Frasers Centrepoint Trust (FCT) has released its financial results for the first half of FY2026, and the numbers reaffirm its position as one of Singapore’s most resilient and dependable retail REITs. With a portfolio anchored in suburban malls that serve essential daily needs, FCT continues to demonstrate stability and growth even in an environment marked by economic uncertainty and cautious consumer sentiment. As an investor who allocates 7.49% of my stock portfolio to FCT, I pay close attention to each set of results, and this half-year performance reinforces my conviction in the trust’s long-term prospects.

The 1HFY26 results reflect strong operational fundamentals, disciplined capital management, and meaningful progress on asset enhancement initiatives that will drive future income growth. Revenue and net property income saw double-digit increases, occupancy remained near full capacity, and rental reversions were healthy across the board. At the same time, FCT continued to refresh its tenant mix, strengthen its balance sheet, and invest in community engagement and sustainability initiatives that enhance the long-term value of its assets.

This article provides a comprehensive walkthrough of FCT’s 1HFY26 performance, the key drivers behind its results, and what investors can expect moving forward.

Strong Financial Performance Driven by Acquisitions and Organic Growth

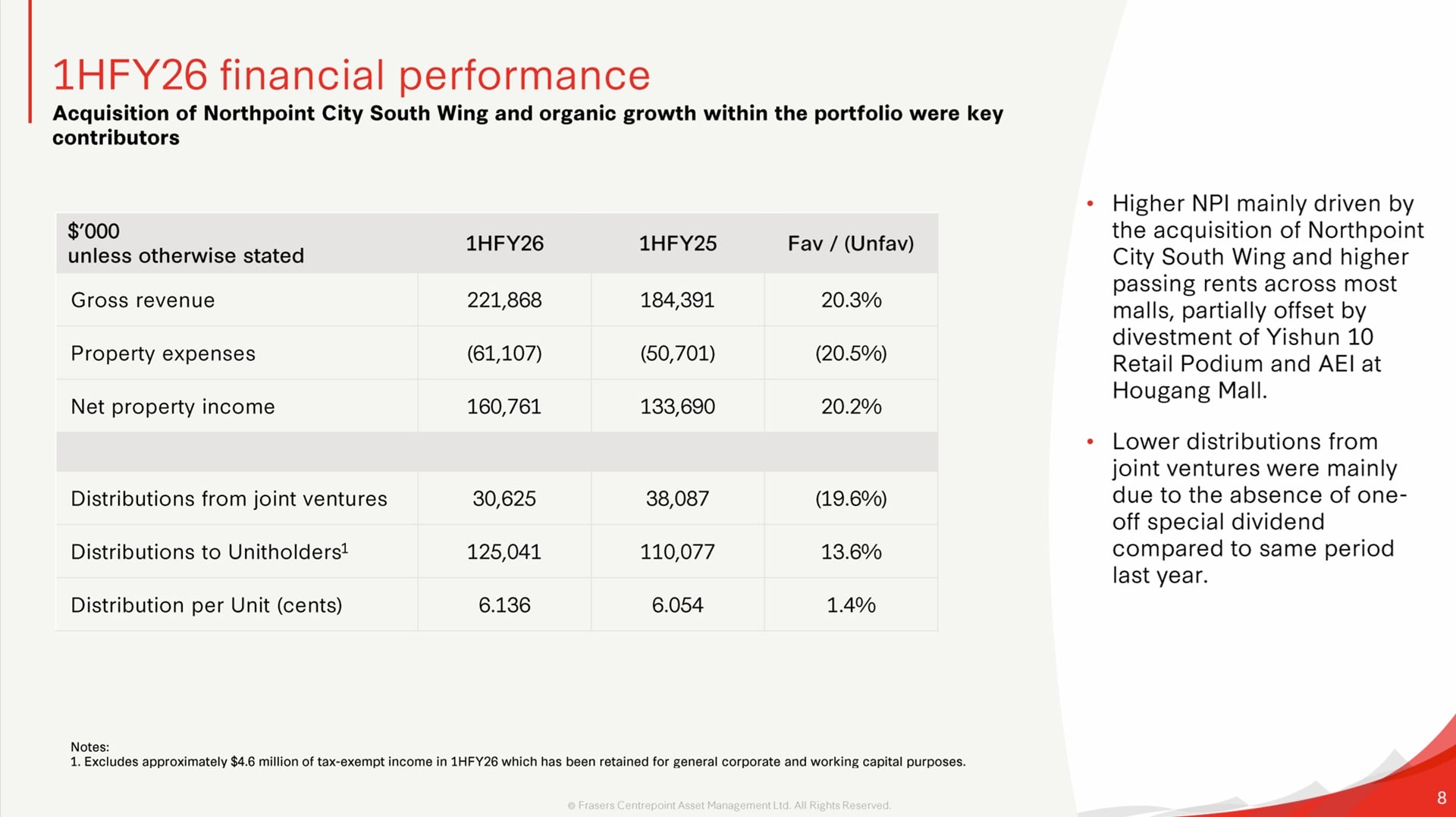

FCT delivered a robust set of financial results for the first half of FY2026. Gross revenue rose 20.3% year-on-year to S$221.9 million, while net property income increased 20.2% to S$160.8 million. These gains were primarily driven by the acquisition of Northpoint City South Wing in May 2025, which contributed significantly to both revenue and NPI. Higher passing rents across most malls also supported the uplift, although the divestment of Yishun 10 Retail Podium and ongoing AEI works at Hougang Mall partially offset the growth.

Distributions to unitholders increased 13.6% to S$125.0 million. Distribution per unit (DPU) rose 1.4% to 6.136 cents. While the DPU growth was more modest compared to the rise in NPI, this was largely due to the absence of a one-off special dividend from joint ventures that had boosted the previous year’s results. Even without such one-off contributions, FCT managed to deliver steady DPU growth, reflecting the stability of its cash flows.

The trust’s financial performance highlights the resilience of suburban retail assets, which continue to benefit from necessity-driven spending and strong catchment fundamentals. FCT’s malls are strategically located near transport nodes and residential estates, ensuring consistent footfall and tenant demand.

