The Singtel FY26 financial results have arrived, and they paint a picture of a telecommunications and digital infrastructure giant that is not only stabilising its core business but also accelerating into new growth engines. As an investor who holds Singtel as 1.30% of my stock portfolio in terms of amount invested, the latest performance update is particularly meaningful. Despite the Singtel share price falling 2.24% to close at S$4.59 on Friday, 22 May 2026, the underlying fundamentals and strategic direction of the Group suggest that FY26 was a year of execution, capital recycling and structural repositioning.

The Singtel FY26 financial results show that the Group is progressing well under its Singtel28 strategy, which aims to transform the company from a traditional telco into a diversified digital infrastructure and services powerhouse. With strong contributions from regional associates, improved profitability from Optus, record bookings at NCS and accelerating momentum in Digital InfraCo, Singtel FY26 results demonstrate that the Group is building a multi‑engine growth model that is more resilient and future‑ready. For investors tracking the Singtel share price, these developments provide important context beyond short‑term price movements.

In this article, I will break down the key highlights of the Singtel FY26 financial results, examine the performance of each major business segment, explore the Group’s capital management initiatives, and discuss what these developments mean for long‑term investors. Throughout this discussion, the Singtel FY26 results and the behaviour of the Singtel share price will be central to understanding whether the stock still deserves a place in a long‑term portfolio.

