CapitaLand Integrated Commercial Trust (CICT), Singapore’s largest commercial real estate investment trust, has taken a decisive step in reshaping its long‑term portfolio strategy. On 20th April 2026, the REIT announced a dual transaction that marks one of its most significant strategic pivots in recent years: the divestment of Asia Square Tower 2 for S$2.476 billion and the proposed acquisition of Paragon, a premier freehold integrated development on Orchard Road, for S$3.9 billion. Together, these moves reflect CICT’s disciplined approach to capital recycling and its ambition to strengthen its position as the leading proxy for Singapore’s commercial real estate market.

The sale of Asia Square Tower 2 and the acquisition of Paragon are deeply interconnected. By unlocking capital from a mature leasehold office asset and redeploying it into a freehold, mixed‑use trophy property in the heart of Orchard Road, CICT is positioning itself to capture structural demand trends in luxury retail, medical services, and tourism. The move also enhances the REIT’s exposure to Singapore’s most tightly held retail precinct, where supply is limited and demand remains consistently strong.

This article explores the strategic rationale behind both transactions, the financial implications for unitholders, and what this means for CICT’s future trajectory.

A Timely Exit: Divesting Asia Square Tower 2 at a Premium

Asia Square Tower 2 has been a core part of CICT’s office portfolio since 2017. Over the years, the asset delivered stable performance and reached a mature stage in its investment cycle. The property was divested for S$2.476 billion, representing a 9.9% premium over its market valuation of S$2.252 billion as at 31 December 2025. This premium underscores the asset’s attractiveness and the favourable timing of the sale.

The exit yield of 3.0% reflects the property’s leasehold nature, with 81 years remaining on its tenure. As a Grade A office building in Marina Bay, Asia Square Tower 2 has strong tenant demand, but its yield profile is lower than what CICT expects to achieve with Paragon. By monetising the asset at an optimal valuation, CICT frees up capital to reinvest into higher‑yielding opportunities.

The divestment also aligns with CICT’s strategy of recycling capital from assets that have limited upside potential. With Asia Square Tower 2 reaching a stable phase, the REIT seized the opportunity to lock in gains and redeploy funds into a property with stronger long‑term growth prospects. The sale proceeds, estimated at S$2.450 billion after transaction costs, will be channelled into the acquisition of Paragon, reducing the need for excessive debt and supporting a sustainable gearing profile.

