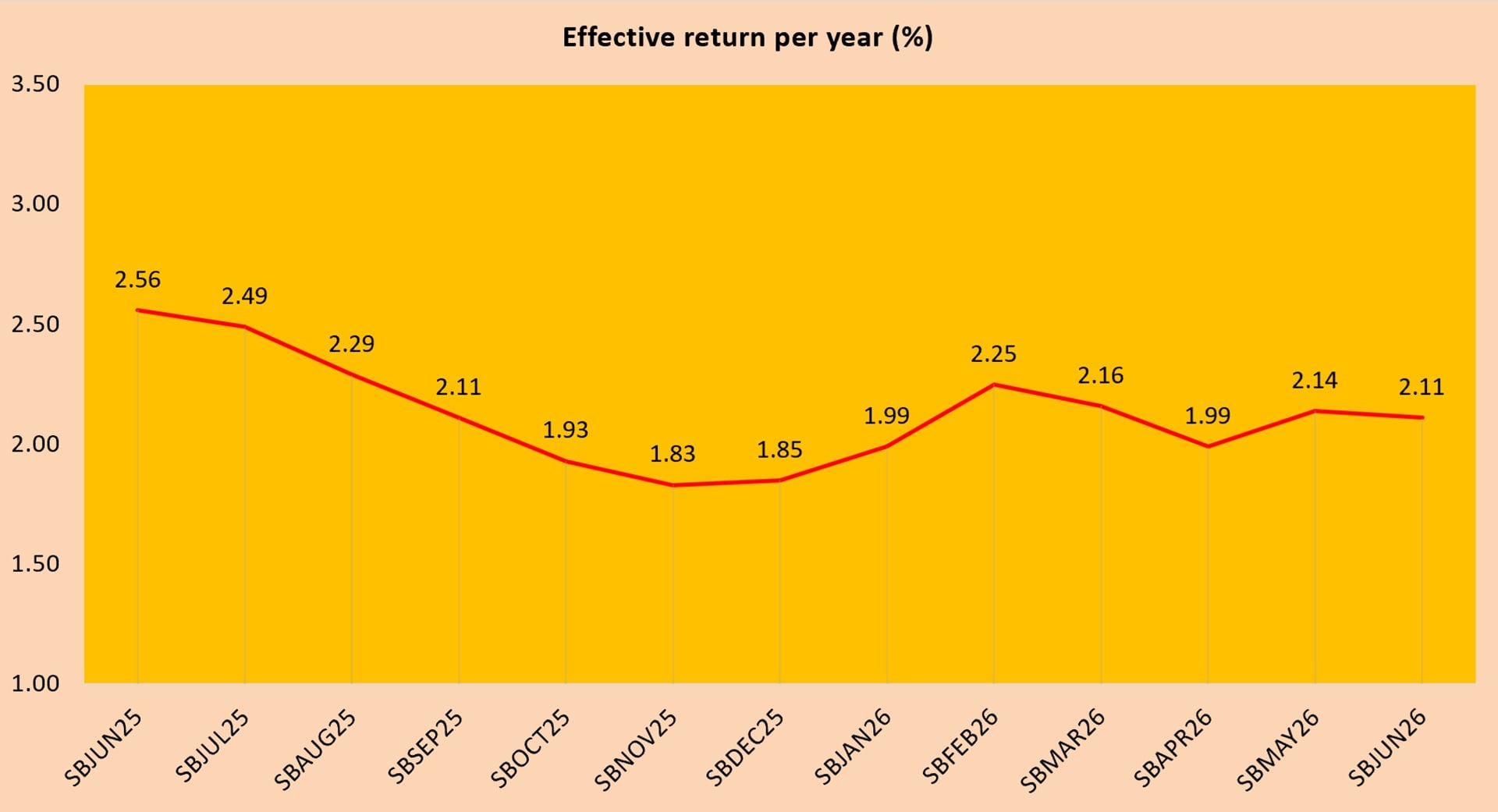

The latest Singapore Savings Bond (SBJUN26, GX26060N) offers an effective return of 2.11% over 10 years if I hold it to maturity. Even if I choose to redeem it after just one year, the 1.46% first‑year interest rate still beats what many digital banks are paying today. For comparison, GXS Bank’s saving and boost pockets currently offer 1.08% and 1.30% per annum, both lower than the starting yield of this Singapore Savings Bond tranche.

