Mapletree Pan Asia Commercial Trust (MPACT) has released its FY25/26 financial results, and the year stands out as one defined by strategic reshaping, disciplined capital management and the growing dominance of its Singapore portfolio. As an investor with 6.31% of my stock portfolio allocated to MPACT, I follow its developments closely, especially in a period marked by shifting macroeconomic conditions and uneven performance across Asia’s commercial real estate markets. The results for the year, titled ‘Mapletree Pan Asia Commercial Trust FY25/26 Financial Results’, were not a year of dramatic expansion, but it was one where the trust reinforced its foundations and positioned itself more defensively for the future. The Mapletree Pan Asia Commercial Trust FY25/26 Financial Results indicate a commitment to long-term stability and growth.

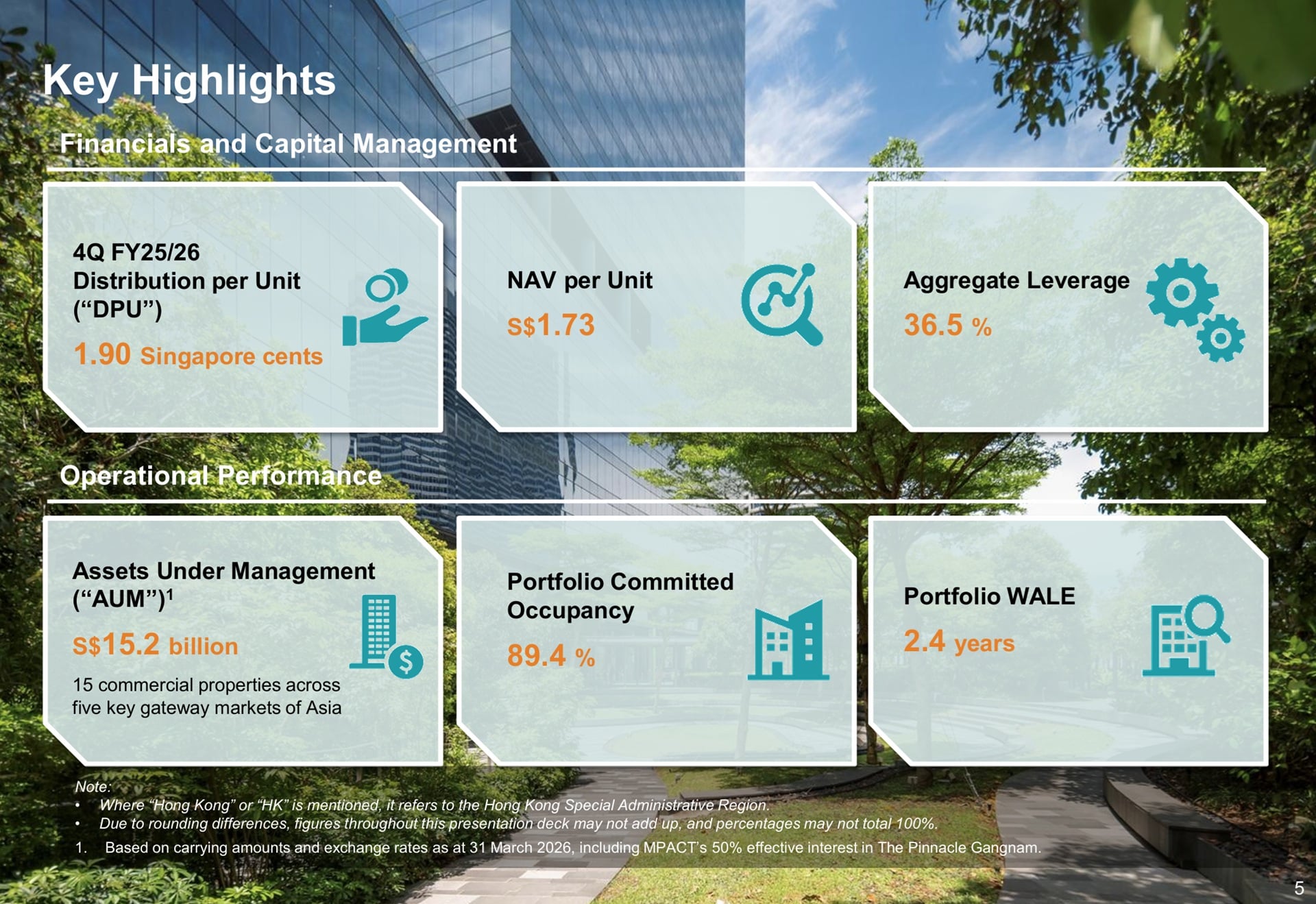

The trust delivered a full‑year Distribution per Unit (DPU) of 7.97 Singapore cents, slightly lower than the previous year’s 8.02 cents. This decline was driven by a one‑off tax charge of S$8.3 million related to the divestment of the office component of Festival Walk. Without this charge, the underlying DPU would have been 8.11 cents, representing a 1.1% increase year‑on‑year. This underlying growth is significant because it shows that the trust’s core operations generated stronger distributable income despite challenges in overseas markets.

Singapore Assets Continue to Drive Performance

Singapore remains the anchor of MPACT’s portfolio, and FY25/26 reinforced its importance. On a comparable basis, Singapore’s gross revenue rose 2.3%, while net property income (NPI) increased 4.1%, even after excluding Mapletree Anson, which was divested earlier in the year. This growth was led by VivoCity and Mapletree Business City (MBC), both of which continue to demonstrate strong tenant demand and resilient operating metrics.

The Mapletree Pan Asia Commercial Trust FY25/26 Financial Results highlight the trust’s strategic focus and the resilience of its Singapore assets during challenging market conditions.

VivoCity delivered one of its strongest performances in recent years. Full‑year NPI grew 7.6%, supported by the completion of its basement 2 asset enhancement initiative (AEI). This AEI added 14,000 square feet of retail space and is generating an ROI of over 10%. Shopper traffic rose to 45.4 million, up 3.6% year‑on‑year, while tenant sales reached S$1.1 billion, reflecting the mall’s continued appeal as a major retail destination. Rental reversion for the year came in at 14.1%, and the mall maintained near‑full committed occupancy throughout the period.