Operational Strength Supported by High Occupancy and Healthy Leasing Activity

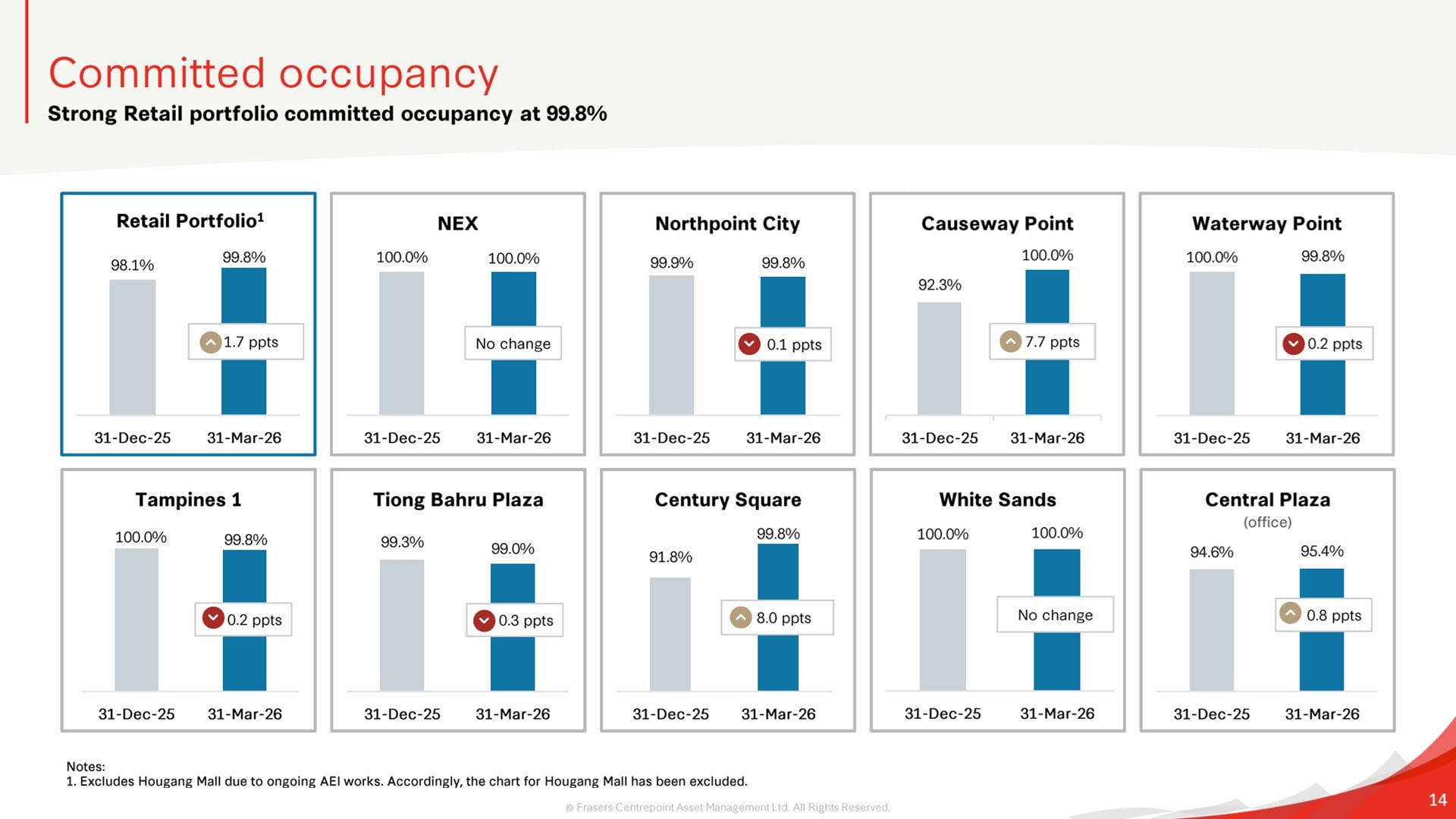

One of the standout aspects of FCT’s 1HFY26 performance is its exceptionally high committed occupancy rate of 99.8%, up from 98.1% in the previous quarter. This near-full occupancy underscores the strong demand for retail space in suburban malls, where tenants benefit from steady footfall and proximity to residential communities.

The trust signed over 289,100 square feet of new leases and renewals during the period. Rental reversion came in at a healthy 6.5% on an average-to-average basis, reflecting broad-based leasing traction across the portfolio. Food and beverage, beauty and healthcare, and fashion and accessories were among the strongest trade categories, highlighting the continued relevance of these segments in suburban retail.

Shopper traffic grew 1.8% year-on-year, while tenant sales increased 3.2%. These figures indicate that consumer activity remains resilient despite inflationary pressures and a cautious economic environment. FCT’s ongoing efforts to refresh its retail offerings also contributed to this momentum. In 1HFY26 alone, the trust introduced 48 new-to-portfolio tenants, including brands such as rumel, Mi Bibimbap, Hoe Nam Vintage, Pull-Tab Coffee, and Teva. These additions help keep the malls vibrant and aligned with evolving consumer preferences.

AEIs at Hougang Mall and NEX to Drive Future Income Growth

Asset enhancement initiatives continue to be a key pillar of FCT’s long-term growth strategy. The Hougang Mall AEI, which began in April 2025, is progressing well. Phase 1 was completed in November 2025, and Phase 2 remains on track for completion in September 2026. Over 88% of the AEI space has already been committed, and the project is expected to achieve a target return on investment of 7%. The refreshed tenant mix and upgraded spaces will enhance the mall’s competitiveness and income potential once the works are completed.

