I am going to look at Frasers Logistics and Commercial Trust 1HFY26 Financial Results. Frasers Logistics and Commercial Trust (FLCT) has released its financial results for the first half of FY2026, offering investors a clearer view of how the REIT is navigating a challenging global environment. As someone who holds FLCT as 7.09% of my stock portfolio in terms of amount invested, these results are particularly relevant in assessing whether the REIT continues to justify its position as a core logistics and industrial play.

The latest numbers based on Frasers Logistics and Commercial Trust 1HFY26 Financial Results show a REIT that remains fundamentally resilient, supported by strong rental reversions, high occupancy in its logistics and industrial segment, and disciplined capital management. At the same time, softer performance in the commercial portfolio and a slight dip in DPU highlight the ongoing pressures in certain markets. Overall, FLCT continues to demonstrate stability, but with nuances that investors should pay attention to.

Revenue and income performance

FLCT reported revenue of S$238.9 million for 1HFY26, a 2.8% increase from the previous year’s S$232.3 million. Adjusted net property income also rose 3.6% to S$167.0 million, supported by positive rental reversions and annual rent increments across its Australia and Europe logistics and industrial segments. These figures were also helped by stronger average exchange rates for the AUD, EUR and GBP during the period, which boosted the translated Singapore dollar income.

The REIT benefited from the full contribution of its recently acquired property at 2 Tuas South Link 1, which was completed in November 2024. However, these gains were partially offset by the divestment of 357 Collins Street in September 2025, higher vacancies in Alexandra Technopark and Farnborough Business Park, and increased non-recoverable land taxes in Victoria and Queensland, Australia.

Distributable income came in at S$111.9 million, slightly lower than the S$113.0 million recorded a year ago. This was mainly due to a smaller capital distribution from divestment gains, which dropped from S$18.0 million to S$5.0 million. Excluding capital distributions, distributable income before divestment gains actually rose by double digits, reflecting the underlying strength of the portfolio and the contribution from organic rental growth.

DPU performance and yield

FLCT declared a distribution per unit (DPU) of 2.95 Singapore cents, a slight decline of 1.7% from the 3.00 cents paid in 1HFY25. Based on Frasers Logistics and Commercial Trust 1HFY26 Financial Results, the main reason for this decline was the lower capital distribution from divestment gains. On an annualised basis, this translates to a distribution yield of 6.6%, based on the closing price of S$0.895 as at 31 March 2026.

While the headline DPU dipped, the DPU before capital distribution actually improved, rising from 2.52 cents to 2.82 cents. This improvement was driven by stronger rental performance and the contribution from new acquisitions. The REIT also took 75.0% of management fees in units, compared to 43.1% in the previous year, which helped preserve cash for distributions and supported the payout ratio.

Portfolio performance and rental reversions

One of the standout highlights of Frasers Logistics and Commercial Trust 1HFY26 Financial Results is the strong rental reversion achieved across its portfolio. For the period from January to March 2026, the REIT recorded average rental reversions of +8.8% on an incoming-versus-outgoing rent basis and +22.0% on an average-versus-average rent basis. These are robust numbers that underscore the strength of demand for its assets.

The logistics and industrial segment was the main driver, achieving reversions of +9.4% and +23.2% respectively on the same measures. This reflects the continued strength of demand for high-quality logistics space in Australia and Europe, where supply remains tight and structural demand drivers such as e-commerce, supply chain optimisation and nearshoring continue to support rental growth.

In contrast, the commercial portfolio saw more modest performance, with overall reversions at around flat on an incoming-versus-outgoing basis and mid-single-digit positive on an average-versus-average basis. The commercial segment continues to face headwinds, particularly in markets like Singapore and the UK where business park and office demand remains uneven and tenants are more selective, often gravitating towards the best-in-class buildings.