MBC also contributed to the trust’s stability. Key top‑ten tenant renewals were secured during the year, reinforcing income visibility and extending the weighted average lease expiry (WALE). The overall portfolio WALE improved to 2.4 years, with the office and business park segment at 2.9 years. These renewals demonstrate the continued relevance of MBC as a high‑quality business park asset in Singapore’s competitive office landscape.

This focus is evident in the Mapletree Pan Asia Commercial Trust FY25/26 Financial Results which show a strong commitment to maintaining a high-quality portfolio.

Singapore now accounts for 61% of total assets under management and 66% of NPI, reflecting the trust’s strategic emphasis on strengthening its core market. This shift toward Singapore has helped cushion the impact of weaker performance in overseas markets.

Overseas Markets Face Operational and Currency Challenges

The challenges faced by overseas markets, as reflected in the Mapletree Pan Asia Commercial Trust FY25/26 Financial Results, emphasize the importance of the trust’s Singapore assets.

While Singapore delivered growth, the overseas portfolio faced a combination of operational softness and foreign exchange pressures. Gross revenue and NPI from overseas assets declined due to weaker market conditions in Greater China and Japan, as well as the absence of contributions from three divested assets: TS Ikebukuro Building, ABAS Shin‑Yokohama Building and Festival Walk Tower.

Festival Walk in Hong Kong maintained 100% committed occupancy, but full‑year tenant sales dipped slightly by 0.8%. However, the final quarter of the year saw a 6.0% rebound in tenant sales, driven by increased spending on luxury items. The mall is undergoing a reconfiguration of 18,800 square feet of space into a multi‑concept F&B and lifestyle cluster. This project is expected to deliver a projected ROI of nearly 50% upon completion in 2Q FY26/27, making it one of the most ambitious enhancement initiatives in the trust’s portfolio.

In China, softer market rents and cautious business sentiment weighed on performance. Japan’s occupancy was affected by the expiry of Fujitsu’s lease at the Makuhari building, although the market has begun to absorb the vacancy. These challenges reflect broader economic conditions in the region, where recovery has been uneven and demand for commercial space remains subdued in certain submarkets.

Foreign exchange movements had a significant impact on valuations. The stronger Singapore dollar resulted in a S$301.1 million negative FX impact on overseas assets. Excluding this, the portfolio valuation would have been almost flat, declining only 0.2% year‑on‑year. This demonstrates that the operational performance of the overseas assets, while softer, was not the primary driver of valuation declines.