Meanwhile, NEX is preparing for a major AEI that will unlock additional retail and office space. Phase 1 of the AEI is scheduled to commence in May 2026 and complete by the end of the year. With over 40% of the space pre-committed and another 28% in advanced negotiations, the project is off to a strong start. The AEI will introduce new clusters focused on kids and education, home and living, and fashion and lifestyle. Supported by a capex of S$90 million and a target ROI of around 7%, the NEX AEI is poised to enhance the mall’s positioning as a key retail hub in the Northeast region.

These AEIs are strategically timed to capture demand from growing residential populations and evolving consumer needs. They also demonstrate FCT’s proactive approach to maintaining asset relevance and enhancing long-term income resilience.

Prudent Capital Management Strengthens Financial Stability

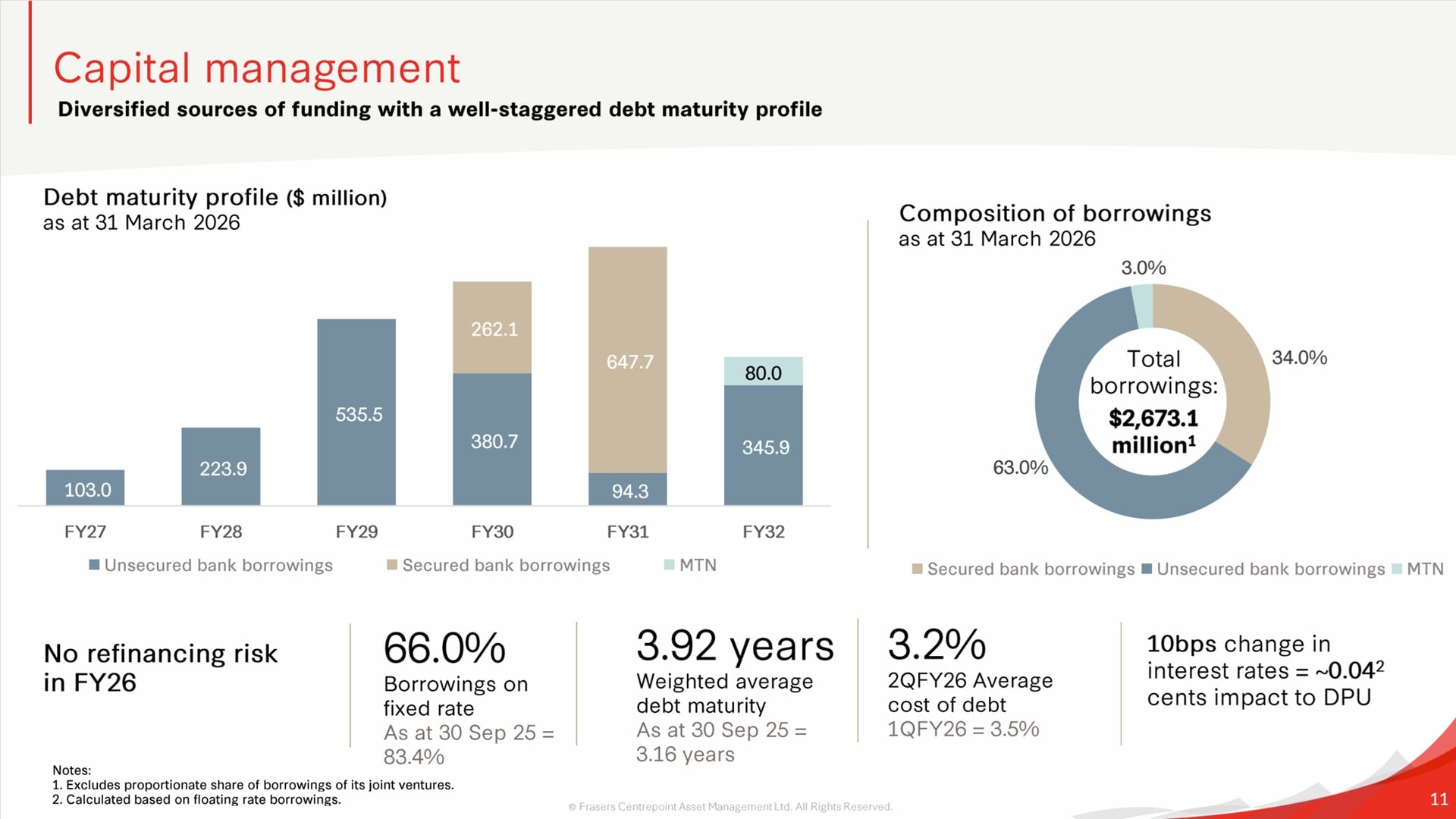

FCT continues to manage its capital structure with discipline. As of 31 March 2026, aggregate leverage stood at 40.0%, slightly lower than the 40.3% recorded at the end of December 2025. The trust refinanced all loans due in FY26, extending its weighted average debt maturity to 3.92 years. Approximately two-thirds of its borrowings are hedged to fixed interest rates, providing stability amid interest rate volatility.

The average cost of debt declined to 3.2% in 2QFY26, down from 3.5% in the previous quarter. This reduction reflects the trust’s ability to secure more favourable financing terms and optimise its debt profile. With S$873 million in undrawn facilities, FCT maintains ample liquidity to support ongoing AEIs and potential acquisitions.

The trust’s adjusted net asset value per unit rose to S$2.19, up from S$2.17 as at 30 September 2025. This increase was mainly due to changes in the fair value of derivative financial instruments.

Community Engagement and ESG Initiatives Enhance Long-Term Value

Beyond financial performance, FCT continues to invest in community engagement and sustainability initiatives. Its malls serve as vibrant social hubs, hosting events ranging from Lunar New Year celebrations to public health campaigns and senior engagement programmes. These initiatives help strengthen community ties and enhance the malls’ role as essential neighbourhood centres.