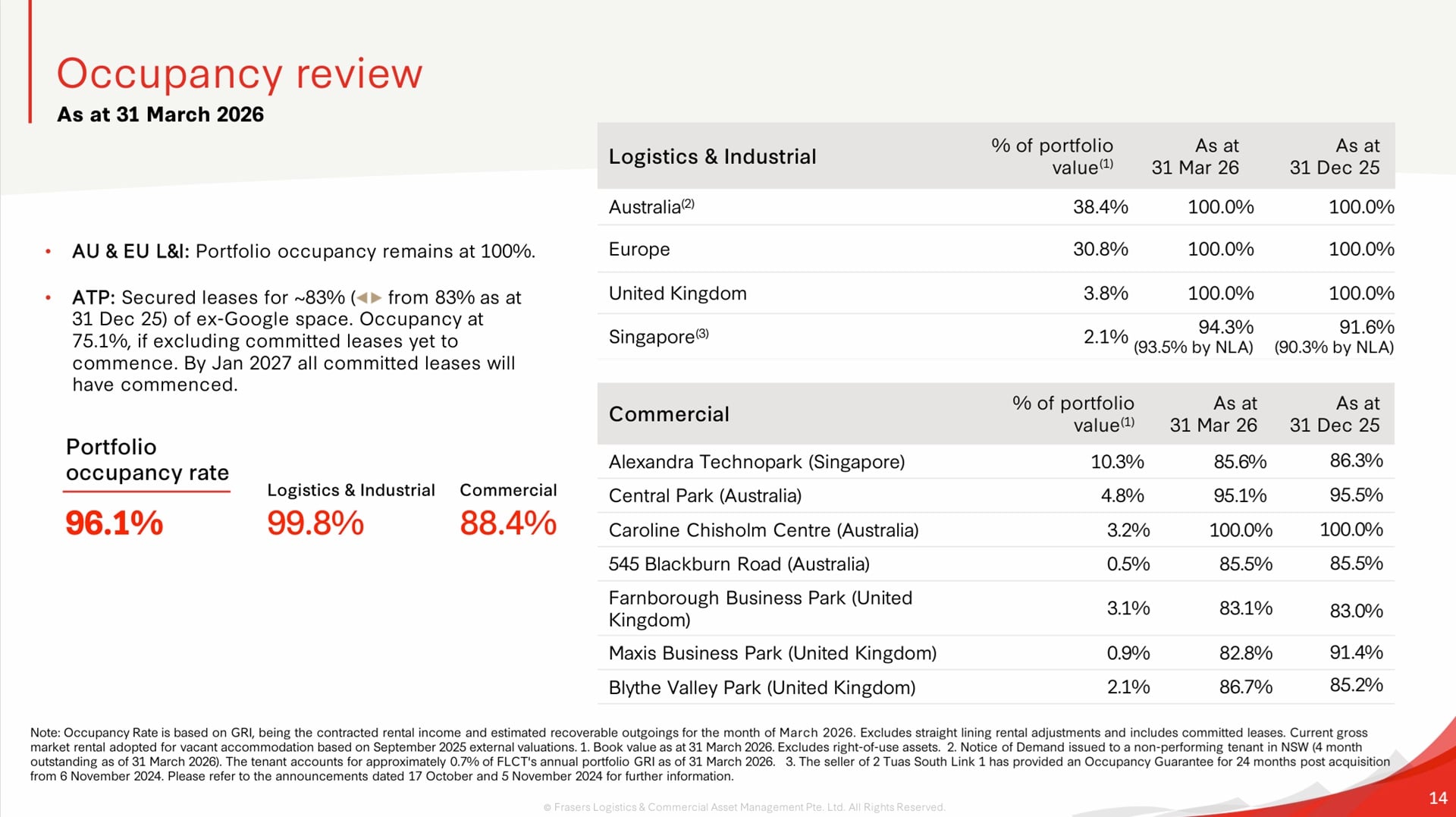

Occupancy and lease profile

FLCT maintained a healthy portfolio occupancy of 96.1% as at 31 March 2026. The logistics and industrial portfolio remains exceptionally strong at 99.8% occupancy, underscoring the resilience of this asset class and the quality of FLCT’s tenant base. The commercial portfolio, however, stands at 88.4%, reflecting ongoing challenges in office and business park markets across Singapore, Australia and the UK.

Alexandra Technopark (ATP) in Singapore continues to be a key area of focus. The REIT has secured leases for approximately 83% of the former Google space, with occupancy expected to improve further as committed leases commence progressively through January 2027. This staged backfilling helps to stabilise income but also means that some upside will only be fully visible over the next few years.

