Mapletree Logistics Trust (MLT) has released its 4Q FY25/26 financial results, and the overall picture is one of resilience in a difficult environment. As an investor, MLT currently makes up 3.72% of my stock portfolio in terms of amount invested, so every set of results matters to me not just as numbers on a page, but as a direct driver of my long-term income and capital growth. The recent report on the Mapletree Logistics Trust 4Q FY25/26 Financial Results highlights this resilience.

The Mapletree Logistics Trust 4Q FY25/26 Financial Results demonstrate the Trust’s commitment to maintaining investor confidence and showcasing its operational resilience.

The quarter was shaped by familiar challenges: weaker regional currencies, higher interest rates and the ongoing impact of earlier divestments. Yet, beneath the headline declines in revenue and distribution per unit (DPU), the underlying operations remained steady. When we strip out non-recurring divestment gains and currency swings, MLT’s core engine continues to run reliably, which is exactly what income investors look for in a logistics REIT.

Understanding the Mapletree Logistics Trust 4Q FY25/26 Financial Results is crucial for investors looking to make informed decisions.

Top line and NPI: small declines, but core growth underneath

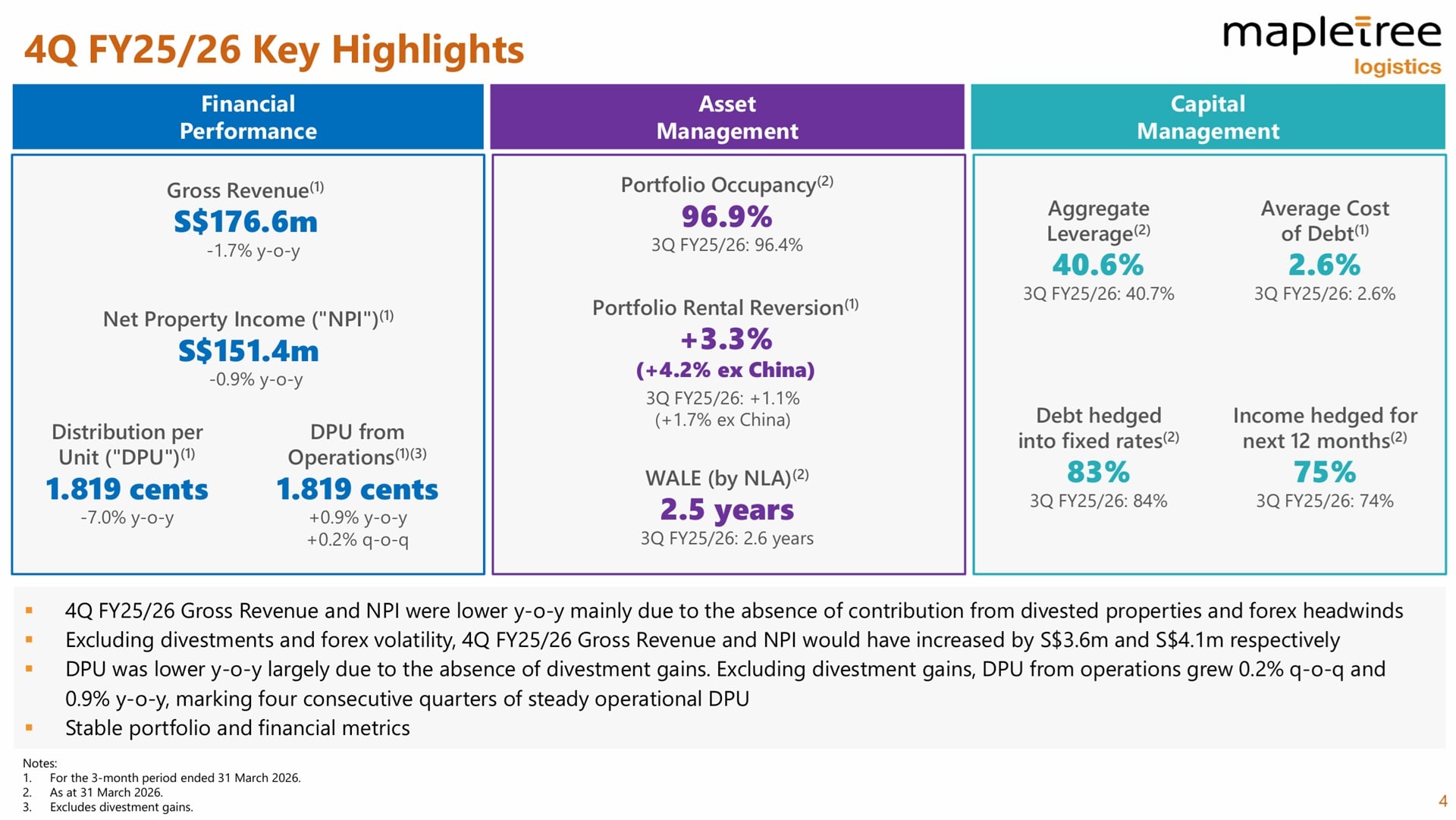

For the three months ended 31 March 2026, MLT reported gross revenue of about S$176.6 million, a modest year-on-year decline of 1.7%. Net property income (NPI) dipped slightly by 0.9% to around S$151.4 million. At first glance, this might look like a soft quarter, but the drivers matter. The main drag came from the absence of contributions from properties that were divested in earlier periods, as well as the impact of weaker regional currencies against the Singapore dollar.

The implications of the Mapletree Logistics Trust 4Q FY25/26 Financial Results extend beyond immediate numbers and reflect long-term trends in the logistics sector.

The detailed analysis of the Mapletree Logistics Trust 4Q FY25/26 Financial Results provides insights into the operational performance and future outlook.

In-depth analysis of the Mapletree Logistics Trust 4Q FY25/26 Financial Results reveals important insights for current and prospective investors.