On the ESG front, FCT has fully hedged its electricity costs for FY26 and partially for FY27, reducing exposure to energy price fluctuations. All its properties are green-certified, and the trust has achieved 100% green financing across its borrowings. The adoption of smart facilities management technologies, including AI-enabled security and predictive maintenance systems, further enhances operational efficiency and cost savings.

These efforts not only support sustainability goals but also contribute to long-term asset value and tenant satisfaction.

Outlook: Resilience Amid Economic Uncertainty

While macroeconomic uncertainties persist, FCT remains confident in the resilience of Singapore’s suburban retail sector. Population growth, rising household incomes, and limited new suburban retail supply continue to support demand for well-located malls. Government initiatives such as the CDC vouchers scheme also help sustain consumer spending.

In the North region, ongoing developments are expected to create opportunities to further enhance FCT’s asset positioning. The transformation of Causeway Point into a regional retail hub, along with the AEIs at Hougang Mall and NEX, will strengthen the trust’s competitive edge.

As an investor, I view FCT as a stable, income-generating component of my portfolio. Its strong fundamentals, disciplined capital management, and proactive asset enhancement strategy provide confidence in its ability to deliver sustainable long-term returns.

Summary of Frasers Centrepoint Trust (FCT) 1HFY26 Results

Pros:

- Strong revenue and NPI growth driven by acquisitions and higher passing rents

- Near-full occupancy at 99.8% with healthy rental reversions

- AEIs at Hougang Mall and NEX poised to drive future income growth

- Prudent capital management with lower cost of debt and extended maturities

- Resilient suburban retail demand supported by essential trades and strong catchments

Cons:

- DPU growth remains modest due to absence of one-off JV distributions

- AEI downtime temporarily reduces income contribution from affected malls

- Higher leverage at 40% limits headroom for large acquisitions

- Macroeconomic uncertainties may affect consumer spending and tenant sales