The impact of foreign exchange movements on valuations, as discussed in the Mapletree Pan Asia Commercial Trust FY25/26 Financial Results, illustrates the importance of strategic planning.

Strategic Divestments Strengthen the Balance Sheet

FY25/26 was a year of deliberate reshaping for MPACT. The trust completed three divestments, and the net proceeds were channelled directly into debt reduction. This strategy has meaningfully strengthened the balance sheet and improved financial resilience.

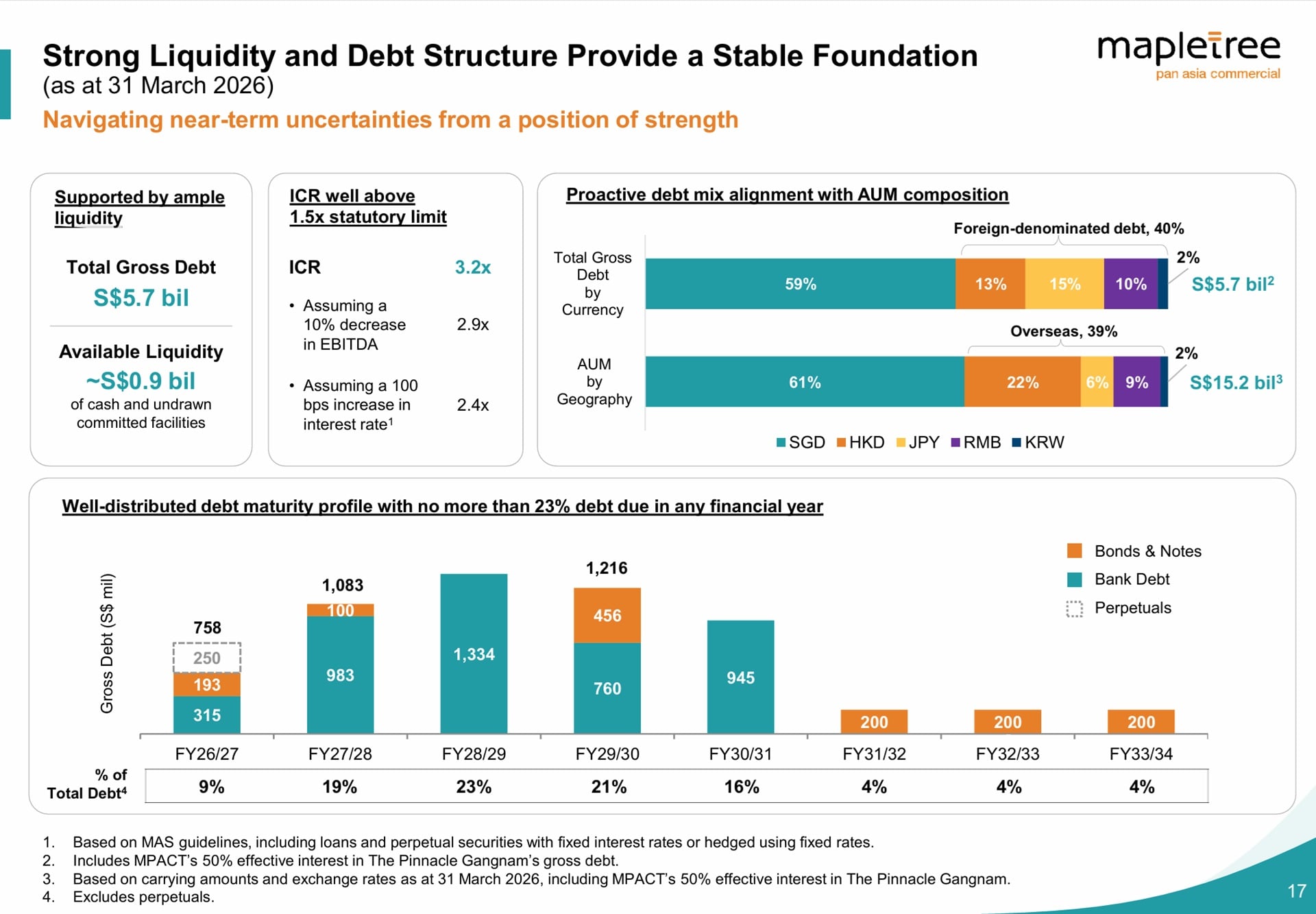

Aggregate leverage fell to 36.5%, down from 37.7% a year ago. The weighted average all‑in cost of debt declined to 3.16%, compared to 3.51% previously. Interest coverage improved to 3.2 times, comfortably above regulatory requirements. These improvements were driven by lower interest rates on SGD and HKD borrowings, as well as reduced debt levels following the divestments.