Management indicated that if we adjust for divestments and currency volatility, both revenue and NPI would actually have grown. In other words, the properties that remain in the portfolio are generating higher income than before, and the completed redevelopment project in Singapore has started to contribute meaningfully. This is an important nuance: the REIT is not shrinking in quality, but pruning older assets and reinvesting into stronger ones.

For the full year FY25/26, gross revenue came in at about S$708.3 million, down 2.6% year-on-year, while NPI fell 2.4% to roughly S$610.2 million. Again, divestments and currency translation losses were the main reasons for the decline. Adjusted for these factors, the portfolio would have delivered higher revenue and NPI, underscoring the resilience of the underlying operations.

The overview of the Mapletree Logistics Trust 4Q FY25/26 Financial Results indicates that despite challenges, the fundamentals remain strong.

DPU: headline decline, but operational distributions remain steady

The available DPU for 4Q FY25/26 was 1.819 cents, about 7.0% lower than the same quarter a year ago. For the full year, DPU was 7.262 cents, a 9.8% decline. On the surface, this may concern income investors who rely on stable or growing distributions. However, the comparison is distorted by the fact that in the previous financial year, MLT distributed divestment gains on top of its recurring income.

Analyzing the DPU in the context of the Mapletree Logistics Trust 4Q FY25/26 Financial Results gives a clearer picture of operational performance.

Once we exclude those one-off divestment gains, the picture improves significantly. Operational DPU for the quarter actually grew year-on-year, and the REIT has now delivered four consecutive quarters of steady DPU from operations. For the full year, operational DPU was slightly lower, reflecting the cumulative impact of divestments and currency weakness, but the decline was far more modest than the headline number suggests.

As an investor, I see this as a reminder to look beyond headline DPU and focus on recurring cash flow. MLT’s ability to maintain and even grow operational distributions in a tough environment is a positive signal for long-term sustainability.

Investors should take the time to evaluate the Mapletree Logistics Trust 4Q FY25/26 Financial Results for a comprehensive understanding of investment potential.

