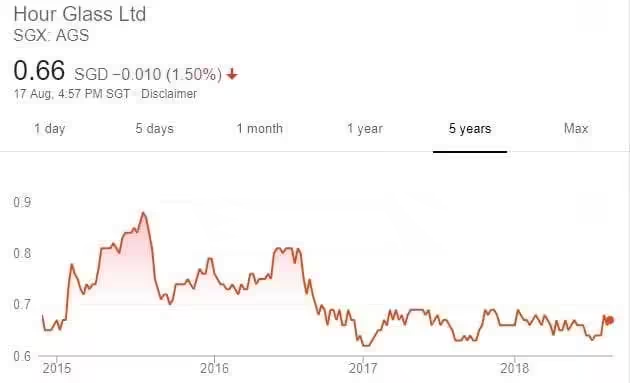

The Hour Glass has been suffering from the downtrend in the luxury goods market in both Hong Kong and China due to the clamp down of corruption from the Chinese government since 2015. This can be seen from the share price where it fell from its highest peak of S$0.88 to around S$0.71. And yes, I was vested prior to the plunge in share price.

The Hour Glass currently makes up 3% of my entire stock portfolio. Re-capping my reasons to stay invested:

- Simple luxury watch business

- Good management

- Consistent dividend

- Consistent profitability and performance (Revenue, Profits and NAV)

- Low debt servicing ratio

Luxury Consumption vs State of Economy

The Hour Glass is in the luxury watch business and luxury consumption is led by the state of the economy. Under good times, people have more spending power and thus the ability to spend on luxury goods. The Hour Glass business is thus cylindrical stock.

Finally after 3 years of waiting, the Chinese shoppers are back. In the FY2018 annual report, The Hour Glass mentioned that the luxury watch market has enjoyed a pronounced turnaround in the last 12 months which was driven by a strong global economy and revived demand from Chinese shoppers.

The Hour Glass has recently announced its 1Q2019 financial results. Revenue for the quarter increased by 10.0% to $180.7 million as compared to $164.4 million achieved in the same period last year as sentiment improved in selective markets in the region. Gross margin improved to 24.4% and resulted in higher profit after tax to $14.5 million, a 103% increase compared to $7.1 million for 1Q FY2018. As at 30 June 2018, group inventory was $277.8 million. Cash and cash equivalents stood at $188.0 million. Consolidated net assets were $523.8 million or $0.74 per share.

1QFY19 Financial Results

| 1QFY19

(S$’000) |

1QFY18

(S$’000) |

Change | |

| Revenue | 180,726 | 164,373 | 10% |

| Net Profit | 14,458 | 7,116 | 103% |

| Earnings Per Share (EPS) | 2.03 cents | 0.99 cents | 105% |

| Net asset value per ordinary share (in $) | 0.74 | 0.39 | 89.74% |

Dividends

Based on the dividend payout of 2 cents and current share price of S$0.66, this translates to a current dividend yield of 3.03%. The management has been consistent with dividend payout, however dividends have not increased over the past 3 years.

Debt to Equity Ratio

From the below table, we can see that the management has been proactively reducing its debts.

| FY2018 | FY2017 | FY2016 | FY2015 | FY2014 | |

| Debt to Equity Ratio (%) | 9.8 | 10.7 | 14.4 | 15.0 | 10.9 |

Summary

The Hour Glass is also sitting on a pile of cash and cash equivalents of S$188 million. It is unclear what they will do with the increasing stock pile of cash (E.g. increase inventories, open more stores etc).

The Hour Glass currently has an estimated intrinsic value of S$0.81. At the current price of S$0.66, this translates to roughly 23% margin of safety should you jump onto the bandwagon now. The management has proven its consistent dividend payout of at least 24% of their earnings.

I am indecisive whether to hold on to The Hour Glass while waiting for clarity. Those not vested yet can ride on uptrend due to the come back of the Chinese tourists which have a possibility of unlocking The Hour Glass’s value.

For those vested like me during its peak can only collect dividends while waiting to break even or reduce losses.