OUE REIT has kicked off 2026 with a set of financial results that reflect resilience, strategic clarity and disciplined execution across its diversified portfolio. For investors watching the Singapore REIT landscape closely, the latest update offers a clear view of how the trust is positioning itself for the next phase of growth while navigating a still-uncertain macroeconomic environment. As someone who holds OUE REIT as 1.72% of my overall stock portfolio in terms of amount invested, these results provide useful insight into how the REIT is performing operationally and financially, and whether its long-term strategy continues to justify its place in my holdings. As part of the analysis of the OUE REIT 1Q 2026 Financial Results, it’s important to consider the broader context of the real estate market.

The first quarter of 2026 saw OUE REIT deliver higher revenue, stronger net property income and a meaningful reduction in financing costs. These improvements were supported by a combination of resilient commercial performance, strong hospitality recovery and the REIT’s maiden expansion into Australia through its acquisition of a 19.9% interest in 180 George Street, also known as Salesforce Tower in Sydney. The trust’s ability to grow income while lowering borrowing costs is particularly noteworthy given the interest rate environment of the past few years, and it signals that management’s capital management strategy is beginning to bear fruit. These results contribute to our understanding of the OUE REIT 1Q 2026 Financial Results and their implications for future performance.

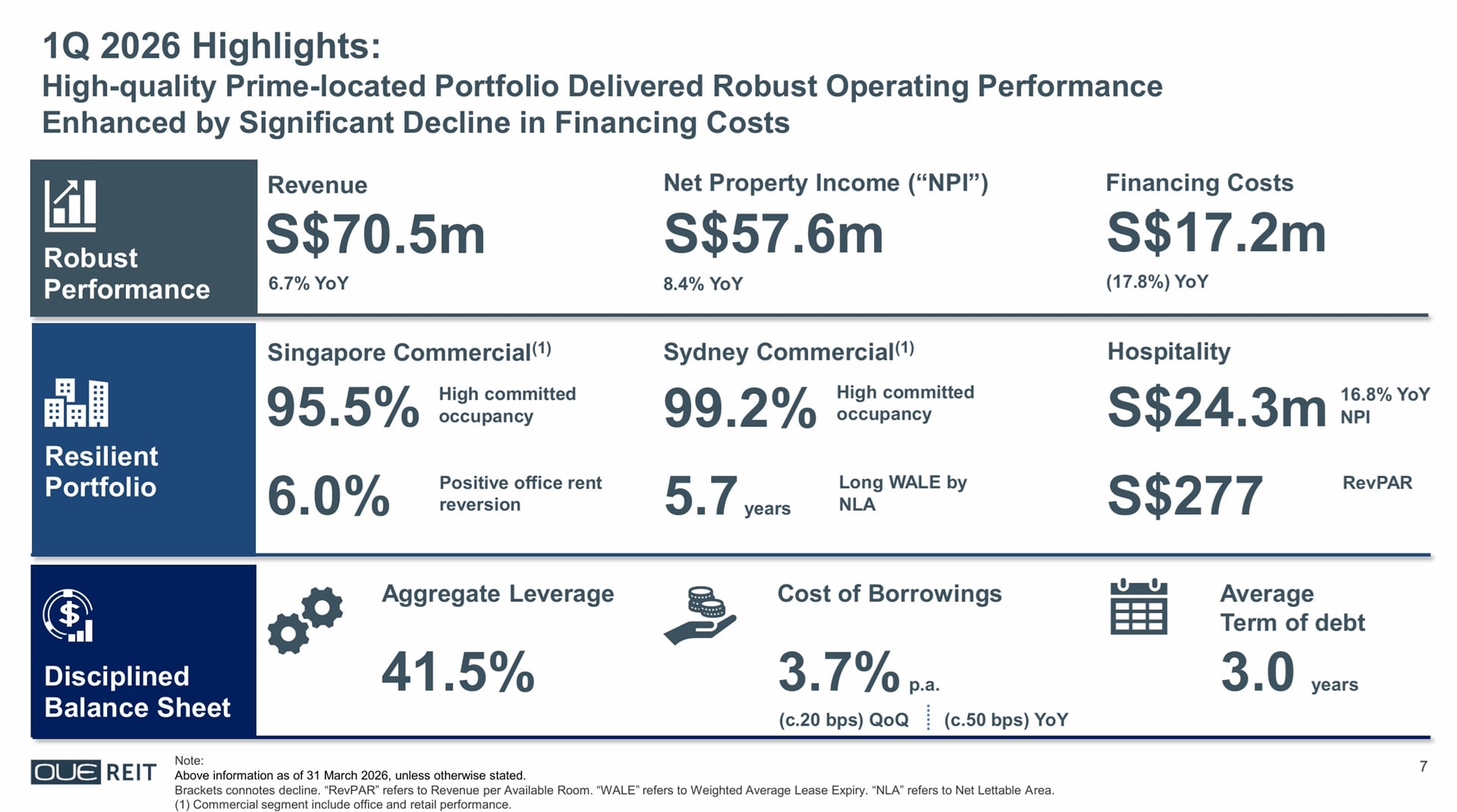

Revenue for the quarter rose to S$70.5 million, representing a 6.7 percent year-on-year increase. Net property income grew even faster at 8.4 percent year-on-year to S$57.6 million, reflecting improved operating leverage and stronger contributions from both the commercial and hospitality segments. The hospitality segment, in particular, delivered double-digit growth as Singapore’s tourism and MICE activity continued to recover. Meanwhile, the commercial portfolio remained stable with positive rental reversions and high occupancy across its Singapore office assets.

One of the standout achievements in the quarter was the 17.8 percent year-on-year decline in financing costs. This improvement was driven by proactive refinancing efforts completed in 2025 and the benefit of a gradually easing interest rate environment. With the weighted average cost of debt falling to 3.7 percent per annum, OUE REIT is now in a stronger position to preserve distributable income even as it continues to invest in growth opportunities. The interest coverage ratio also improved to 2.6 times, comfortably above regulatory and banking thresholds.

The acquisition of 180 George Street in Sydney marks a significant milestone for OUE REIT as it expands beyond Singapore into another major gateway city. The asset is a premium freehold commercial tower located in Sydney’s core CBD, with a near-full committed occupancy of 99.2 percent and a long weighted average lease expiry of more than five years. Its tenant mix is anchored by high-quality occupiers in technology, financial services and professional services, which aligns well with the REIT’s existing commercial portfolio. The acquisition was funded through capital redeployment from the divestment of Lippo Plaza Shanghai, demonstrating management’s disciplined approach to recycling capital from mature assets into higher-quality, higher-growth opportunities.

Back in Singapore, the REIT continues to unlock value from its existing assets. OUE Bayfront received planning approval to convert Level 17 into more than 22,600 square feet of new prime office space. With an estimated capital expenditure of up to S$43 million, the project is expected to generate a stabilised return on investment exceeding 11 percent. This kind of asset enhancement initiative is a key part of OUE REIT’s Phase 3 Value Creation Journey, which focuses on disciplined capital allocation and long-term value creation for unitholders.

