Keppel DC REIT has released its 1Q 2026 operational updates, and this quarter feels different. After two years of navigating rising interest rates, tenant‑related uncertainties, and a volatile macro environment, the REIT is beginning to show the kind of momentum that long‑term investors have been waiting for. As someone who allocates 5.74% of my stock portfolio to Keppel DC REIT, I read this update with a mix of caution and optimism. The numbers are stronger, the portfolio is more resilient, and the strategic direction is clearer than it has been in a while.

The data centre sector is undergoing a structural shift, driven by the explosive growth of artificial intelligence workloads, hyperscaler expansion, and the global race to secure digital infrastructure. Keppel DC REIT sits at the intersection of these forces, and this quarter’s results show how the REIT is positioning itself to benefit from these long‑term trends while tightening its fundamentals.

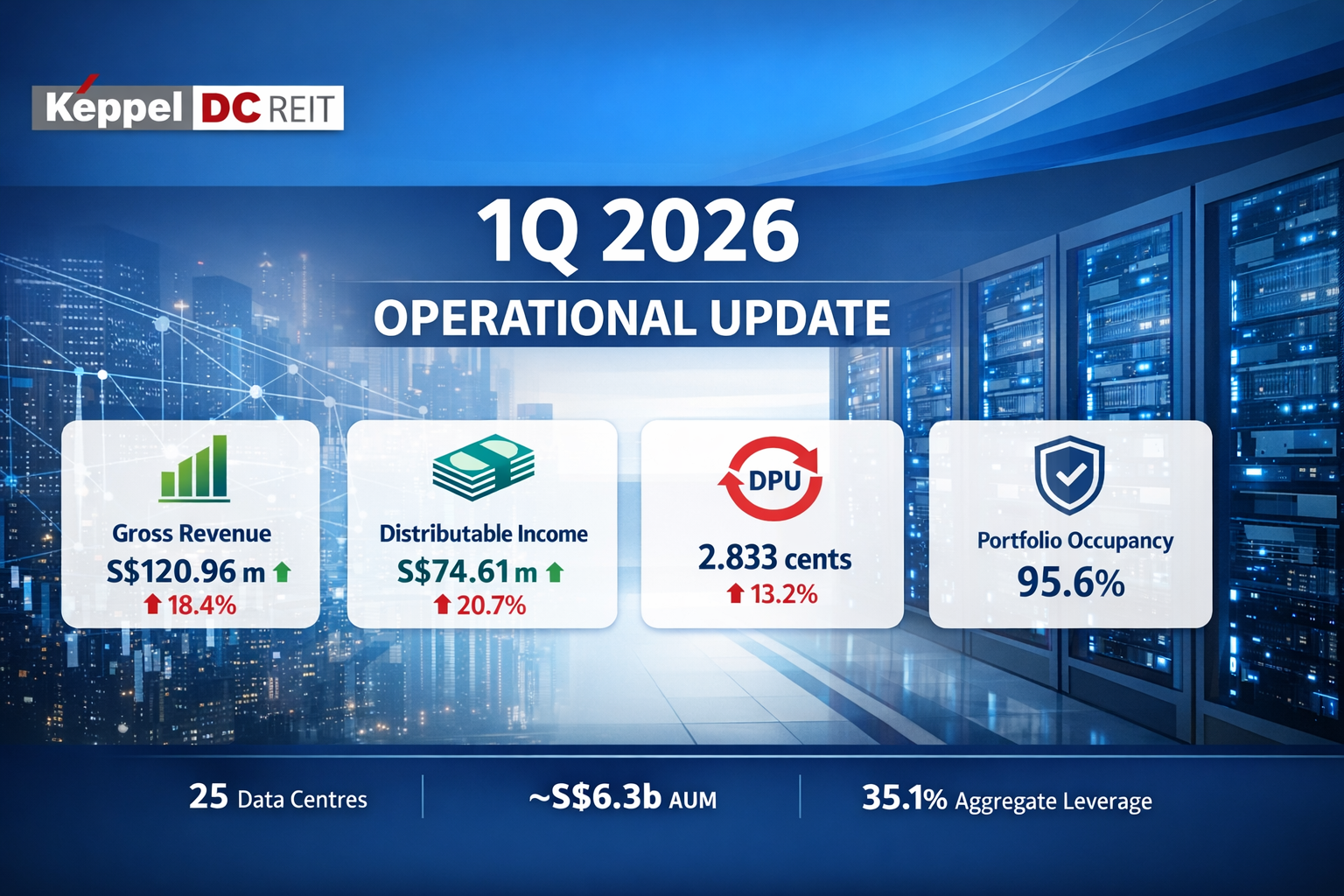

The 1Q 2026 update highlights improvements in revenue, distributable income, occupancy, and capital management. It also provides a deeper look into the REIT’s global portfolio, tenant mix, and the evolving landscape of data centre demand. What emerges is a picture of a REIT that is stabilising, strengthening, and preparing for the next phase of growth.

A Quarter of Strong Financial Recovery

The financial performance for 1Q 2026 stands out as one of the strongest in recent quarters. Gross revenue rose to S$120.96 million, an 18.4% increase from the same period last year. Net property income grew even faster, rising 19.4% to S$105.17 million. This uplift was driven by a combination of factors, including the acquisition of Tokyo Data Centre 3, higher contributions from contract renewals and rental escalations, and the consolidation of full ownership in Keppel DC Singapore 3 and 4. These strategic moves have begun to bear fruit, and the numbers reflect that.

Distributable income increased by 20.7% year‑on‑year to S$74.61 million. This is a meaningful improvement, especially considering the pressure on distributions in recent years due to higher financing costs and tenant‑related issues in China. The distribution per unit (DPU) rose to 2.833 cents, a 13.2% increase from 1Q 2025. While Keppel DC REIT pays distributions semi‑annually, this quarterly DPU figure provides a strong indication of the REIT’s improving cash‑flow profile.