A Strong Set of Results Driven by Diversification and Execution

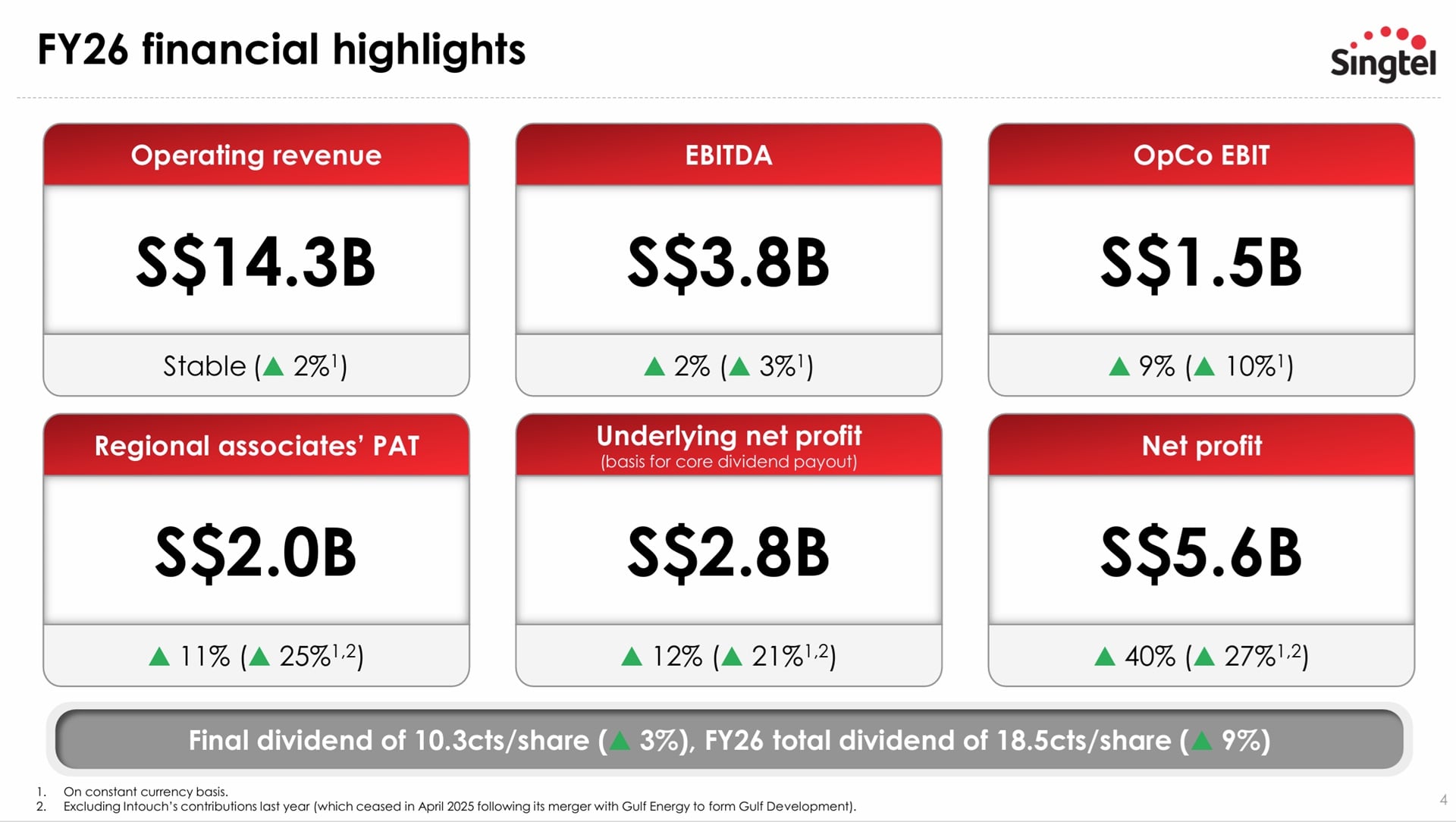

The Singtel FY26 financial results show that the Group delivered a strong performance across its operating companies and regional associates. Underlying net profit rose to S$2.77 billion, driven mainly by Airtel, AIS, NCS, Digital InfraCo and Optus. Excluding foreign currency impact and the absence of Intouch contributions, underlying profit growth would have been even stronger, underscoring the quality of the Singtel FY26 results.

Net profit surged to S$5.61 billion, supported by a net exceptional gain largely from partial stake sales in Airtel. While these exceptional gains are not recurring, they reflect Singtel’s active capital management strategy and its ability to unlock value from its portfolio. For investors watching the Singtel share price, such value realisation events can be important catalysts, even if the market sometimes takes time to fully price them in.

Operating revenue in the Singtel FY26 financial results remained stable at around S$14.26 billion, while EBITDA grew and operating company EBIT rose at a faster pace. These improvements were supported by strong performances from NCS, Digital InfraCo and Optus, which collectively form the backbone of Singtel’s transformation into a digital infrastructure leader. The Singtel FY26 results also highlight that the Group achieved a return on invested capital of 11.1%, up significantly from earlier years, reflecting better capital discipline and higher‑return growth engines.

This improvement in ROIC is particularly important when evaluating the Singtel share price. A higher and rising ROIC suggests that the company is deploying capital more efficiently, which can support higher valuations over time if the market believes the trend is sustainable. The Singtel FY26 financial results therefore signal that the Group is not just growing, but growing in a more profitable and disciplined way.

Regional Associates: Airtel and AIS Lead the Charge

One of the most important components of the Singtel FY26 financial results is the strong contribution from regional associates. Post‑tax earnings from associates increased meaningfully, and excluding Intouch and currency effects, contributions would have risen even more. The Singtel FY26 results clearly show that regional associates remain a powerful earnings engine.

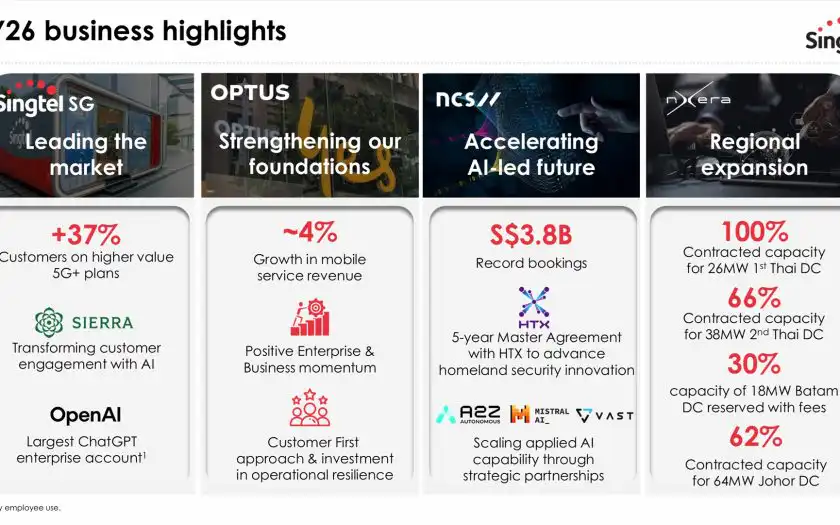

Airtel was a standout performer in the Singtel FY26 financial results, delivering strong earnings growth across India and Africa. Higher ARPU, customer growth and improved operating leverage contributed to this performance. AIS also delivered solid growth driven by mobile, broadband and enterprise services, supported by disciplined cost management and lower depreciation. These trends reinforce the strategic value of Singtel’s stakes in these regional champions.