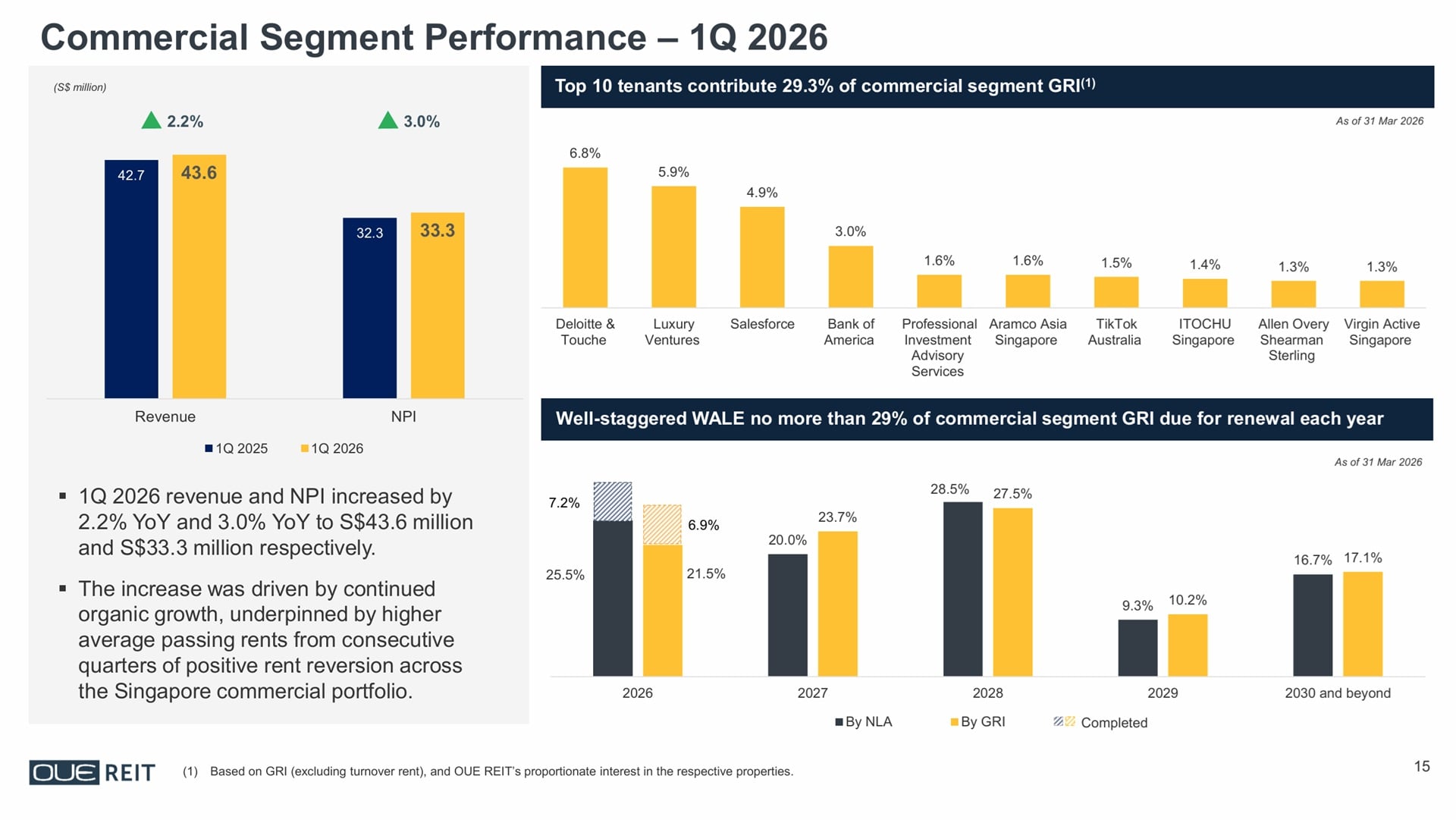

The commercial segment, comprising both office and retail assets, delivered stable performance in the first quarter. Revenue rose to S$43.6 million, supported by higher average passing rents and continued positive rental reversions across the Singapore office portfolio. Committed occupancy remained high at 95.2 percent, and rental reversion for office leases came in at a positive 6.0 percent. These figures reflect the ongoing strength of Singapore’s Grade A office market, which continues to benefit from tightening supply, strong demand from financial services and technology firms, and a broader flight-to-quality trend among occupiers.