The REIT did acknowledge that the divestment of Kelsterbach Data Centre in Germany partially offset the gains from acquisitions. However, the impact was relatively modest compared to the uplift from new assets and rental escalations. The overall financial picture is one of recovery and renewed strength.

Portfolio Stability Anchored by High Occupancy and Long WALE

Keppel DC REIT’s portfolio continues to demonstrate resilience, with occupancy remaining high at 95.6% as of 31 March 2026. This is only slightly lower than the 95.8% recorded in the previous quarter, and the REIT attributes the stability to its mix of contracted data centre spaces and active portfolio optimisation. The REIT’s weighted average lease expiry (WALE) stands at 6.5 years by lettable area, providing strong income visibility. By rental income, WALE is 4.6 years, reflecting the shorter contractual periods typical of colocation assets, which make up a significant portion of the portfolio.

One of the most encouraging metrics this quarter is the rental reversion of approximately 51% for contracts renewed in 1Q 2026. This suggests that demand for data centre capacity remains robust and that the REIT has pricing power in key markets. With only around 6% of rental income up for renewal each year in 2026 and 2027, the REIT is well‑positioned to maintain stable cash flows while capturing upside from market demand.

The tenant base remains diversified across 722 unique clients, with Internet Enterprise companies contributing 69.6% of rental income. Telecoms and IT services make up the next largest segments. The top 10 tenants contribute 42.8% of rental income, and while this concentration is notable, the majority of these tenants are Fortune Global 500 hyperscalers. These are sticky, long‑term clients with significant infrastructure needs, and their presence provides stability to the portfolio.

Capital Management Strengthens with Lower Leverage and Improved Debt Costs

In a high‑interest‑rate environment, capital management becomes one of the most critical aspects of REIT performance. Keppel DC REIT has made meaningful progress in this area. Aggregate leverage stands at 35.1%, down 20 basis points from the end of 2025. This reduction was driven primarily by the depreciation of the Japanese yen and euro against the Singapore dollar, which lowered the SGD value of foreign‑currency borrowings.

The REIT now has approximately S$550 million of debt headroom based on its internal threshold of 40% gearing, and around S$2 billion of headroom based on the MAS regulatory limit of 50%. This gives the REIT flexibility to pursue future acquisitions without overstretching its balance sheet.