A Landmark Acquisition: Paragon as a Freehold Orchard Road Icon

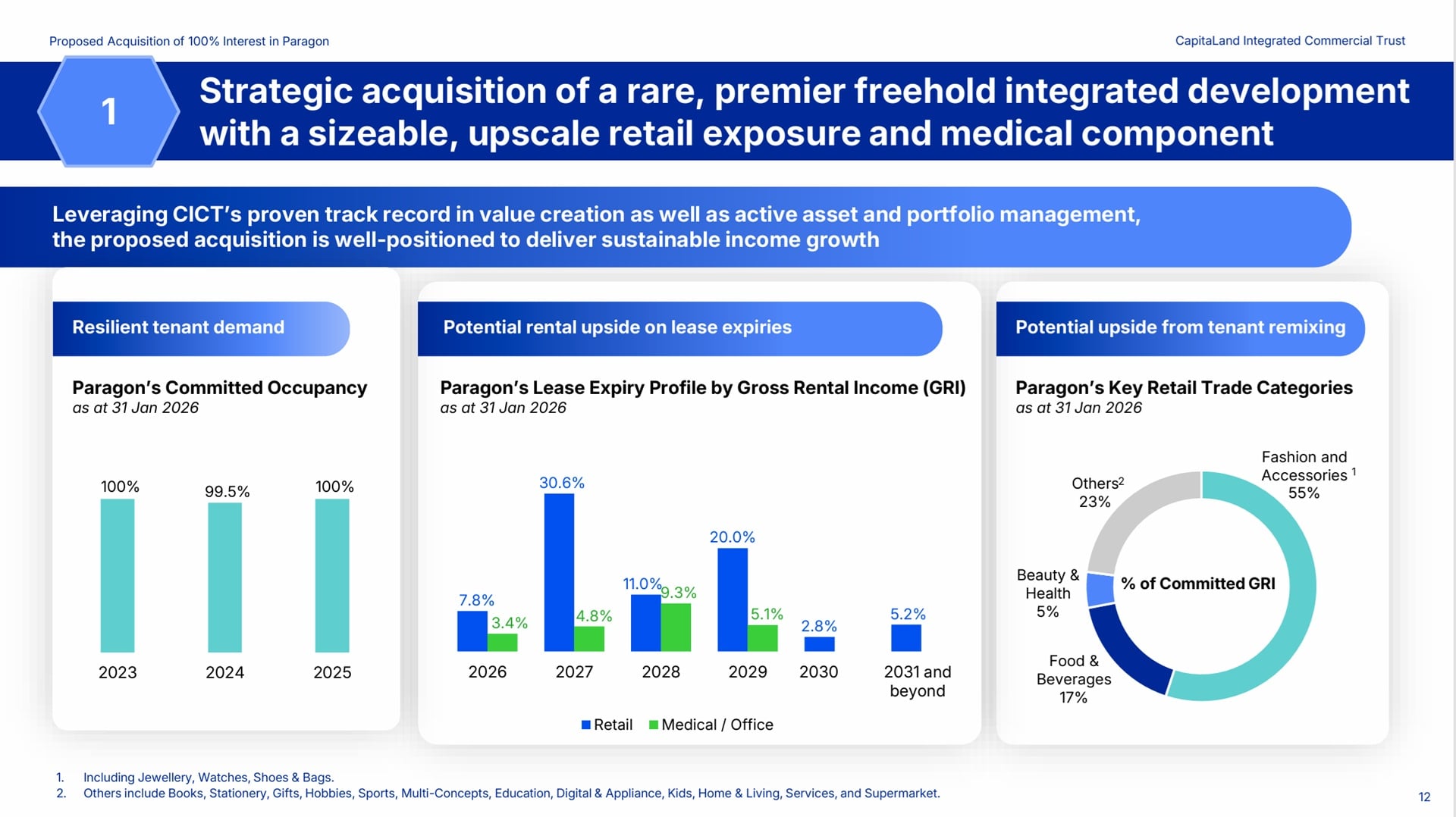

Paragon is one of Singapore’s most recognisable retail and medical destinations. Located at 290 Orchard Road, the freehold property comprises a six‑storey retail podium, two basement levels, and two towers housing medical suites and office space. As at 31 January 2026, both the retail and medical/office components were fully occupied, reflecting the asset’s enduring appeal and strong tenant demand.

The agreed property value of S$3.9 billion was derived from independent valuations by Knight Frank and Cushman & Wakefield, which placed the asset between S$3.895 billion and S$3.905 billion. The acquisition outlay, including fees and expenses, is estimated at S$3.919 billion.

What makes Paragon particularly compelling is its combination of luxury retail, medical services, and prime Orchard Road frontage. The retail podium houses over 190 brands spanning luxury, contemporary fashion, lifestyle, and dining. The medical tower is home to more than 80 multidisciplinary medical tenants, benefiting from structural tailwinds such as an ageing population and rising medical tourism. This blend of retail and medical uses creates a resilient income base that is less cyclical than pure retail assets.

The net yield of 3.9% on the agreed property value is significantly higher than the exit yield of Asia Square Tower 2, reinforcing the strategic rationale for the capital redeployment. The freehold tenure further enhances Paragon’s long‑term value, especially in a precinct where most assets are leasehold and tightly held.

Strengthening CICT’s Orchard Road Dominance

The acquisition of Paragon significantly expands CICT’s presence in Orchard Road, where it already owns ION Orchard (50% interest), Plaza Singapura, and The Atrium@Orchard. With Paragon added to the portfolio, CICT becomes the largest owner of private retail space in Singapore, commanding an estimated 10% share of the market based on net lettable area.

Orchard Road remains Singapore’s premier shopping belt, supported by strong tourism flows, high‑income local shoppers, and limited new retail supply. Between 2026 and 2028, annual gross new retail supply is forecasted at only 0.3 million square feet, with no major developments expected. This tight supply environment supports rental growth and enhances the value of existing assets.

Tourism recovery is another key driver. Singapore recorded 16.9 million tourist arrivals in 2025, and projections for 2026 range between 17 and 18 million visitors. Tourism receipts are expected to reach up to S$32.5 billion. Paragon, with its luxury retail mix and medical tourism appeal, is well positioned to capture this demand.