Portfolio quality: high occupancy and positive rental reversions

The visual data accompanying the Mapletree Logistics Trust 4Q FY25/26 Financial Results support the narrative of stability and growth.

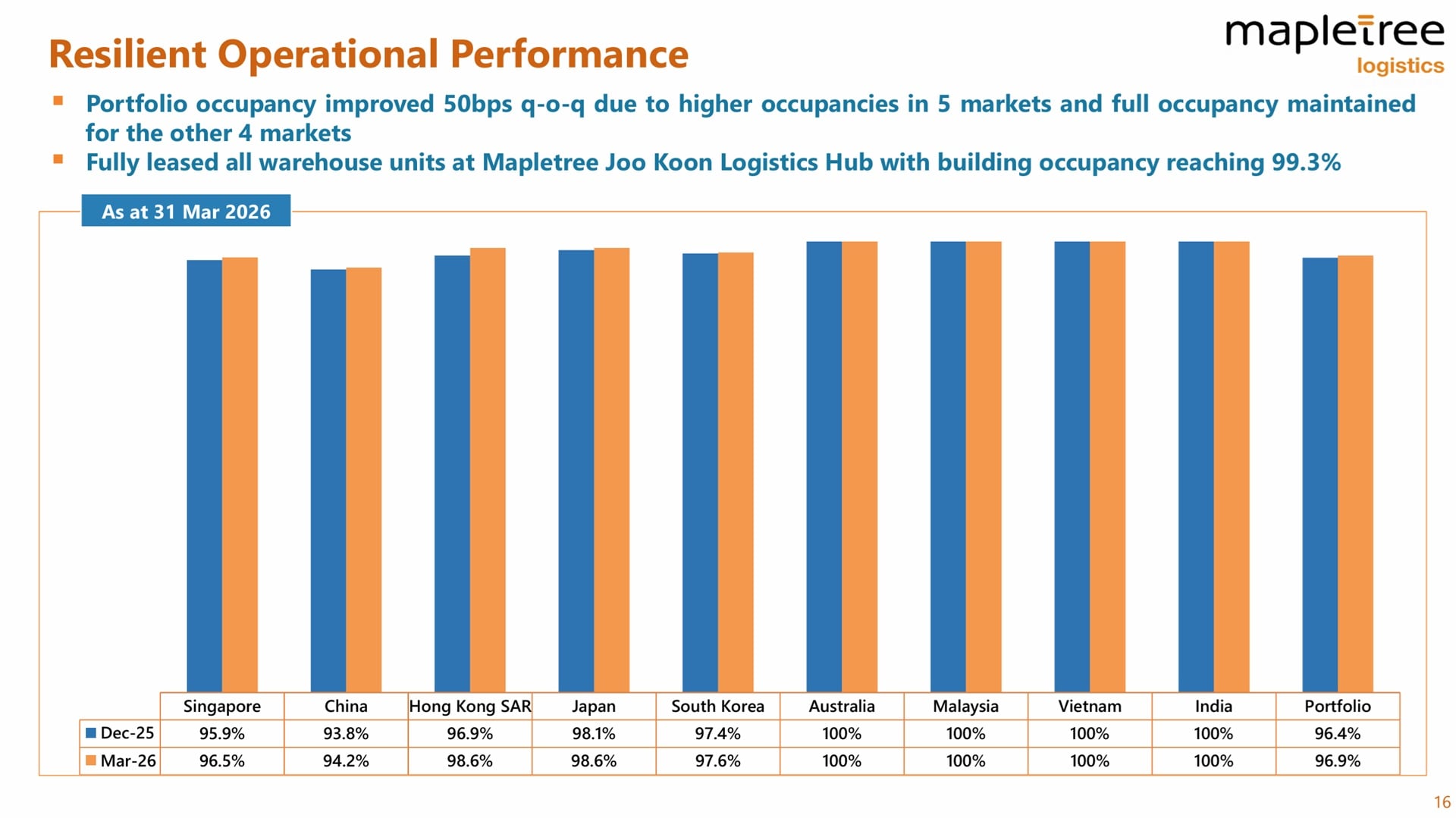

Operationally, the portfolio remains in good shape. As at 31 March 2026, portfolio occupancy improved to 96.9%, up from 96.4% in the previous quarter. Occupancy rose in key markets such as Singapore, China, Hong Kong SAR, Japan and South Korea, while Australia, Malaysia, Vietnam and India maintained full occupancy. This broad-based strength across nine markets helps to smooth out country-specific volatility.

Rental reversions were another bright spot. For 4Q FY25/26, the portfolio achieved an average positive rental reversion of about 3.3%, and around 4.2% if China is excluded. Most markets saw positive rental growth, with China being the only exception. Even there, the negative rental reversion continued to narrow compared to previous quarters, suggesting that conditions may be stabilising.

The positive rental reversions highlighted in the Mapletree Logistics Trust 4Q FY25/26 Financial Results add to the trust’s investment appeal.

The weighted average lease expiry (WALE) of the portfolio stands at around 2.5 years. This provides a balanced lease profile: not so short that income visibility is at risk, but not so long that the REIT is locked into outdated rental levels. With a diversified tenant base of nearly a thousand customers across consumer, logistics, e-commerce and industrial sectors, concentration risk remains well managed.

Active portfolio rejuvenation: accretive acquisition and value-unlocking divestments

Active portfolio management is a key takeaway from the Mapletree Logistics Trust 4Q FY25/26 Financial Results, demonstrating strategic foresight.

One of the key themes for MLT in recent years has been active portfolio rejuvenation, and FY25/26 continued that trajectory. During the year, the REIT completed the acquisition of a freehold Grade A warehouse in Bhiwandi, Mumbai, for about S$53.2 million. The asset is fully leased to two leading online food and grocery delivery companies in India, with a weighted average lease expiry of close to four years and built-in rental escalations. This acquisition deepens MLT’s presence in India, a fast-growing logistics market with strong structural demand from e-commerce and consumption.