FLCT’s weighted average lease expiry (WALE) stands at 4.9 years, providing good income visibility. A significant proportion of leases are embedded with fixed escalations or CPI-linked indexation, offering built-in rental growth and a partial hedge against inflation. This lease structure is particularly valuable in an environment where costs and interest rates remain elevated.

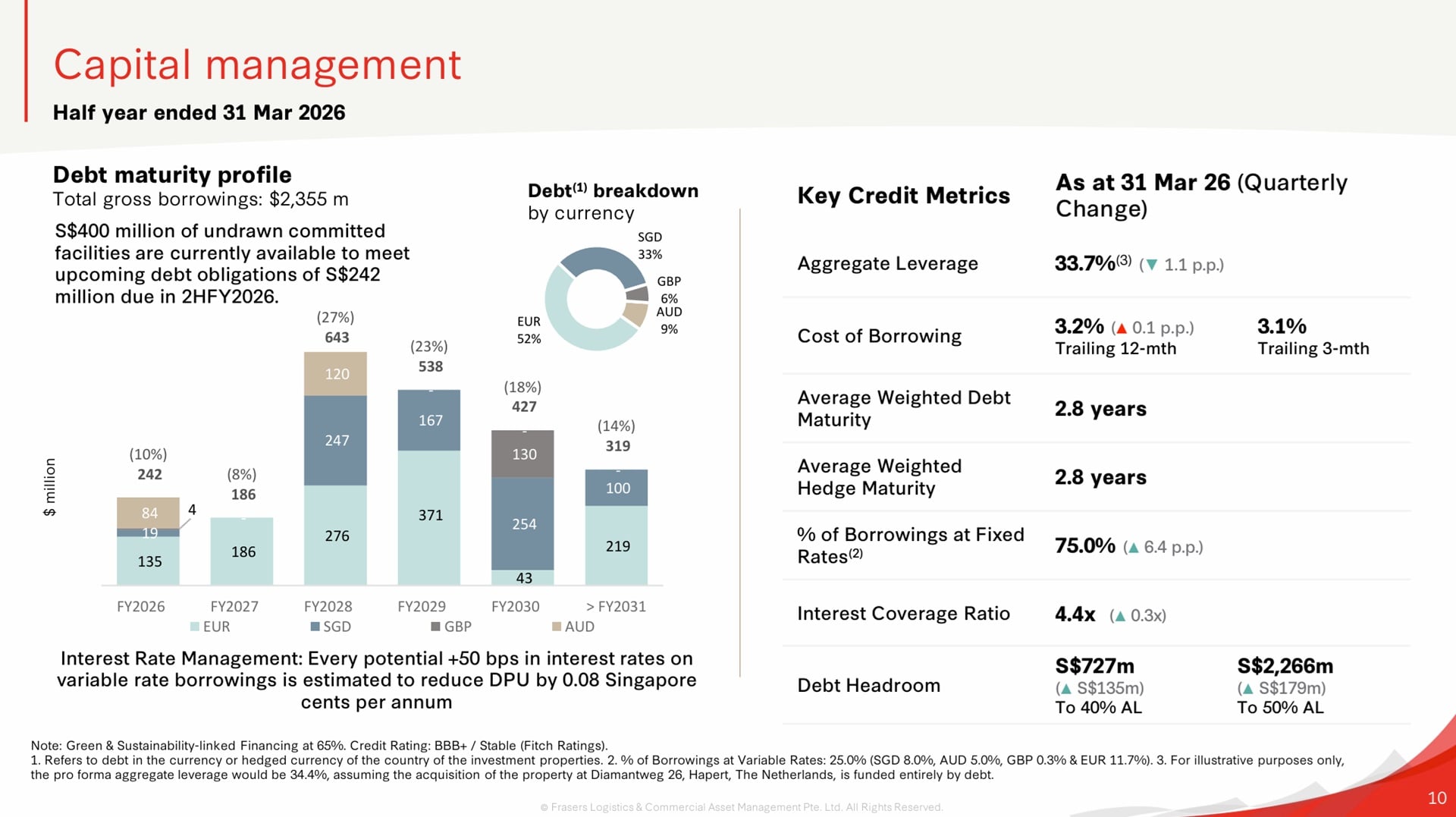

Capital management and balance sheet strength

FLCT continues to maintain a strong balance sheet, with aggregate leverage at 33.7%, comfortably below regulatory limits and providing ample debt headroom for future opportunities. The REIT’s cost of borrowing remains stable at around 3.2% on a trailing 12-month basis, with 75.0% of borrowings on fixed rates, which reduces exposure to interest rate volatility.

