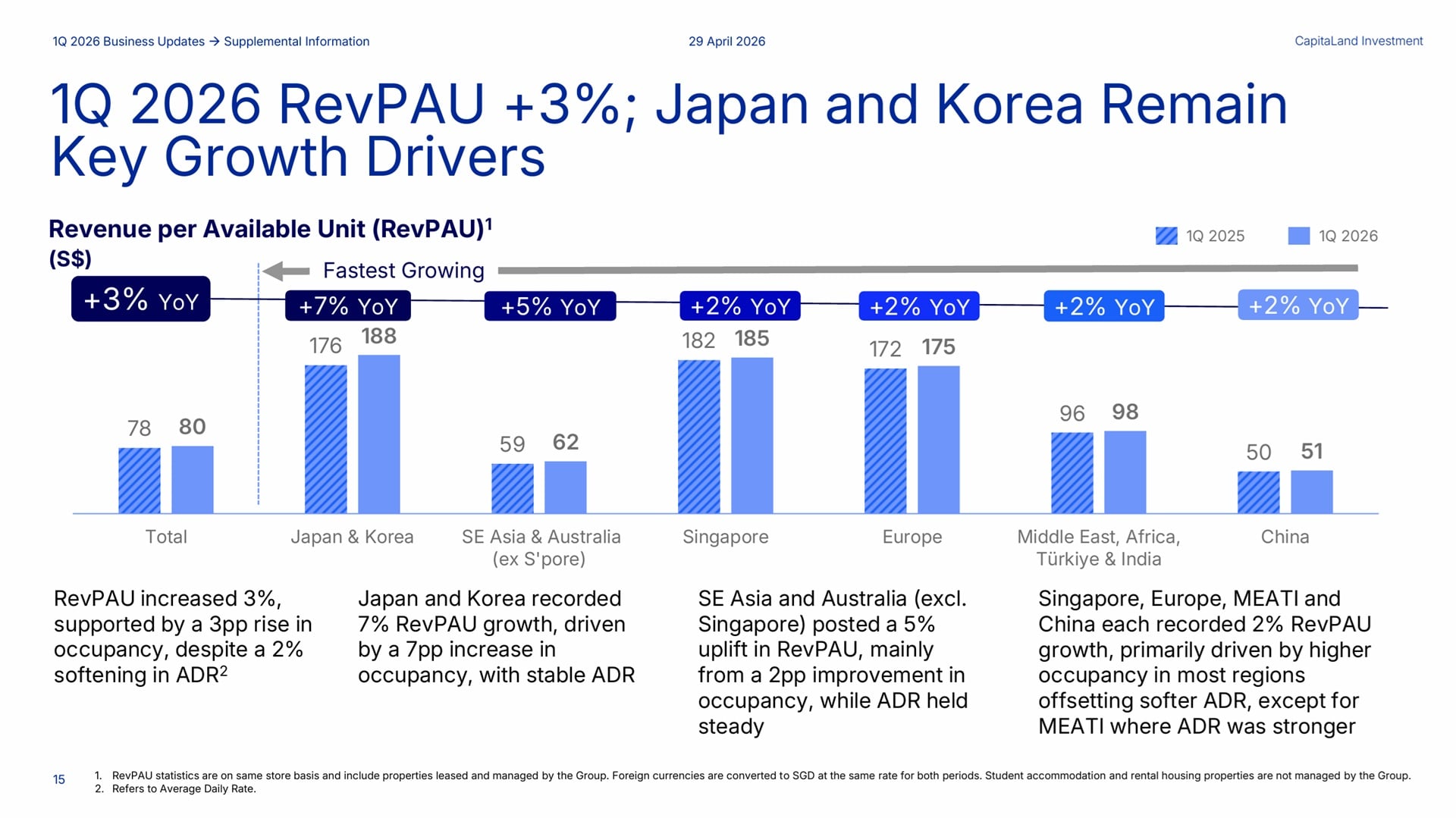

The lodging platform continues to be a bright spot. In 1Q 2026, CLI signed around 1,800 units and opened more than 2,250 units, extending the reach of brands such as Ascott across key markets. Revenue per available unit (RevPAU) increased 3% year-on-year, supported by a three-percentage-point rise in occupancy.

According to the recent CapitaLand Investment 1Q 2026 Business Update, the lodging platform is thriving.

Japan and Korea were standout performers, with RevPAU up 7% on the back of a seven-percentage-point improvement in occupancy.

Southeast Asia remains a key growth engine, with a strong pipeline of property openings over the next 12 months. This should expand the fee income base and help cushion any potential softness in specific markets. At the same time, Ascott is investing in technology and partnerships to scale more efficiently.

Portfolio performance and market conditions

CLI’s portfolio performance remains differentiated across markets. Resilient Asian markets such as

Singapore, Malaysia and India continue to deliver strong occupancies and generally positive rental

reversions. In Singapore, retail occupancy is high and both shopper traffic and tenant sales have grown year-on-year, while office occupancy remains tight with limited vacancy supporting rents.

China, however, remains more challenging. Demand recovery is uneven across asset types, and the leasing environment is competitive, putting pressure on rents. In other developed markets such as Australia, Korea, the US and Europe, conditions are mixed and outcomes vary by local supply-demand dynamics.

Balance sheet strength and why SGD 2.64 looks interesting

The CapitaLand Investment 1Q 2026 Business Update provides insights into the company’s balance sheet strength.

From a risk perspective, CLI’s balance sheet looks solid. Net debt to equity stands at around 0.41x,

with a comfortable interest coverage ratio and a high proportion of fixed-rate debt. Operating cash flow in 1Q 2026 was higher than the same period last year, supported by dividends from associates, joint ventures and other investments.

With the share price at SGD 2.64 as of 5 May 2026, the market seems to be pricing in a fair amount of macro risk and China-related uncertainty, while perhaps not fully recognising the strength of CLI’s recurring fee platform and its capital-light growth model. For me, with CLI at 1.92% of my portfolio, this level looks like an opportunity to at least hold and potentially accumulate gradually.

This culminates in a comprehensive analysis in the CapitaLand Investment 1Q 2026 Business Update that deserves attention.

Summary of CapitaLand Investment 1Q 2026 Business Update

The summary of the CapitaLand Investment 1Q 2026 Business Update highlights critical investment factors.

If you want to invest into CapitaLand Investment based on its 1Q 2026 business update, the pros are:

When considering the CapitaLand Investment 1Q 2026 Business Update, the pros can inform investment decisions.

- Strong and growing fee-related revenue base that provides resilient, recurring earnings.

- Expanding private funds and credit platforms supported by institutional mandates.

- Robust balance sheet with low net gearing and ample debt headroom.

- Strategic acquisitions and divestments that enhance income resilience.

- Lodging platform showing improving RevPAU and strong pipeline.

The cons are:

The CapitaLand Investment 1Q 2026 Business Update also outlines some cons that potential investors should weigh.

- China market remains challenging with uneven demand.

- REIB revenue has declined due to divestments.

- Global macro uncertainty may moderate capital raising and deployment.

- Rising inflation and operating cost pressures could weigh on profitability.