On the flip side, MLT divested six properties across Singapore, Malaysia, South Korea and Australia. These assets generally had older specifications or limited redevelopment potential. Importantly, the divestments were executed at an average premium of around 20% above their latest valuations, unlocking value for unitholders and freeing up capital for reinvestment into higher-quality, higher-growth assets.

Through the lens of the Mapletree Logistics Trust 4Q FY25/26 Financial Results, we see a proactive approach to asset management.

This disciplined recycling of capital is central to MLT’s long-term strategy. Rather than simply growing for the sake of size, the REIT is gradually upgrading its portfolio, improving asset quality, tenant mix and earnings visibility.

Valuation, balance sheet and hedging: steady and conservative

The valuation insights within the Mapletree Logistics Trust 4Q FY25/26 Financial Results reveal the trust’s cautious yet confident market stance.

As at 31 March 2026, MLT’s portfolio valuation stood at about S$13.1 billion, down 1.6% year-on-year. The decline was mainly due to the divestment of six properties and a sizeable currency translation loss of roughly S$325 million. These were partially offset by a net fair value gain of S$47.8 million, contributions from the completed redevelopment project, capital expenditure and the India acquisition. Most markets recorded valuation gains, with the exception of China and Hong Kong SAR.

On the capital management front, MLT continues to operate with a prudent balance sheet. Aggregate leverage is at 40.6%, which is comfortably within regulatory limits and leaves room for future acquisitions or redevelopment opportunities. The weighted average borrowing cost remains low at around 2.6%, supported by proactive refinancing and the use of divestment proceeds to pay down debt.

Understanding the balance sheet metrics from the Mapletree Logistics Trust 4Q FY25/26 Financial Results can guide prudent investment decisions.