By consolidating its Orchard Road footprint, CICT strengthens its competitive moat and enhances its ability to shape tenant mix, drive experiential retail, and optimise asset performance across multiple properties in the precinct.

Enhancing Portfolio Quality and Diversification

Post‑acquisition, CICT’s enlarged portfolio will be valued at approximately S$28.7 billion, with 95% of its assets located in Singapore. The addition of Paragon increases the proportion of integrated developments within the portfolio, balancing retail, office, and medical exposure. This diversification reduces reliance on any single asset class and enhances income stability.

Tenant concentration risk remains low, with no single tenant contributing more than 5% of gross rental income. The lease expiry profile is also well distributed, reducing refinancing and occupancy risks. Paragon’s strong occupancy and diversified tenant base further strengthen the REIT’s resilience.

Financial Impact: DPU Accretion and Sustainable Leverage

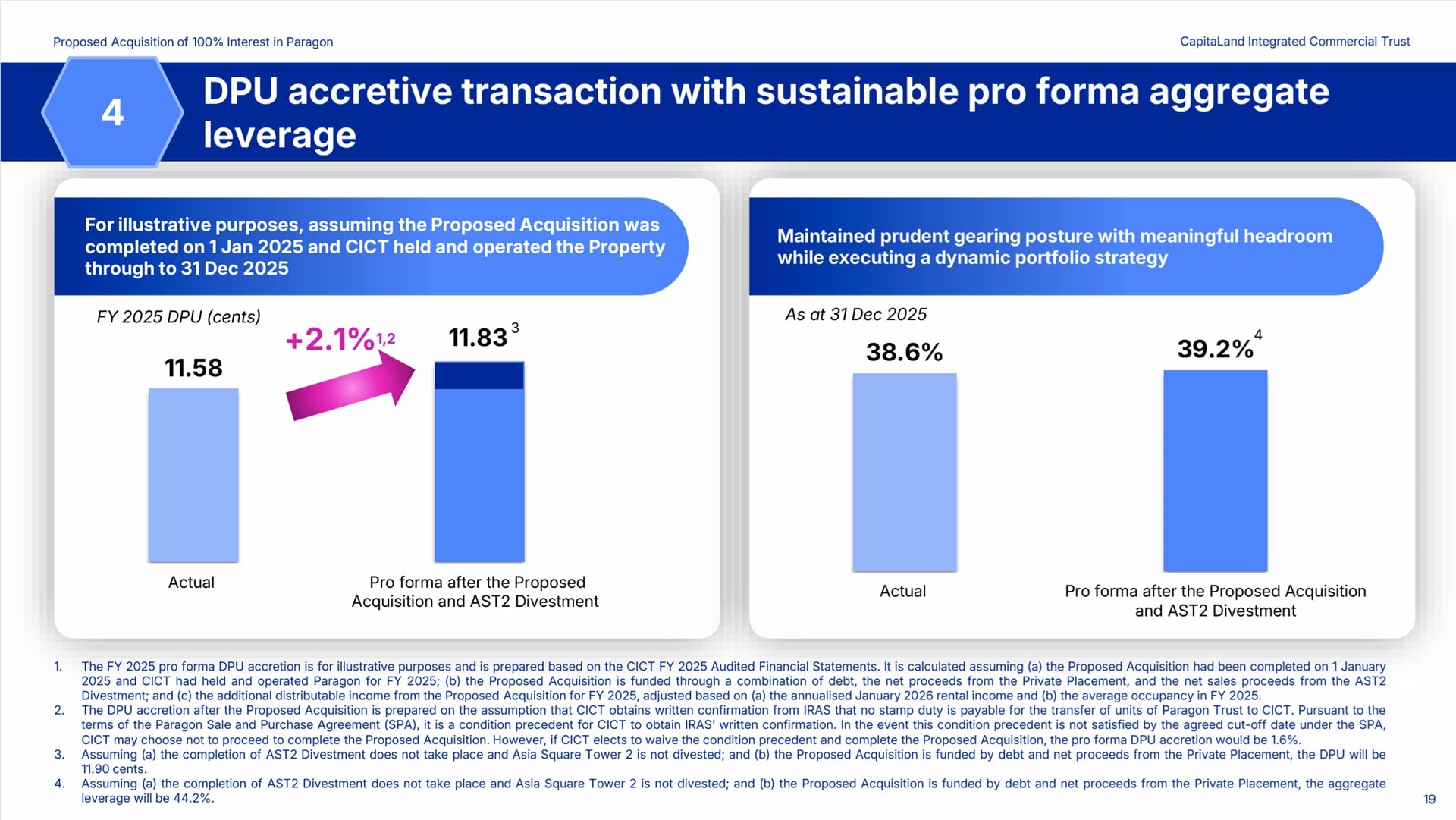

One of the most important considerations for unitholders is the financial impact of the transactions. Based on pro forma estimates, the acquisition of Paragon and the divestment of Asia Square Tower 2 are expected to deliver a 2.1% increase in distribution per unit for FY2025, assuming the acquisition had been completed at the start of the year.

This accretion is driven by Paragon’s higher net yield, full occupancy, and strong rental income. The financing structure, which includes debt, private placement proceeds, and the divestment proceeds from Asia Square Tower 2, helps maintain a prudent balance sheet. Pro forma aggregate leverage is expected to be 39.2%, comfortably below the regulatory limit of 50%.

If the acquisition is completed before the divestment of Asia Square Tower 2, CICT plans to use a bridging loan to temporarily fund the transaction. This loan will be repaid once the divestment is completed. The acquisition fee will be paid in units, aligning the manager’s interests with those of unitholders.

Long‑Term Growth Potential Through Asset Enhancement

Paragon has not undergone a major asset enhancement initiative since 2009. Preliminary analysis by the vendor suggests that a future enhancement could involve capital expenditure of S$300 million or more, depending on scope and design. CICT intends to conduct its own feasibility studies to evaluate enhancement opportunities that could elevate Paragon’s positioning and long‑term performance.