The REIT also has S$400 million in undrawn committed facilities, more than sufficient to cover the S$242 million of debt maturing in the second half of FY2026. Its interest coverage ratio stands at a healthy 4.4 times, indicating that earnings comfortably cover financing costs. FLCT also maintains an investment-grade credit rating of BBB+ with a stable outlook, which supports its access to capital markets at reasonable spreads.

Net asset value (NAV) per unit rose to S$1.12, up from S$1.10 as at 30 September 2025. This was supported by currency gains, capital expenditure and the resilience of asset valuations despite a higher interest rate environment. While cap rates have generally softened across global real estate, the structural appeal of prime logistics and industrial assets has helped to cushion valuation pressures.

Strategic acquisition in the Netherlands

FLCT recently completed a €43.0 million acquisition of a modern freehold logistics facility located at Diamantweg 26 in Hapert, the Netherlands. The property is fully leased to DSV Air & Sea Nederland B.V., a major global logistics operator, with a long WALE of 9.5 years. The acquisition was completed at a discount to independent valuation and is expected to be DPU-accretive.

This addition strengthens FLCT’s logistics and industrial portfolio and aligns with its strategy of increasing exposure to high-quality logistics assets in developed markets. The asset’s long lease tenure, strong tenant profile and strategic location near key transport routes make it a complementary and defensive addition to the portfolio.

Macroeconomic and market outlook

FLCT operates across Australia, Europe, Singapore and the UK, and the REIT’s outlook commentary reflects the varied conditions across these markets. Australia’s industrial sector remains resilient, supported by limited new supply and strong demand, although inflation and rising interest rates may temper occupier sentiment. Europe continues to see healthy logistics demand despite muted investment activity, while the UK logistics market remains stable with modest rental growth and gradually normalising vacancy levels.

In Singapore, business park demand remains subdued, with occupiers still rightsizing and consolidating, but logistics warehouse occupancy continues to improve, supported by sustained demand for modern ramp-up facilities and a relatively modest new supply pipeline. Across FLCT’s markets, the manager remains cautious about global risks, including geopolitical tensions, inflationary pressures and supply chain disruptions, but continues to see strong structural demand for logistics and industrial assets.

Personal take on Frasers Logistics and Commercial Trust 1HFY26 Financial Results as a unitholder

From the perspective of an investor with 7.09% of my stock portfolio allocated to FLCT, Frasers Logistics and Commercial Trust 1HFY26 Financial Results are broadly reassuring. The slight decline in headline DPU is not ideal, but the improvement in underlying distributable income before divestment gains suggests that the core engine of the REIT is still running well. The logistics and industrial portfolio continues to be the star performer, and the recent acquisition in the Netherlands further tilts the portfolio towards this resilient segment.

The main areas to watch are the commercial assets, particularly Alexandra Technopark and the UK business parks, where leasing momentum and occupancy will be key drivers of medium-term performance. Nonetheless, the strong balance sheet, disciplined capital management and visible rental growth embedded in the lease structure provide a solid foundation for long-term income generation.

Summary of Frasers Logistics and Commercial Trust 1HFY26 financial results

Based on Frasers Logistics and Commercial Trust 1HFY26 Financial Results, the pros of investing are:

- Strong rental reversions across the logistics and industrial portfolio, supporting organic income growth.

- High occupancy of 99.8% in logistics and industrial assets, reflecting resilient tenant demand.

- Healthy aggregate leverage of 33.7% with a stable cost of borrowing and high proportion of fixed-rate debt.

- Long WALE of 4.9 years with a large share of leases featuring fixed or CPI-linked escalations.

- DPU-accretive acquisition in the Netherlands that enhances portfolio quality and income visibility.

The cons are:

- Slight decline in overall DPU due to lower capital distributions from divestment gains.

- Commercial portfolio occupancy remains weaker at 88.4%, particularly in business park and office assets.

- Higher vacancies and ongoing backfilling efforts at assets such as Alexandra Technopark.

- Exposure to macroeconomic risks including inflation, interest rate volatility and currency movements across multiple markets.