On 26th October 2023, MPACT (Mapletree Pan Asia Commercial Trust) announced its 2Q FY23/24 financial results. With the merger between Mapletree North Asia Commercial Trust and Mapletree Commercial Trust, MPACT is no longer a pure Singapore property play as it inherited the Hong Kong properties.

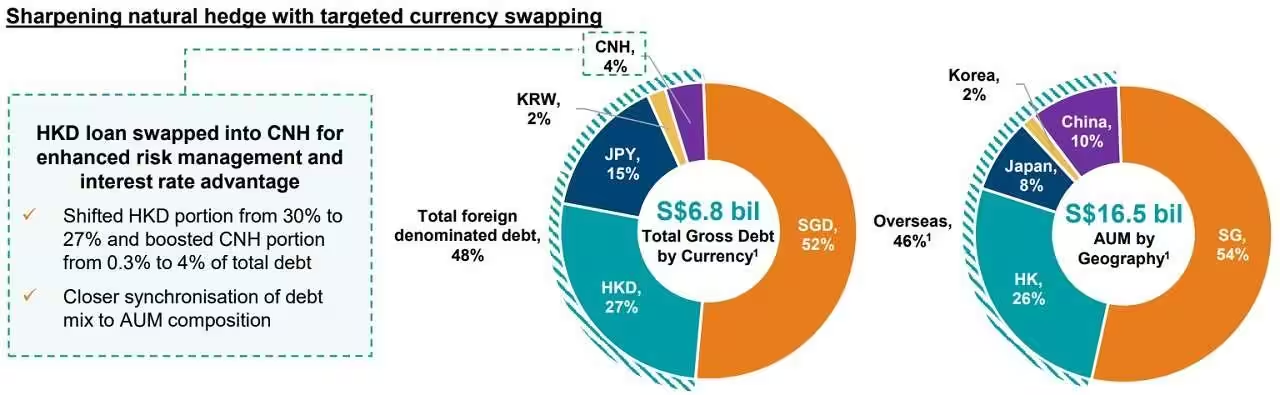

As at 30 September 2023, MPACT’s total assets under management was S$16.5 billion. The portfolio comprised 18 commercial properties across five key gateway markets of Asia – five in Singapore, one in Hong Kong, two in China, nine in Japan and one in South Korea.

With underperforming assets inherited from Mapletree North Asia Commercial Trust, let us take a detailed look how bad the financial results are.

MPACT 2Q FY23/24 Financial Results

In 2Q FY23/24, MPACT’s Gross Revenue increased by 10.1% year-on-year to S$240.2 million. The higher gross revenue was primarily due to the full quarter contribution from overseas properties acquired through the merger and stronger performance and higher contribution from the Singapore properties.

The improvement in Gross revenue was dampened by stronger SGD against all foreign currencies, increased property operating expenses and higher utility rates.

Net finance cost increased by 37.5% due to interest expenses incurred by the overseas properties and the acquisition debt. Interest rates were also elevated on existing SGD and HKD borrowings.

As a result of the increase in property cost, utility cost and net finance costs, Distribution Per Unit (DPU) fell 8.2% year-on-year to 2.24 cents.

| 2Q FY23/24 (S$’000) |

2Q FY22/23 (S$’000) |

Change | |

| Gross Revenue | 240,162 | 218,165 | 10.1% |

| Net Property Income | 183,158 | 168,511 | 8.7% |

| Property expenses |

(57,004) | (49,654) | (14.8%) |

| Net Finance Costs |

(57,553) | (41,861) | (37.5%) |

| Amount Distributable To Unitholders | 118,035 | 117,683 | 0.3% |

| Distribution Per Unit (“DPU”) (cents) | 2.24 | 2.44 | (8.2%) |

Debt

As of 30th September 2023, MPACT’s gearing stood at a high of 40.7%. Average Term to Maturity of Debt stood at 3 years.

79.9% of MPACT’s borrowings are hedged at fixed interest rate to mitigate against climbing interest rates.

MPACT was given a Baa1 (Negative) rating by Moody’s.

Debt maturity is well-distributed with FY23/24 refinancing mostly completed.

To mitigate against foreign exchange risks, MPACT is applying currency swapping as a natural hedge.

Companies that sell their products in foreign markets typically face currency risks. The risk can be hedged by incurring expenses in the same currency

Occupancy

As of 30th September 2023, MPACT’s overall portfolio occupancy stood healthy at 96.3%.

I like the way MPACT summarizes the occupancy and rental reversion of its assets. China, Japan and Hong Kong properties are having negative rental reversion.

Current Dividend Yield

Based on MPACT’s closing share price of S$1.30 and FY2022/23 full year distribution of 9.61 cents, this translate to a current dividend yield of 7.39%.

Summary of MPACT 2Q FY23/24 Financial Results

As usual, let me summarize the pros and cons.

The pros are:

- MPACT’s Gross Revenue increased by 10.1% year-on-year to S$240.2 million.

- 79.9% of MPACT’s borrowings are hedged at fixed interest rate.

- Overall portfolio occupancy stood healthy at 96.3%.

- High current dividend yield at 7.39%.

The cons are:

- Increasing property operating expenses and higher utility rates.

- Net finance cost increased by 37.5%.

- Distribution Per Unit (DPU) fell 8.2% year-on-year to 2.24 cents.

- MPACT’s gearing stood at a high of 40.7%.

- MPACT was given a Baa1 (Negative) rating by Moody’s.

- China, Japan and Hong Kong properties are having negative rental reversion.