![]()

Singtel currently makes up 2.38% of my stock portfolio. The telco had announced their 4Q2019 financial results on 28th May 2020. The underlying net profit was down 13% to S$2.46 billion due mainly to weakness in Australia. The weakness in Australia was due to continuing data price competition and weak consumer sentiment, and the effects of lower equipment sales and margins and low NBN resale margins.

In consideration of Airtel’s exceptional charges of S$1.80 billion, the net profit declined by 65% to S$1.08 billion as compared to S$3.10 billion a year ago. The exceptional charges refer to regulatory costs, including the adjusted gross revenue matter and a one-time spectrum charge. Singtel took a net exceptional charge of S$302 million this quarter, mainly arising from Airtel’s provision for the spectrum charge.

Operating revenue for the full year also declined 2% in constant currency terms at S$16.54 billion, a result of lower mobile service revenue and equipment sales, aggravated by the onset of COVID-19.

Debt

Singtel’s group net debt stood at S$12.50 billion including S$2.1 billion of lease liabilities recognised under the new accounting standards. I believe free cash flow is something investors are concern about. The good news is that free cash flow rose 4% to S$3.78 billion for the full year with the impact of changes in accounting standards, positive working capital and lower tax payments.

Dividends

I have bought into Singtel for its consistent payout of dividends. Singtel had announced a final dividend of 5.45 cents. The total dividends paid in FY2020 is 12.25 cents as compared to 17.5 cents paid in FY2019. This is a 30% reduction in dividends.

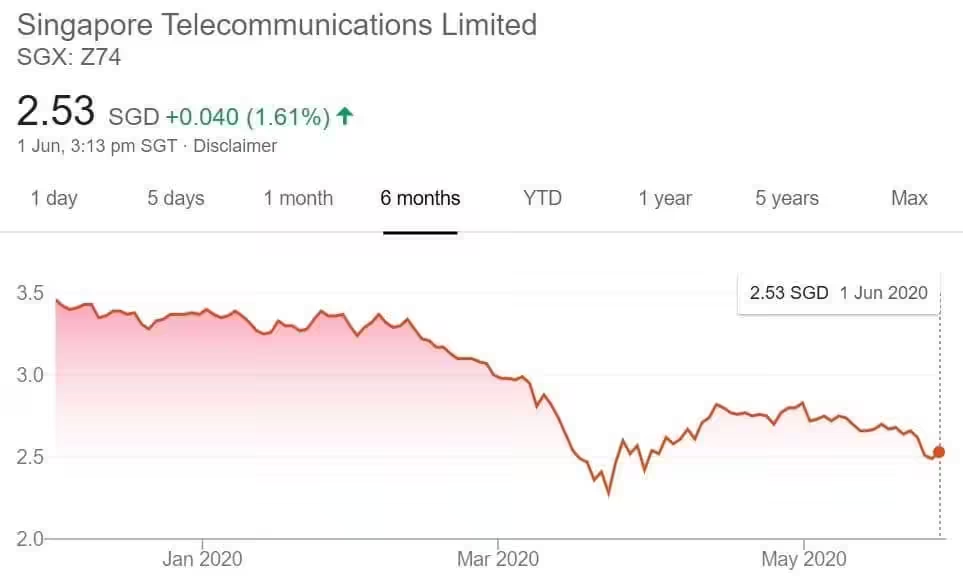

Based on the current share price of S$2.53 and FY20 dividend payout of 12.25 cents, this translate to a current dividend yield of 4.84%.

Summary

The outlook for Singtel remains weak due to stiff competition from other Telcos in different countries. Even though Singtel has won the 5G spectrum, my opinion is unless there is some value gained out of 5G spectrum, this can hardly translate into profits for Singtel. This is not to mention about the capital expenditure required into developing the infrastructure for thhe 5G network.

I am not too concern about the weak share price of Singtel as it only makes up a minority of my stock portfolio. The catalyst for Singtel comes from its regional associates. Since the COVID-19 pandemic has impacted businesses across the globe, the regional associates are impacted as well in a way or another. Meanwhile, I shall hold on to Singtel in view of the day it regains its glory in terms of dividend payout.