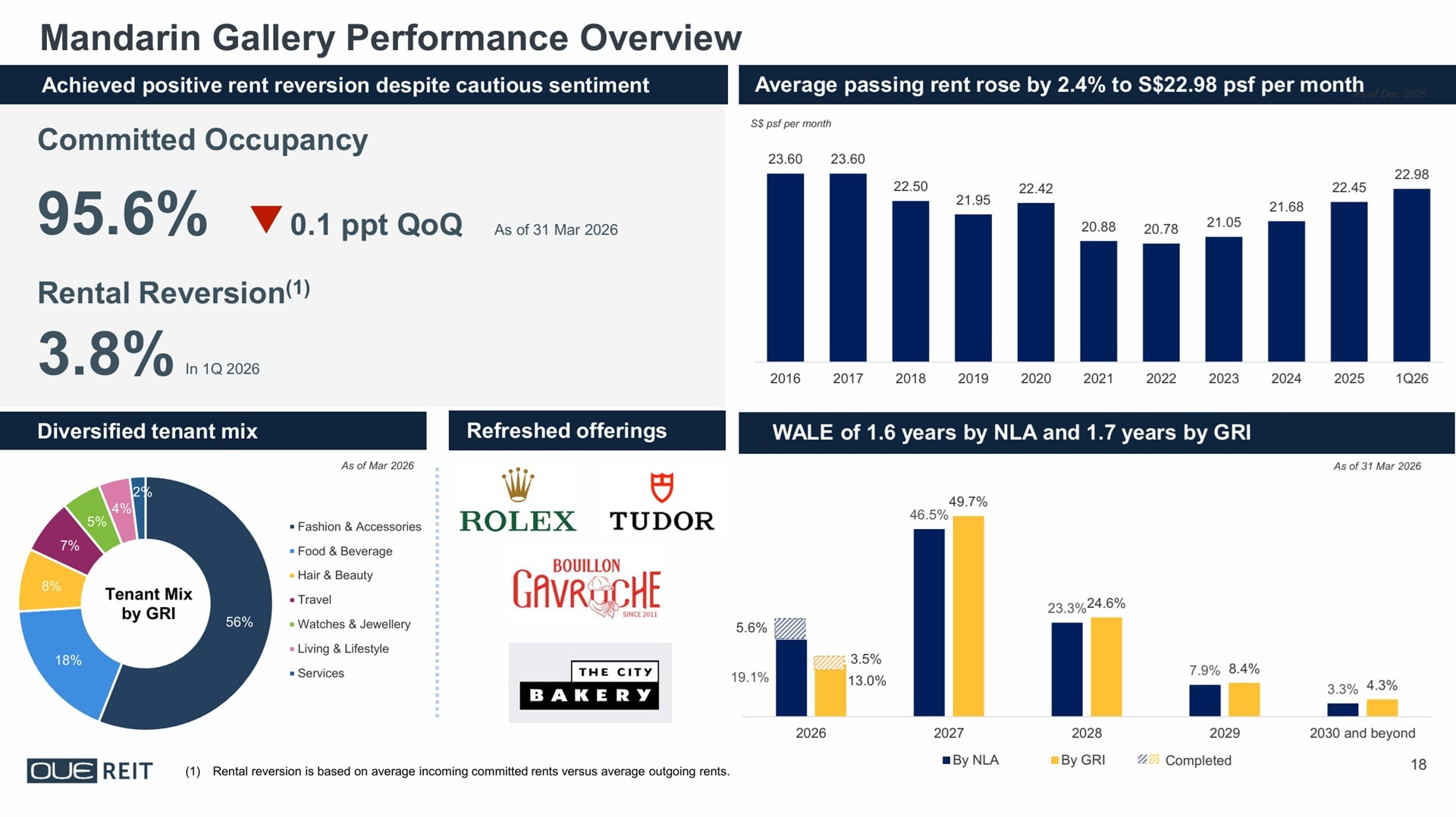

Mandarin Gallery, the REIT’s retail asset along Orchard Road, also maintained stable operating metrics despite a cautious retail environment. The mall achieved a positive rental reversion of 3.8 percent and saw its average passing rent rise to S$22.98 per square foot per month. The tenant mix remains well-diversified, and the mall continues to refresh its offerings to stay relevant amid evolving consumer preferences.

