![]()

Currently, Singtel makes up 9% of my wife’s stock portfolio. On 8th August 2019, Singtel has released their 1QFY20 financial results. Singtel has posted a net profit of S$541 million that was down a whopping 35%. This was due to Airtel’s losses. There was no surprises that an associate losses can have a lot of impact on Singtel as 48% of Singtel’s net profit comes from its Regional Associates which consists of Airtel, AIS, Telkomsel and Globe.

If we put the negative news about Airtel aside, below are the positives from the rest of the associates:

- Telkomsel in Indonesia posted an 18% increase in earnings on robust growth in data and digital services.

- In the Philippines, Globe saw strong data revenue growth from its mobile and broadband businesses.

Here are the financial highlights for Singtel’s Quarter Ended 30 June 2019.

Debt

In the quarter, Singtel paid S$735 million for subscription to Airtel’s rights issue based on its rights entitlement for its direct stake of 15%. On top of this, Singtel has invested on upgrading its network and spectrum (5G). Overall, net debt increased by S$1.97 billion from a quarter ago to S$11.85 billion. With higher net debt, net debt gearing ratio increased to 28.4%.

Free Cash Flow

Free cash flow for the quarter was S$1.22 billion, down 17% due to lower associates’ dividends and higher capital expenditure.

Dividend Yield

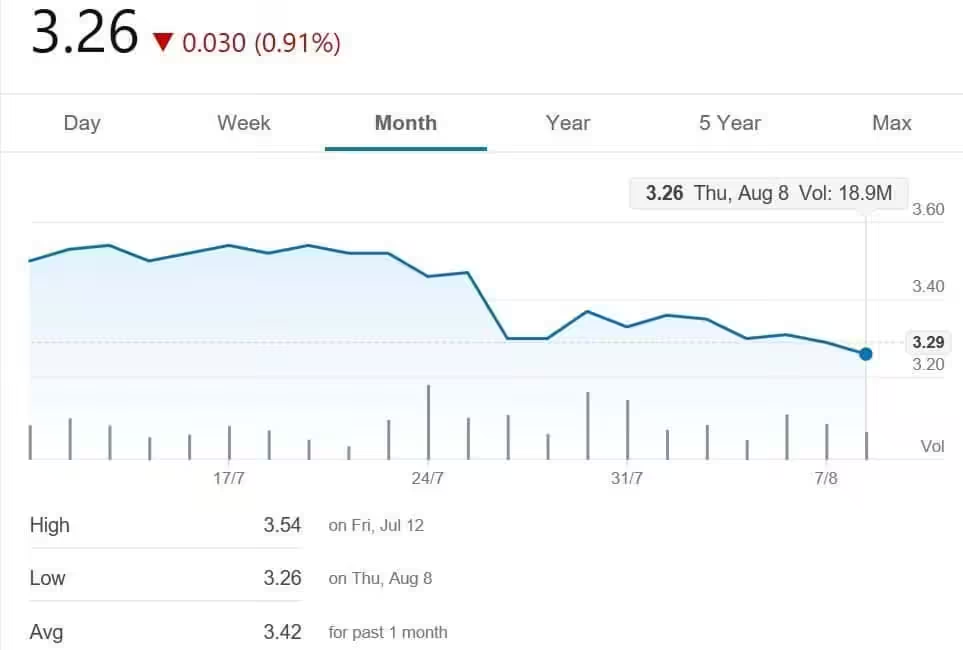

Based on the current closing share price of S$3.26 and historical dividend payout of 17.5 cents, the current dividend yield is 5.37%. The current yield is attractive but take note of the outlook below. My personal opinion is that growth has slowed down and outlook does not seem rosy. The main concern here is still about Airtel and what is Singtel going to do about it.

Can Singtel continue to sustain its dividends?

Outlook

Here is a summary of the outlook for Singtel as indicated in its management report.

- Excluding acquisitions, consolidated revenue for the Group to grow by mid single digit and consolidated EBITDA to grow by high single digit.

- Capital expenditure is expected to approximate S$2.2 billion, comprising A$1.4 billion for Optus and S$0.8 billion for the rest of the Group.

- Group free cash flow (excluding spectrum payments and dividends from associates) to be around S$2.4 billion.

- Dividends from the regional associates are expected to be around S$1.2 billion, reflecting Telkomsel’s lower earnings for its financial year ended 31 December 2018.

- Revenue from ICT services to grow by low single digit.

- Cyber security revenue to increase by low teens.

- Amobee’s operating revenue (including intragroup revenue) to grow by high single digit and its EBITDA to improve.