One of the biggest advantages of the Singapore Savings Bond is its stability. Unlike promotional bank rates that change every few months, SSB interest rates are transparent and predictable. The built‑in step‑up interest structure means the longer I stay invested, the higher my effective return becomes. This fits neatly with how I plan for retirement, where consistency matters more than chasing the next short‑term offer.

When it comes to building a stable foundation for my portfolio, Singapore Savings Bonds naturally stand out. They are designed to be low‑risk, especially when compared with more volatile investments like individual stocks or ETFs. Market‑linked assets can swing sharply with economic news, earnings reports, or global events, but SSBs offer something far simpler: steady, predictable returns backed by the Singapore Government.

For anyone who values capital preservation and peace of mind, Singapore Savings Bonds serve as a reliable anchor. They may not deliver the explosive gains that equities sometimes offer, but they also do not expose me to the same level of uncertainty. In a long‑term financial plan, that stability is worth a lot.

Minimum investment amount for Singapore Savings Bonds

The minimum investment amount for a Singapore Savings Bond is just S$500, which makes it easy to start small and build a position gradually. This low entry point is ideal for new investors who want to get comfortable with government bonds, as well as for more experienced investors who are looking to park spare cash in a safe, interest‑bearing instrument.

Each individual can invest up to S$200,000 in Singapore Savings Bonds, inclusive of both cash and SRS contributions. The longer you hold them, the higher your effective return, thanks to the step‑up interest feature. This structure rewards patience and disciplined saving, which is exactly the kind of habit I’ve been trying to build over the years.

How the Singapore Savings Bond fits into my long‑term plan

Adding SBJUN26 to my portfolio is not just another investment move. It reinforces the long‑term strategy my wife and I have been shaping for years: slow, steady growth, predictable income,

and the comfort of knowing our retirement plans are progressing in the right direction.

Instead of constantly hunting for the next promotional bank rate, I can rely on the Singapore Savings Bond framework to provide clarity on how my money will grow over time. In an environment where interest rates and market sentiment can change quickly, the Singapore Savings Bond offers something increasingly rare: a simple, transparent, and government‑backed way to grow my savings.

For me, that combination of safety, flexibility, and predictability makes SSBs a core building block of my long‑term financial plan.

Key reasons the Singapore Savings Bond stands out

- Government‑backed security: Capital is protected and backed by the Singapore Government.

- Step‑up interest: The longer you hold, the higher your effective return over the 10‑year period.

- Flexible redemption: Redeem monthly with no capital loss, subject to a small fee.

- Low minimum investment: Start from just S$500 and scale up gradually.

- Predictable returns: Clear visibility of future interest rates helps with retirement and cash‑flow planning.

- Low risk vs. equities: Less volatility than stocks or ETFs, making it suitable for conservative investors.

For investors who prioritise stability and capital preservation, the Singapore Savings Bond remains

one of the most dependable options available. It may not be the flashiest investment, but as part of a diversified portfolio, it quietly does exactly what it is designed to do which is to grow your savings steadily over time.

How to Buy Singapore Savings Bonds Online

Buying Singapore Savings Bonds is a straightforward process, and everything can be done digitally once you have an individual CDP account with the Central Depository. This account is essential because it serves as the place where your SSB holdings will be kept. After your CDP account is set up, you can apply for SSBs through the online banking platforms of DBS/POSB, OCBC or UOB, or by using their ATMs. Simply log in to your bank account, navigate to the Singapore Government Securities section and follow the on‑screen instructions to submit your application.

The minimum investment amount is $500, and you can increase your subscription in multiples of $500, up to a maximum of $200,000 per SSB issuance. A new bond is released every month, and its interest rates are updated annually based on prevailing market conditions. Once your application is successful, interest will be paid to you twice a year, and your full principal will be returned at the end of the ten‑year term.

Can I redeem Singapore savings bonds before maturity?