Given the competitive nature of Orchard Road and evolving consumer expectations, a well‑executed enhancement could unlock significant value. Enhancements may include reconfiguring retail layouts, upgrading medical facilities, introducing new experiential concepts, or improving connectivity and circulation. While the final scope remains subject to internal approvals, the potential upside adds another layer of growth optionality for unitholders.

A Strategic Move That Reinforces CICT’s Leadership

The divestment of Asia Square Tower 2 and the proposed acquisition of Paragon represent a bold and strategic reallocation of capital. By exiting a mature leasehold office asset and acquiring a freehold, high‑yielding integrated development in Singapore’s most coveted retail precinct, CICT is reinforcing its leadership in the commercial real estate landscape.

The transactions enhance portfolio quality, strengthen income resilience, and position the REIT to benefit from long‑term structural trends in retail, medical services, and tourism. With distribution per unit accretion, sustainable leverage, and a stronger Orchard Road presence, CICT is charting a path of disciplined growth and value creation.

As the REIT prepares for unitholder approval and eventual completion of the acquisition, the market will be watching closely. If executed as planned, this strategic pivot could become one of the defining milestones in CICT’s evolution as Singapore’s premier commercial REIT.

Summary of the Paragon Acquisition

The pros are:

- Strengthens CICT’s dominance in Orchard Road, Singapore’s most valuable retail precinct

- Enhances portfolio quality with a freehold, high‑yielding integrated development

- Provides resilient income through a mix of luxury retail and medical tenants

- Expected to be distribution per unit accretive

- Supported by strong tourism recovery and limited new retail supply

- Diversifies income streams and reduces tenant concentration risk

The cons are:

- High acquisition cost of S$3.9 billion increases financial commitments

- Potential future asset enhancement may require significant capital expenditure

- Integration risks associated with adding a major asset to the portfolio

- Short‑term gearing may rise if acquisition precedes the divestment of Asia Square Tower 2

- Exposure to Orchard Road increases concentration in a single precinct

Sources:

CICT – Announcement Presentation

3 comments from a long term investor of CICT(2015 vintage):

1) Paragon was the crown jewel of SPH Reit( privatized). In fact, the entire SPH Reit was propped up by this single mall. I know because I was also a faithful unitholder of SPH Reit. Even though there are already multiple blinking jewels in CICT’s portfolio, Paragon will not be outshined.

2) Adding Paragon to CICT’s collection is a no brainer.

3) Speaking about Jewels, there’s a jewel over in the eastern end of Singapore, which also could be acquired to adorn CICT’s crown.