The Singtel FY26 financial results have arrived, and they paint a picture of a telecommunications and digital infrastructure giant that is not only stabilising its core business but also accelerating into new growth engines. As …

Continue reading

Growing Wealth for a Sweet Retirement.

Stock news, analysis and financial results related to Singtel. My stock analysis will provide the current dividend yield based on historical payout and current stock price.

The Singtel FY26 financial results have arrived, and they paint a picture of a telecommunications and digital infrastructure giant that is not only stabilising its core business but also accelerating into new growth engines. As …

Continue reading

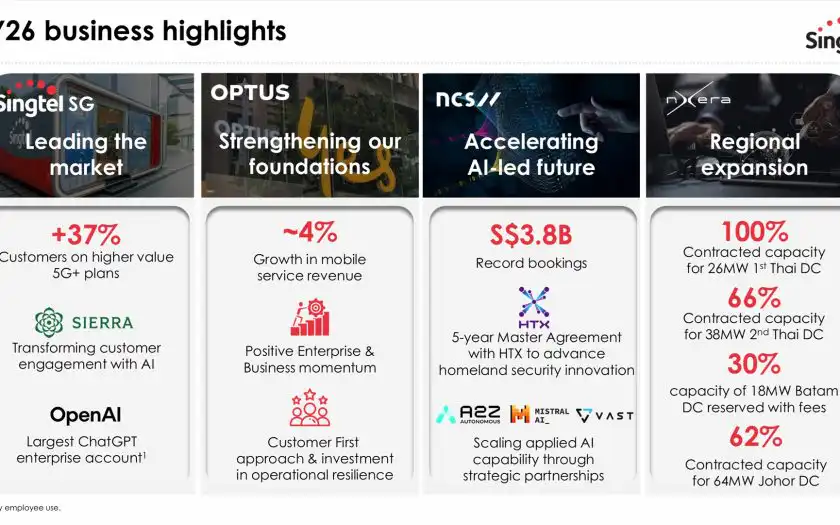

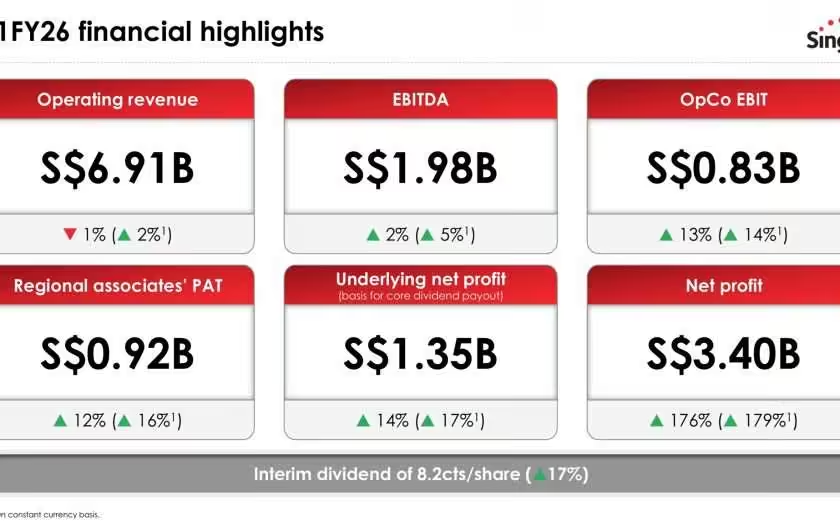

Singtel’s H1FY26 financial results mark a pivotal moment in its transformation journey, showcasing the strength of its diversified portfolio and strategic execution amid macroeconomic headwinds. The Group reported a net profit of S$3.40 billion, a …

Continue reading

Singtel (SGX: Z74) has recently experienced a notable surge in its share price, reaching a five-year high. This rally is not merely a fleeting upward trend but rather a testament to the company’s strategic reset, …

Continue reading

This is the last month of the year 2023 and again I am going to provide an update on the progress of myself trying to reach my targeted financial goals for December 2023. The total …

Continue readingSingtel currently makes up 2.38% of my stock portfolio. The telco had announced their 4Q2019 financial results on 28th May 2020. The underlying net profit was down 13% to S$2.46 billion due mainly to weakness …

Continue reading

Today is a special day (29th February 2020). Instead of the usual 28 days, we have 29 days in this month of February 2020, which is also called the leap year. We are also in …

Continue readingSingtel had released its 3QFY20 financial results on 13 February 2020. The financial results are not so rosey, with operating revenue declining 5% to S$4.38 billion due to lower equipment sales, weak business sentiment and …

Continue readingCurrently, Singtel makes up 9% of my wife’s stock portfolio. On 8th August 2019, Singtel has released their 1QFY20 financial results. Singtel has posted a net profit of S$541 million that was down a whopping …

Continue reading