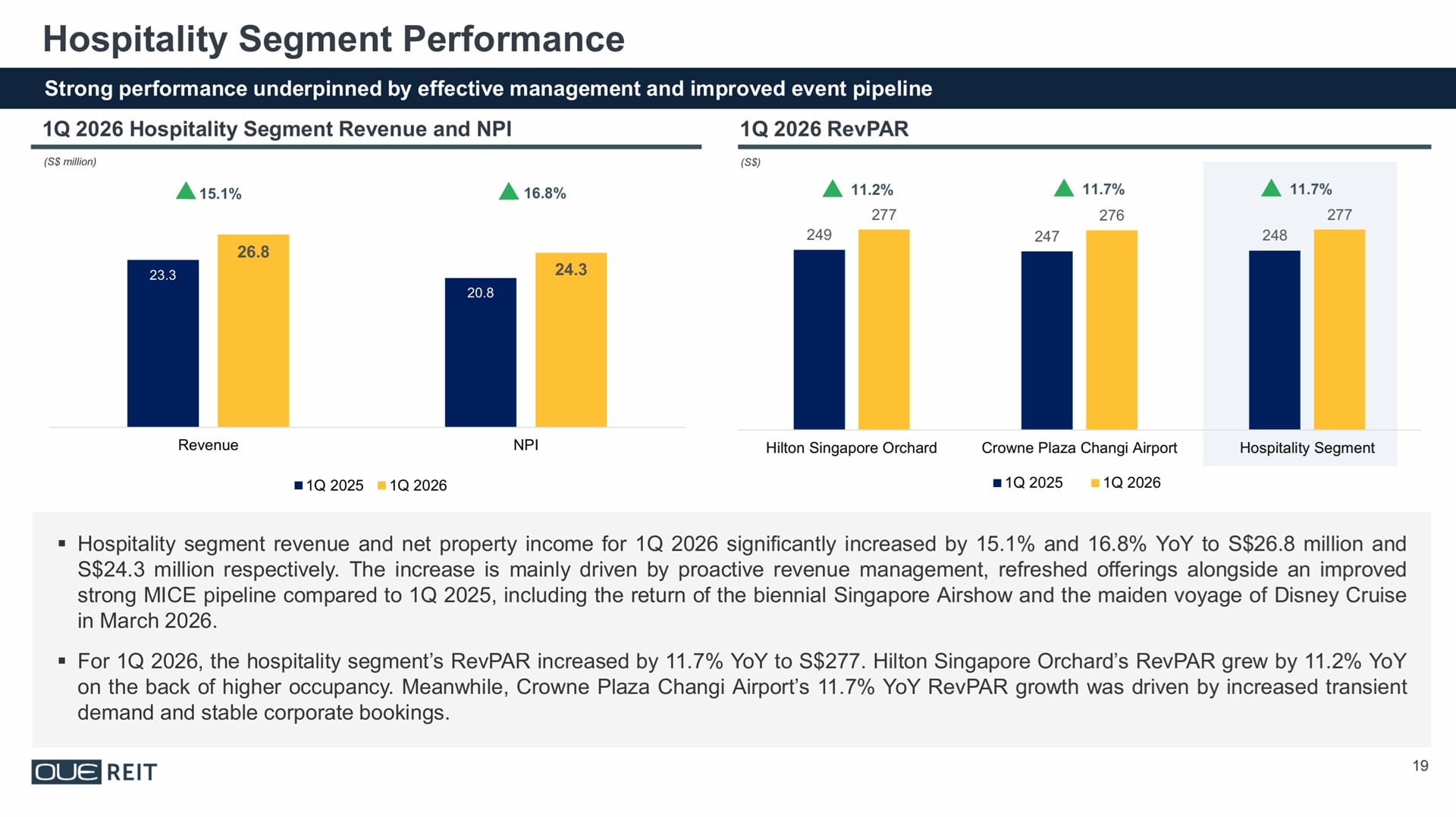

The hospitality segment was the strongest performer in the quarter. Revenue rose to S$26.8 million, while net property income increased to S$24.3 million. Revenue per available room for the segment grew by 11.7 percent year-on-year to S$277, supported by higher occupancy and stronger transient demand. Hilton Singapore Orchard and Crowne Plaza Changi Airport both recorded double-digit growth in room revenue metrics, benefiting from a robust events calendar that included the Singapore Airshow and the maiden voyage of Disney Cruise. With international visitor arrivals rising and hotel supply growth remaining modest, the hospitality segment is well-positioned to continue its recovery through the rest of 2026.

On the balance sheet front, aggregate leverage increased to 41.5 percent following the acquisition of 180 George Street and drawdowns for distribution payments. While this level of gearing is higher than the previous quarter, it remains within regulatory limits and is supported by a well-staggered debt maturity profile. Not more than roughly a fifth of total debt is due in any single year, and the REIT continues to maintain a high proportion of unsecured and green financing. The trust’s investment-grade credit rating of BBB- with a stable outlook further enhances its financial flexibility.

Looking ahead, OUE REIT’s outlook is supported by favourable market conditions in both Singapore and Sydney. In Singapore, the Grade A office market continues to see tightening supply, with no new major completions expected in the Core CBD until 2028. This supply-demand imbalance is expected to support rental growth of around five percent for 2026. The hospitality sector also stands to benefit from a strong pipeline of events and concerts, as well as stabilised hotel supply along Orchard Road.