Globe posted improved results due to stronger mobile and broadband revenue, better performance from its fintech arm and foreign exchange gains, while Telkomsel saw a decline in net profit due to revenue pressure, lease adjustments and tax effects. Overall, the Singtel FY26 results reaffirm that regional associates provide diversification and growth that complement the core operations. For investors, this diversified earnings base can help smooth volatility in the Singtel share price over time.

Optus: Improved Profitability Despite Higher Costs

Optus delivered a resilient performance in the Singtel FY26 financial results. Operating revenue grew, driven by postpaid price increases, prepaid customer growth in amaysim and new network sharing revenue that commenced in early 2025. This revenue growth, combined with cost discipline in key areas, supported a strong uplift in EBIT.

EBIT growth in the Singtel FY26 results was particularly notable at Optus, reflecting mobile growth and network sharing contributions. These gains helped offset higher operating expenses related to network resilience, compliance and remediation. Optus also booked an exceptional loss due to regulatory provisions and retail store buyback costs, but these items do not affect underlying profitability and are part of cleaning up legacy issues.

The Singtel FY26 financial results show that Optus is stabilising after a challenging period and is now focused on improving customer experience, enhancing network performance and modernising its IT platforms. Over time, successful execution in these areas could support better margins and earnings visibility, which in turn may help support the Singtel share price if the Australian business continues to strengthen.

Singtel Singapore: Enterprise Strength Offsets Consumer Weakness

Singtel Singapore’s performance in the Singtel FY26 financial results was mixed. Revenue declined in the consumer segment due to structural price competition, reflecting a mature and highly competitive mobile market. This remains a key headwind and is one of the reasons investors must look beyond just the domestic consumer business when assessing the Singtel FY26 results.

On the other hand, enterprise revenue remained resilient and now contributes more than half of Singtel Singapore’s total revenue. This shift towards enterprise is a central theme in the Singtel FY26 financial results and aligns with the Group’s broader strategy to focus on higher‑value, stickier services. However, EBIT was lower due to reduced operating revenue, spectrum amortisation and continued investments in AI capabilities and digital platforms.

The Singtel FY26 results also highlight the Group’s tri‑brand strategy in Singapore, with Singtel, GOMO and hi! targeting different customer segments. While the regulator’s suspension of the proposed industry consolidation review adds uncertainty to the competitive landscape, Singtel continues to focus on improving churn, enhancing customer value and expanding enterprise solutions. For investors, the domestic business is no longer the sole driver of the Singtel share price, but it remains an important foundation.

NCS: Record Bookings and Strong AI‑Driven Growth

NCS delivered one of the strongest performances in the Singtel FY26 financial results. Revenue rose as demand for digital resilience, AI, data and core IT services remained robust across all business segments. EBIT increased significantly, even after adjusting for a one‑off credit, reflecting improved delivery margins and better operational efficiency.

Record bookings of S$3.8 billion and a book‑to‑bill ratio of 1.2 position NCS for continued growth in FY27. The Singtel FY26 results show that NCS is becoming a major growth engine, benefiting from rising demand for AI‑led transformation across the public sector, defence, healthcare, transportation, telco and financial services. This positions NCS as a key pillar in the Group’s long‑term strategy.

For investors, the strong NCS performance in the Singtel FY26 financial results suggests that Singtel is successfully building a scalable digital services business that can complement its connectivity and infrastructure assets. As this segment grows, it could contribute to a re‑rating of the Singtel share price if the market assigns higher multiples to recurring, high‑value digital services revenue.

Digital InfraCo: Scaling Data Centres and AI Infrastructure

Digital InfraCo delivered exceptional growth in the Singtel FY26 financial results. Revenue increased strongly, driven by Nxera’s higher data centre utilisation and the operational commencement of its large DC Tuas facility in Singapore. This facility, combined with regional data centres in Thailand, Batam and Johor, forms the backbone of Singtel’s regional digital infrastructure strategy.

EBIT growth in the Singtel FY26 results was also impressive at Digital InfraCo, boosted by strong customer demand and contributions from RE:AI, the Group’s GPU‑as‑a‑Service and AI‑as‑a‑Service business. RE:AI began commercialisation in January 2026 and has already seen healthy customer sign‑ups, with long‑term contracts providing visibility on future revenue.