The average cost of debt improved to 2.6%, down 20 basis points from the previous quarter. This improvement was due to the full‑quarter impact of acquisition loans drawn in 4Q 2025, particularly in Japanese yen and Singapore dollars, which carried interest rates below the REIT’s average cost of debt. The trailing 12‑month interest coverage ratio stands at 7.2 times, slightly lower due to higher finance costs but still comfortably above industry norms.

The REIT maintains a strong hedging position, with 84.8% of its debt fixed. This significantly reduces exposure to interest rate volatility. Additionally, the REIT has a natural hedge of around 71% for its overseas portfolio, mitigating currency risks. These measures collectively strengthen the REIT’s financial resilience and provide stability in an uncertain macro environment.

A Global Portfolio Positioned for AI‑Driven Growth

Keppel DC REIT now manages 25 data centres across 10 countries, with assets under management of approximately S$6.3 billion. The portfolio is heavily weighted toward Asia Pacific, which accounts for 84.7% of AUM. Singapore alone contributes 62.7%, reflecting the country’s status as a regional data centre hub.

Recent acquisitions and asset enhancements have strengthened the portfolio. Tokyo Data Centre 3, acquired in 2025, is now fully contributing to revenue and stands out as a high‑quality hyperscale asset with a long WALE of 14.5 years. Keppel DC Singapore 7 and 8 have secured 10‑year land lease extensions, enhancing long‑term asset value and stability. Meanwhile, the Guangdong Data Centres in China remain fully occupied, although rental income continues to be affected by loss allowances for uncollected rent.

The REIT’s strategy remains focused on hyperscale data centres, high‑quality colocation assets, and markets with strong digitalisation and AI‑driven demand. This aligns with global trends, as AI inference workloads are projected to become the largest driver of data centre usage by 2030. The REIT’s exposure to hyperscalers positions it well to benefit from this structural shift.

Navigating Global Uncertainty with Operational Resilience

The REIT acknowledges the broader macroeconomic uncertainties, including rising energy prices and inflation risks stemming from the Middle East conflict. Central banks such as the Federal Reserve and the European Central Bank have kept interest rates unchanged but remain prepared to tighten if inflation pressures return. Despite these challenges, the REIT expects limited first‑order impact from energy price volatility, as net electricity costs account for less than 3% of operating expenses. Power procurement contracts are also in place through the end of 2026, providing additional stability.

The capital landscape for data centres is evolving, with operators increasingly turning to asset recycling, sale‑and‑leasebacks, and platform‑level joint ventures to unlock capital for expansion. These trends underscore the growing institutionalisation of the data centre asset class and highlight the importance of flexible capital structures. Keppel DC REIT’s strong balance sheet and disciplined capital management position it well to participate in this evolving landscape.

My Perspective as an Investor

With 5.74% of my portfolio invested in Keppel DC REIT, I view this quarter’s results as a meaningful step forward. The REIT has stabilised after a challenging period and is now benefiting from structural tailwinds in the data centre sector. The improvements in revenue, distributable income, occupancy, and cost of debt are encouraging, and the REIT’s positioning in AI‑driven markets provides a compelling long‑term growth narrative.

At the same time, risks remain. Tenant concentration, exposure to China, and global macro uncertainties require ongoing monitoring. But the REIT’s strong fundamentals, disciplined capital management, and strategic portfolio positioning give me confidence in its long‑term prospects.

Pros and Cons of Investing in Keppel DC REIT (Based on 1Q 2026 Updates)

The pros are:

- Strong revenue and income growth

- Positive rental reversion of ~51%

- High occupancy and long WALE

- Improved cost of debt and strong hedging

- Significant debt headroom for acquisitions

- AI‑driven structural demand supports long‑term growth

- Diversified global portfolio

- High‑quality hyperscaler tenants

The cons are:

- Tenant concentration risk

- Exposure to China with ongoing loss allowances

- Higher finance costs from acquisition loans

- Geopolitical and macroeconomic uncertainties

- Shorter WALE for colocation assets