On 25th October 2023, Frasers Centrepoint Trust announced their 2H2023 Financial Results. According to the press release, Frasers Centrepoint Trust had achieved a set of strong FY23 results based on robust operating performance and strategic portfolio re-constitution.

Currently, Frasers Centrepoint Trust makes up 5.25% of my stock portfolio. This means I have a major stake on this sub-urban retail REIT.

Frasers Centrepoint Trust 2H2023 Financial Results

In 2H2023, Frasers Centrepoint Trust’s Gross revenue grew 1.8% year-on-year to S$184.1 million. The growth was driven by higher gross rent, atrium and car park income, partially offset by lower contribution from Tampines 1 due to ongoing AEI.

Property expenses in 2H2023 rose S$1.9 million or 3.6% year-on-year due to higher utilities expenses, higher repair and maintenance costs, higher staff costs and lower write-back of doubtful receivables.

Because of higher interest expense, Frasers Centrepoint Trust’s Distribution Per Unit (DPU) in 2H2023 was 1.2% lower year-on-year at 6.020 cents.

| 2H2023 (S$’000) |

2H2022 (S$’000) |

Change | |

| Gross Revenue | 184,063 | 180,744 | 1.8% |

| Net Property Income | 129,555 | 128,118 | 1.1% |

| Property expenses |

(54,508) | (52,626) | (3.6%) |

| Amount Distributable To Unitholders | 103,065 | 103,776 | (0.7%) |

| Distribution Per Unit (“DPU”) (cents) | 6.020 | 6.091 | (1.2%) |

Frasers Centrepoint Trust FY2023 Financial Results

Frasers Centrepoint Trust’s Gross revenue for FY23 was up 3.6% to S$369.7 million. Net Property Income (NPI) was up 2.7% at S$265.6 million due to the stronger gross revenue.

For FY23, property expenses rose 5.9% year-on-year to S$104.1 million.

This brings the total Distribution Per Unit (DPU) in FY23 to 12.150 cents which was slightly 0.2% lower as compared to FY22.

| FY2023 (S$’000) |

FY2022 (S$’000) |

Change | |

| Gross Revenue | 369,723 | 356,931 | 3.6% |

| Net Property Income | 265,586 | 258,597 | 2.7% |

| Property expenses |

(104,137) | (98,334) | (5.9%) |

| Amount Distributable To Unitholders | 207,745 | 208,190 | (0.2%) |

| Distribution Per Unit (“DPU”) (cents) | 12.150 | 12.227 | (0.6%) |

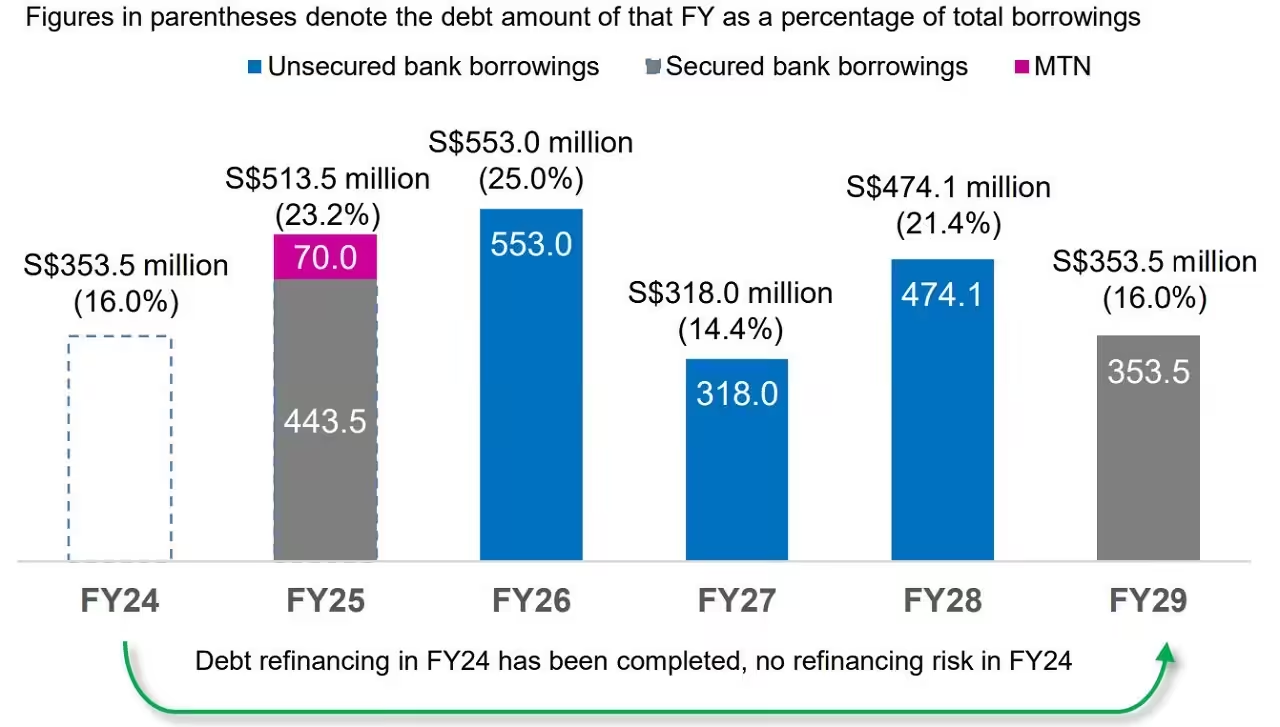

Debt

As of 30th September 2023, Frasers Centrepoint Trust’s gearing ratio stood at 39.3%. 63% of its debt are hedged to fixed interest rate. Average debt to maturity stood at 2.33 years.

The pro forma aggregate leverage is estimated to be around 36.1% after the divestment of Changi City Point and divestment of interest in Hektar REIT whereby the funds will be used to par down its debt.

As you can see from the above chart, refinancing has been completed and there is no refinancing risks for FY24.

Occupancy

The retail portfolio committed occupancy stood at a high of 99.7%. Tampines One has been excluded because of ongoing AEI works.

Frasers Centrepoint Trust’s retail rental reversion in FY23 was stronger at +4.7% as compared to +4.2% in FY22.

Current Dividend Yield

Based on Frasers Centrepoint Trust’s share price of S$2.04 and FY23 full year distribution of 12.150 cents, this works out to be a current dividend yield of 5.96%.

Summary of Frasers Centrepoint Trust 2H2023 Financial Results

We came to the last section where I will summarize the pros and cons based on Frasers Centrepoint Trust’s 2H2023 financial results.

The pros are:

- Frasers Centrepoint Trust’s Gross revenue grew 1.8% year-on-year to S$184.1 million. Similarly, full year FY23 gross revenue grew 3.6% to S$369.7 million.

- Pro forma aggregate leverage is estimated to be around 36.1% which is at acceptable ratio.

- FY24 refinancing has been completed.

- Retail portfolio committed occupancy stood at a high of 99.7%.

- Current dividend yield of 5.96%.

The cons are:

- Property expenses in 2H2023 rose S$1.9 million or 3.6% year-on-year.

- Frasers Centrepoint Trust’s Distribution Per Unit (DPU) in 2H2023 was 1.2% lower year-on-year at 6.020 cents. Similarly, full year FY23 distribution fell 0.6%.

I am personally disappointed Frasers Centrepoint Trust was not able to continue growing its DPU year-on-year. But under the increasing interest rate environment, it can be tough for most REITs.