You are free to redeem your Singapore Savings Bonds (SSBs) at any time before they mature, and there is no penalty for doing so. This flexibility is one of the reasons SSBs are so popular. You are not locked in, and there is no minimum holding period. If you ever need to access your funds, you can simply redeem your bonds in any month of your choosing.

Redemption is straightforward. You can submit a request through DBS digibank (mobile or online) or use any DBS/POSB ATM. Applications open at 6:00 pm on the first business day of the month and close at 9:00 pm on the fourth last business day. Do note that redemptions can only be made Monday to Saturday, between 7:00 am and 9:00 pm, excluding public holidays. Each request comes with a non‑refundable S$2 fee, and once submitted, it cannot be changed or cancelled.

Where Can I Check the Latest Interest Rates for Singapore Savings Bonds?

The latest Singapore Savings Bond interest rates are published on the Monetary Authority of Singapore’s Singapore Savings Bond Portal. Each monthly issuance comes with a full schedule of rates across the ten‑year term, making it easy for investors to review and compare returns. MAS also provides a Singapore Savings Bonds Calculator, which allows you to estimate your total interest earnings based on your investment amount and holding period.

For instance, an investment of S$10,000 in the SBJUN26 (GX26060N) tranche held to maturity would generate a total of S$2,136.60 in interest. Below is the breakdown of the annual payouts for SBJUN26 (GX26060N) across its ten‑year duration.

| Year from issue date | Interest % | Average return per year %* |

| 1 | 1.46 | 1.46 |

| 2 | 1.60 | 1.53 |

| 3 | 1.73 | 1.60 |

| 4 | 1.87 | 1.66 |

| 5 | 2.02 | 1.73 |

| 6 | 2.19 | 1.80 |

| 7 | 2.36 | 1.88 |

| 8 | 2.53 | 1.95 |

| 9 | 2.70 | 2.03 |

| 10 | 2.87 | 2.11 |

*At the end of each year, on a compounded basis.

How To Track Singapore Savings Bonds?

You can monitor your Singapore Savings Bonds by visiting the Monetary Authority of Singapore (MAS) website, which offers up-to-date information on bond issuance and performance.

![]() I use Stocks Café to track my SSB Singapore purchases. If you like to know more about Stocks Cafe, please read up my previous review of Stocks Cafe.

I use Stocks Café to track my SSB Singapore purchases. If you like to know more about Stocks Cafe, please read up my previous review of Stocks Cafe.

Should I Consider SBJUN26 (GX26060N)?

Last month, I added SBMAY26 to my portfolio as part of a long‑term plan my wife and I have been steadily building over the years. It wasn’t a flashy move, but it was a sensible one, exactly the kind of disciplined, low‑maintenance decision that keeps a retirement strategy on track. The Singapore Savings Bond has always appealed to me for its predictability. Once I lock in a tranche, I know my returns will quietly compound in the background while I focus on the rest of my financial goals.

This month’s SBJUN26 tranche comes with a slightly lower effective interest rate compared to SBMAY26, but it still stands out as an attractive option in today’s environment. When I compare it with fixed deposits or so‑called “high‑yield” savings accounts, the Singapore Savings Bond continues to offer a compelling balance of safety, flexibility, and long‑term value. Fixed deposits often require higher minimum placements and lock‑in periods, while high‑yield accounts can change their promotional rates without warning. In contrast, the SSB gives me a transparent 10‑year interest schedule from day one.

What makes the Singapore Savings Bond especially appealing is how it fits into a broader financial plan. It’s not meant to replace equities or other growth assets, but it complements them beautifully. While markets move up and down, the SSB provides a steady anchor—government‑backed, low‑risk, and designed to reward patience through its step‑up interest structure. Even when a tranche’s headline rate dips slightly, the overall value proposition remains strong because the SSB isn’t just about chasing the highest yield. It’s about building a stable foundation that supports long‑term goals like retirement, education funding, or simply maintaining peace of mind.

So even though SBJUN26 offers a marginally lower return than SBMAY26, it still earns its place in my portfolio. It reinforces the same principles that guided my earlier purchase: slow, steady growth and the confidence that comes from knowing part of my savings is working quietly, safely, and predictably in the background.