The financial metrics outlined in the Mapletree Pan Asia Commercial Trust FY25/26 Financial Results reflect a commitment to maintaining a robust balance sheet.

MPACT now has S$0.9 billion in available liquidity, and 75.1% of its debt is either fixed or hedged. Approximately 95% of distributable income is generated in or hedged into SGD, significantly reducing exposure to currency volatility. The trust’s debt maturity profile is well‑spread, with no single financial year accounting for more than 23% of refinancing needs. This reduces refinancing risk in an environment where interest rates remain uncertain.

Portfolio Valuation: Singapore Offsets Overseas Declines

The performance of Singapore assets, highlighted in the Mapletree Pan Asia Commercial Trust FY25/26 Financial Results, provides a basis for optimism moving forward.

MPACT’s total portfolio valuation stands at S$15.2 billion, down 2.1% year‑on‑year. Singapore assets saw a S$278 million uplift, driven largely by VivoCity’s strong performance and valuation increase of 5.4%. The remaining Singapore assets held steady, reflecting their stability and continued demand.

Overseas assets saw a S$301.7 million operational decline, compounded by the S$301.1 million FX impact. Excluding FX, the portfolio would have been broadly stable. Net asset value (NAV) per unit is S$1.73, down from S$1.78, primarily due to FX translation losses rather than operational weakness.

Operational Metrics Reflect Stability and Discipline

MPACT renewed or re‑let 3.0 million square feet of space during the year, including 1.5 million square feet of leases expiring in FY25/26. Portfolio committed occupancy improved quarter‑on‑quarter to 89.4%, supported by leasing momentum at MBC.

Rental reversion for the full year was flat, reflecting a strategic focus on tenant retention and occupancy stability in softer overseas markets. This approach prioritises long‑term cash flow resilience over short‑term rental gains, which is prudent given the current macroeconomic environment.

The trust’s diversified tenant base and strong Singapore weighting continue to provide resilience. The renewal of another top‑ten tenant at MBC in the final quarter further reinforces income visibility.

Looking Ahead: A More Focused and Resilient MPACT

FY25/26 was a year of consolidation and strengthening. The trust has emerged with a more focused portfolio, lower leverage, reduced finance expenses and a stronger Singapore core. While macroeconomic uncertainties persist in China, Japan and Hong Kong, MPACT’s strategic repositioning and ongoing asset enhancement initiatives place it in a stronger position to navigate the coming years.

The outlook for the future, as indicated in the Mapletree Pan Asia Commercial Trust FY25/26 Financial Results, suggests a focused and resilient strategy to navigate uncertainties.

As an investor, the trust’s ability to maintain underlying DPU growth despite overseas headwinds is encouraging. The increasing dominance of Singapore assets, particularly VivoCity and MBC, provides a stable foundation for long‑term returns. The trust’s disciplined capital management and proactive approach to portfolio optimisation suggest that it is well‑positioned to weather market volatility while continuing to deliver sustainable distributions.

Summary of Mapletree Pan Asia Commercial Trust FY25/26 Financial Results

In summary, the Mapletree Pan Asia Commercial Trust FY25/26 Financial Results reveal a proactive approach to managing its portfolio.

The pros are:

-

- Strong Singapore portfolio delivering higher NPI and valuation uplift

- Lower finance expenses due to divestments and debt repayment

- Improved leverage, liquidity and interest coverage ratios

- VivoCity’s continued outperformance with strong rental reversions and traffic growth

- High proportion of income generated or hedged in SGD, reducing FX risk

The cons are:

-

- Overseas markets continue to face operational softness and FX headwinds

- Portfolio occupancy remains below 90%, weighed down by China and Japan

- NAV per unit declined due to FX translation losses

- Rental reversion flat as management prioritises occupancy over rent growth

- Macro uncertainties in Greater China and Japan may continue to pressure valuations