On 24th October 2023, Mapletree Logistics Trust released their 2QFY23/24 Financial Results. Currently, Mapletree Logistics Trust makes up 3.60% of my stock portfolio. I have been wanting to increase my stake in Mapletree Logistics Trust but hesitated because of weakening economy in the logistics space.

How is Mapletree Logistics Trust performing under the rising geopolitical uncertainty and tight financial conditions?

Let us take a look in details below.

Mapletree Logistics Trust 2QFY23/24 Financial Results

Gross revenue rose 1.5% y-o-y to S$186.7 million. The increase was attributed to higher contribution from existing properties (Singapore, Hong Kong SAR) and contribution from acquisitions. The revenue gain was partly offset by lower contribution from China, loss of revenue from divested properties and properties under redevelopment and depreciation of CNY, JPY, HKD, AUD against SGD.

As you can see from the table below, property expenses increased mainly due to enlarged portfolio and increase in property tax.

Borrowing costs also increased due to incremental borrowings to fund FY23/24 acquisitions and higher average interest rates on existing debts.

Despite the negative factors, Distribution Per Unit (DPU) increased by 0.9% to 2.268 cents. The is also partly because the impact of currency volatility at the distribution level is partially mitigated through hedging.

| 2QFY23/24 (S$’000) |

2QFY22/23 (S$’000) |

Change | |

| Gross Revenue | 186,694 | 183,868 | 1.5% |

| Property Expenses |

(24,710) | (23,862) | 3.6% |

| Net Property Income | 161,984 | 160,006 | 1.2% |

| Borrowing Costs | (36,822) | (33,426) | 10.2% |

| Amount Distributable | 118,629 | 113,385 | 4.6% |

| Distribution Per Unit (“DPU”) (cents) | 2.268 | 2.248 | 0.9% |

Debt

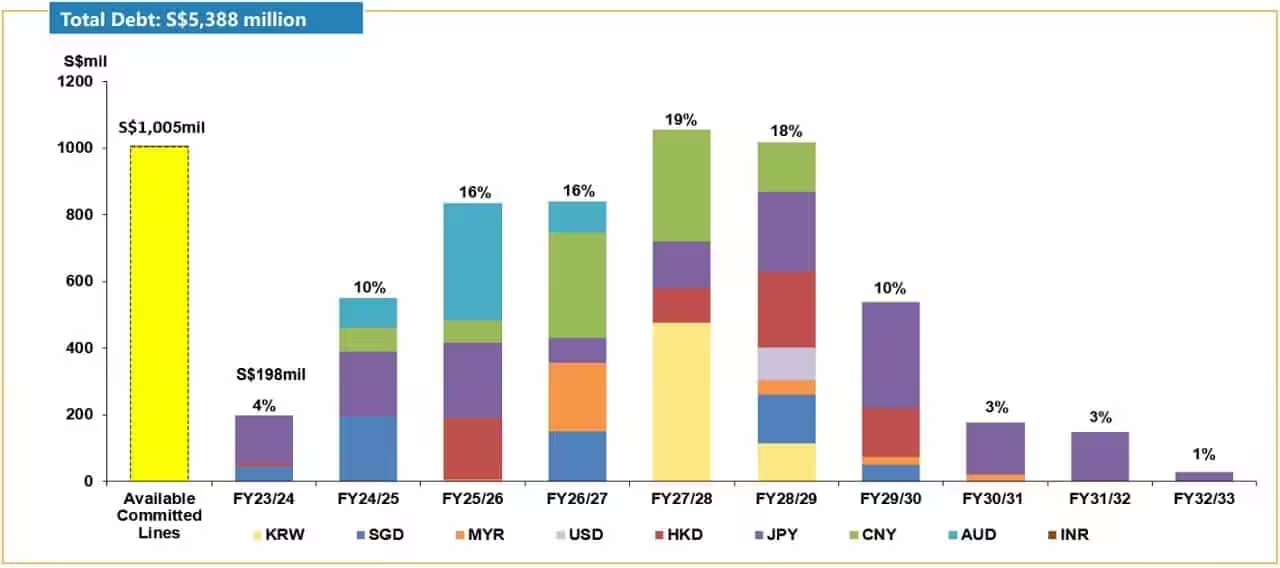

As of 30th September 2023, gearing stood at 38.9%. Mapletree Logistics Trust has a well-staggered debt maturity profile with an average debt duration of 3.8 years.

Mapletree Logistics Trust also have sufficient available committed credit facilities of S$1,005 million to refinance S$198 million (or 4% of total debt) debt due in FY23/24.

83% of total debt is hedged or drawn in fixed rates. Every potential 25 bps increase in base rates may result in estimated S$0.6m decrease in distributable income or -0.01 cents in DPU per quarter.

Occupancy

As of 30th September 2023, overall portfolio occupancy stood at 96.9%.

The decline in Japan occupancy rate due to vacancy in Kuwana Centre which is expected to backfill by 3Q FY23/24.

Mapletree Logistics Trust achieved a portfolio rental reversion of +0.2%. This reflects positive rental reversions across its markets ranging from 3.2% in Malaysia to 16.5% in Hong Kong SAR, except for China which registered negative rental reversion of -8.6% due to weakness in Tier 2 cities.

Lease expiry profile is well-staggered with weighted average lease expiry (by NLA) at 3.0 years.

Current Dividend Yield

Based on Mapletree Logistics Trust’s current share price of S$1.47 and FY22/23 full year distribution of 9.011 cents, this translate to a current dividend yield of 6.13%.

To mitigate against Forex risk, about 80% of amount distributable in the next 12 months is hedged into / derived in SGD. This provides some form of stability in terms of DPU.

Summary of Mapletree Logistics Trust 2QFY23/24 Financial Results

Let me summarize the pro and cons based on Mapletree Logistics Trust’s 2QFY23/24 financial results.

Pros

- Gross revenue rose 1.5% y-o-y to S$186.7 million.

- Distribution Per Unit (DPU) increased by 0.9% to 2.268 cents.

- Gearing stood at 38.9%, below my benchmark of 40%.

- Sufficient available committed credit facilities of S$1,005 million to refinance S$198 million debt due in FY23/24.

- 83% of total debt is hedged or drawn in fixed rates.

- Overall portfolio occupancy stood at 96.9%.

- Lease expiry profile is well-staggered.

- Positive portfolio rental reversion of +0.2%.

- High current dividend yield of 6.13%.

- Forex stability in DPU as 80% of amount distributable in the next 12 months is hedged into / derived in SGD.

Cons

- Property and borrowing expenses increased.

- Higher average interest rates on existing debts.

- China which registered negative rental reversion of -8.6%.