In Sydney, the CBD office market is experiencing improving operating metrics, with rising prime rents and increasing occupancy driven by flight-to-quality trends. New supply is limited in the near term, and leasing interest remains strong for developments completing from 2027 onward. These conditions provide a supportive backdrop for OUE REIT’s newly acquired interest in 180 George Street and help diversify the REIT’s income base beyond Singapore.

From a portfolio construction perspective, OUE REIT’s 1Q 2026 results reflect a REIT that is executing well on its strategic priorities while maintaining operational resilience across its diversified portfolio. The combination of income growth, cost savings, asset enhancements and strategic expansion positions the trust for continued performance in the coming quarters. For investors like myself, who hold OUE REIT as a modest portion of a broader portfolio, the latest results reinforce the REIT’s role as a stable, income-generating asset with potential for long-term value creation, while still requiring close monitoring of leverage and macro risks.

Summary of OUE REIT 1Q 2026 Financial Results

Based on OUE REIT 1Q 2026 financial results, below are the pros and cons of investing into OUE REIT.

Pros

- Strong year-on-year growth in revenue, net property income and hospitality performance.

- Significant reduction in financing costs, improving distributable income stability.

- High occupancy across commercial and hospitality assets with positive rental reversions.

- Strategic expansion into Sydney with a high-quality freehold office asset.

- Asset enhancement initiatives with attractive projected returns on investment.

- Well-diversified portfolio across office, retail and hospitality segments in prime locations.

Cons

- Higher aggregate leverage following the acquisition of 180 George Street.

- Retail environment remains cautious despite stable performance at Mandarin Gallery.

- Hospitality recovery is dependent on tourism flows and event activity, which can be cyclical.

- Future interest rate increases could impact borrowing costs despite current improvements.