The acquisition of STT GDC, expected to complete in the second half of 2026, will create a combined design capacity of about 2.8GW across Asia and Europe. This positions Singtel as a global data centre player with significant strategic optionality. The Singtel FY26 financial results make it clear that digital infrastructure is no longer a side business but a core growth engine that could materially influence the Singtel share price over the medium to long term.

Capital Management: Recycling Assets and Funding Growth

The Singtel FY26 financial results highlight the Group’s active capital management strategy. Around S$3.9 billion of assets were recycled during the year, contributing to a reduction in net debt to S$8.7 billion. The Group has already achieved more than half of its S$9 billion mid‑term asset recycling target, which is intended to fund growth initiatives and shareholder returns.

The Group declared its highest ever annual dividend of 18.5 cents per share, comprising core dividends and value realisation dividends. The core payout ratio remains at 80% of underlying net profit, signalling a commitment to sustainable and progressive dividends. For income‑focused investors, this aspect of the Singtel FY26 financial results is particularly attractive, even if the Singtel share price can be volatile in the short term.

Singtel also executed share buybacks under its Value Realisation Share Buyback programme, further enhancing shareholder returns. The Singtel FY26 results show that the Group is balancing investment in growth areas such as data centres and AI infrastructure with meaningful capital returns. This balanced approach is a key consideration when deciding whether to increase or maintain exposure to Singtel in a diversified portfolio.

Outlook for FY27: Cautious but Focused on Growth Engines

The Singtel FY26 financial results outline a cautious outlook for FY27 due to global uncertainty, particularly from the Middle East conflict and its potential impact on energy prices, inflation and currency volatility. While Singtel has no direct operations in the Middle East, second‑order effects could influence consumer and business sentiment in its key markets.

OpCo EBIT growth is expected to be between low and mid‑single digits, reflecting a more cautious stance after a strong FY26. Total capital expenditure is projected at around S$3.0 billion, with core capex remaining stable and growth capex focused on data centres, AI infrastructure and submarine cables. The Singtel FY26 results also indicate that the Group expects substantial dividends from regional associates, supplemented by special dividends already received.

Despite the cautious macro outlook, the Singtel FY26 financial results show that the Group is well‑positioned to scale its digital infrastructure ecosystem, expand its AI capabilities and strengthen its enterprise business. For long‑term investors, the key question is whether the current Singtel share price adequately reflects these structural growth drivers and the improving quality of earnings.

Pros and Cons of Investing in Singtel Based on Singtel FY26 Financial Results

The Singtel FY26 financial results reveal several advantages for long‑term investors. Singtel delivered strong underlying profit growth, improved return on invested capital and robust contributions from regional associates such as Airtel and AIS. The Group is scaling high‑growth businesses including data centres, AI infrastructure and digital services, which provide structural tailwinds beyond traditional telco revenues. Capital management remains active, with significant asset recycling, share buybacks and the highest annual dividend declared to date. The diversified business model across Asia, Australia and Africa provides resilience and multiple earnings engines that can help stabilise performance even when individual markets face headwinds. For an investor like me, with Singtel making up 1.30% of my stock portfolio, the Singtel FY26 results reinforce the case for keeping Singtel as a core, income‑generating and growth‑linked holding, even if the Singtel share price occasionally reacts negatively to short‑term news.

However, the Singtel FY26 financial results also highlight some challenges and risks. The consumer business in Singapore continues to face structural price competition, which weighs on revenue and EBIT and may limit growth in the domestic market. Optus, while improving, still incurs higher operating costs due to compliance, remediation and network resilience investments, which could pressure margins if revenue growth slows. Global macroeconomic uncertainty, particularly from energy price volatility, inflation and currency fluctuations, may affect earnings translation and investor sentiment towards regional markets. The Group’s transformation into a digital infrastructure and services leader requires sustained capital expenditure, which may cap near‑term free cash flow growth even as long‑term value is being created. These factors can contribute to periods of weakness in the Singtel share price, as seen when the Singtel share price fell 2.24% to S$4.59 on 22 May 2026 despite solid Singtel FY26 results. Ultimately, the decision to invest or stay invested in Singtel hinges on whether one believes that the long‑term benefits of its digital infrastructure, AI and regional growth strategy outweigh the near‑term competitive and macroeconomic risks reflected in the Singtel FY26 financial results.