Interest rate and currency risks are actively managed. About 83% of total debt is either hedged or drawn at fixed rates, limiting the impact of further interest rate volatility. On the income side, roughly 75% of distributable income for the next 12 months has been hedged or is naturally derived in Singapore dollars, reducing the impact of currency swings on distributions.

Sustainability and long-term positioning

The sustainability measures outlined in the Mapletree Logistics Trust 4Q FY25/26 Financial Results reflect a commitment to long-term viability.

Beyond financial metrics, MLT continues to make progress on its sustainability agenda. The REIT is targeting carbon neutrality for Scope 1 and 2 emissions by 2030, aligned with its sponsor’s longer-term net-zero ambitions. During FY25/26, it expanded its self-funded rooftop solar capacity significantly and now has total installed solar capacity of more than 130 MWp across its portfolio, the largest reported among Singapore REITs.

More properties have also obtained green building certifications, lifting the proportion of green-certified space to about two-thirds of the portfolio by gross floor area. These initiatives are not just about branding; they can enhance asset competitiveness, attract quality tenants, reduce operating costs and support long-term valuation resilience.

The initiatives highlighted in the Mapletree Logistics Trust 4Q FY25/26 Financial Results enhance the trust’s competitive edge.

My take as an investor

With MLT forming 3.72% of my portfolio, I view these results as broadly reassuring. The headline declines in revenue and DPU are understandable given divestments and currency headwinds, but the underlying operational performance remains solid. Occupancy is high, rental reversions are positive in most markets, and the REIT continues to recycle capital into better assets while maintaining a conservative balance sheet.

The insights gained from the Mapletree Logistics Trust 4Q FY25/26 Financial Results reinforce the importance of a diversified investment strategy.

The key risks to watch are prolonged currency weakness, higher-for-longer interest rates and any deterioration in demand for logistics space, particularly in China. However, MLT’s diversified geographic footprint, strong tenant base and disciplined capital management provide a reasonable buffer against these uncertainties.

For long-term income investors who can tolerate some volatility in reported numbers due to forex and one-off items, MLT still looks like a credible core holding in the Asia-Pacific logistics space.

Investors must look closely at the Mapletree Logistics Trust 4Q FY25/26 Financial Results to gauge future growth prospects.

Summary of Mapletree Logistics Trust 4Q FY25/26 financial results

Based on Mapletree Logistics Trust 4Q FY25/26 financial results, the pros are:

By examining the Mapletree Logistics Trust 4Q FY25/26 Financial Results, we can identify both strengths and areas for improvement.

- Resilient underlying operations with stable NPI and four consecutive quarters of steady operational DPU despite macro headwinds.

- High portfolio occupancy of 96.9% and generally positive rental reversions across most markets, supporting income visibility.

- Active portfolio rejuvenation through accretive acquisition in Mumbai and divestment of older assets at attractive premiums to valuation.

- Conservative balance sheet with 40.6% leverage, low average borrowing cost of about 2.6% and strong interest rate and forex hedging.

- Ongoing sustainability initiatives, including large installed solar capacity and growing proportion of green-certified properties, enhance long-term competitiveness.

The cons are:

The cons highlighted in the Mapletree Logistics Trust 4Q FY25/26 Financial Results warrant consideration for risk-averse investors.

-

- Headline DPU declined year-on-year due to absence of divestment gains and currency translation losses, which may concern investors focused solely on reported distributions.

- Continued currency volatility in key markets such as Japan, China and Hong Kong SAR can weigh on reported earnings and valuations.

- Exposure to China remains a drag on rental reversions, and a slower recovery there could cap near-term growth.

The challenges noted in the Mapletree Logistics Trust 4Q FY25/26 Financial Results illustrate the complexities of the logistics market.

-

- Higher-for-longer interest rates, if they persist, could gradually increase financing costs once existing hedges roll off.

Overall, the Mapletree Logistics Trust 4Q FY25/26 Financial Results provide a comprehensive overview of the trust’s current standing and future outlook.