On 31st December 2021, Mapletree Commercial Trust (MCT) announced their proposed merger with Mapletree North Asia Commercial Trust (MNACT). The merged entity will be named Mapletree Pan Asia Commercial Trust (MPACT).

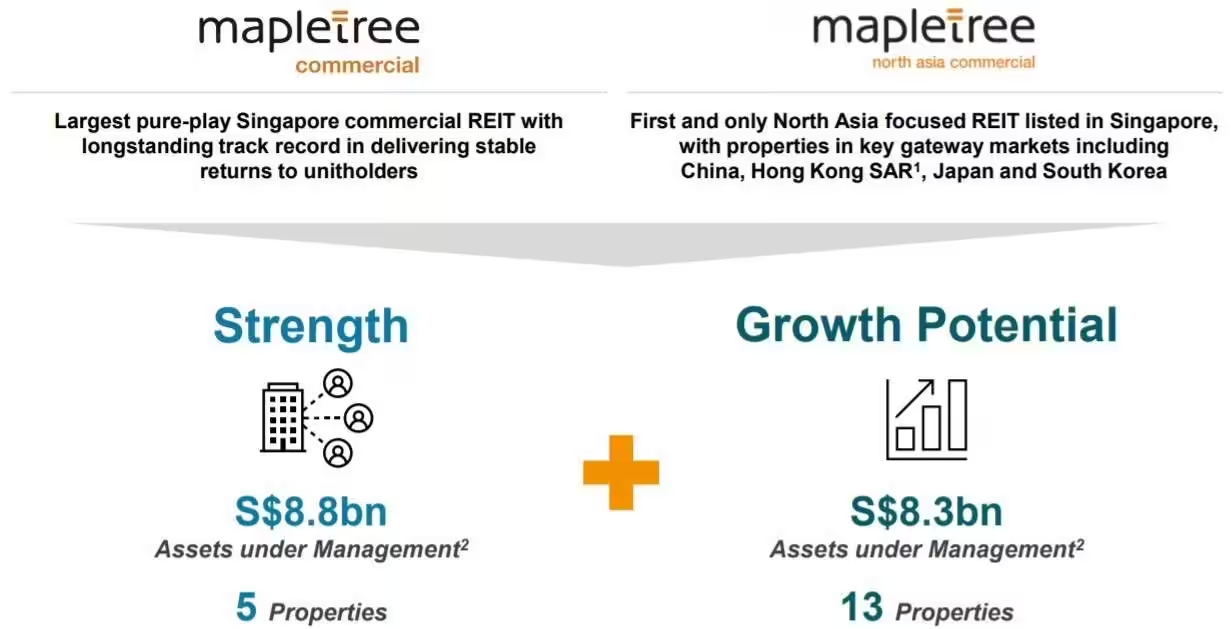

Mapletree Commercial Trust has 5 properties in its portfolio while Mapletree North Asia Commercial Trust has 13 properties. The merged entity Mapletree Pan Asia Commercial Trust (MPACT) will have 18 properties across 5 markets (Singapore, Hong Kong SAR, China, Japan and South Korea).

There will be two scheme consideration options for Mapletree North Asia Commercial Trust Unitholders with the consideration of S$1.1949 per MNACT Unit.

Cash-and-Scrip Consideration

This means you receive 84% in units of MCT and 16% in cash.

- 84% Consideration Units (0.5009 new MCT Units per MNACT Unit)

- 16% Cash Consideration (S$0.1912 in Cash per MNACT Unit)

Scrip-Only Consideration

This means you receive 100% in units of MCT.

- 100% Consideration Units (0.5963 new MCT Units per MNACT Unit)

Rationale and Key Benefits of the Merger

With every merger, the presentation slides will try to list down their rationale and key benefits.

- Proxy to Key Gateway Markets of Asia

- Enhanced Diversification Anchored by High Quality Portfolio

- Leapfrogs to Top 10 Largest REIT in Asia

- Enlarged Platform Better Positioned to Unlock Upside Potential

- DPU and NAV Accretive to MCT Unitholders

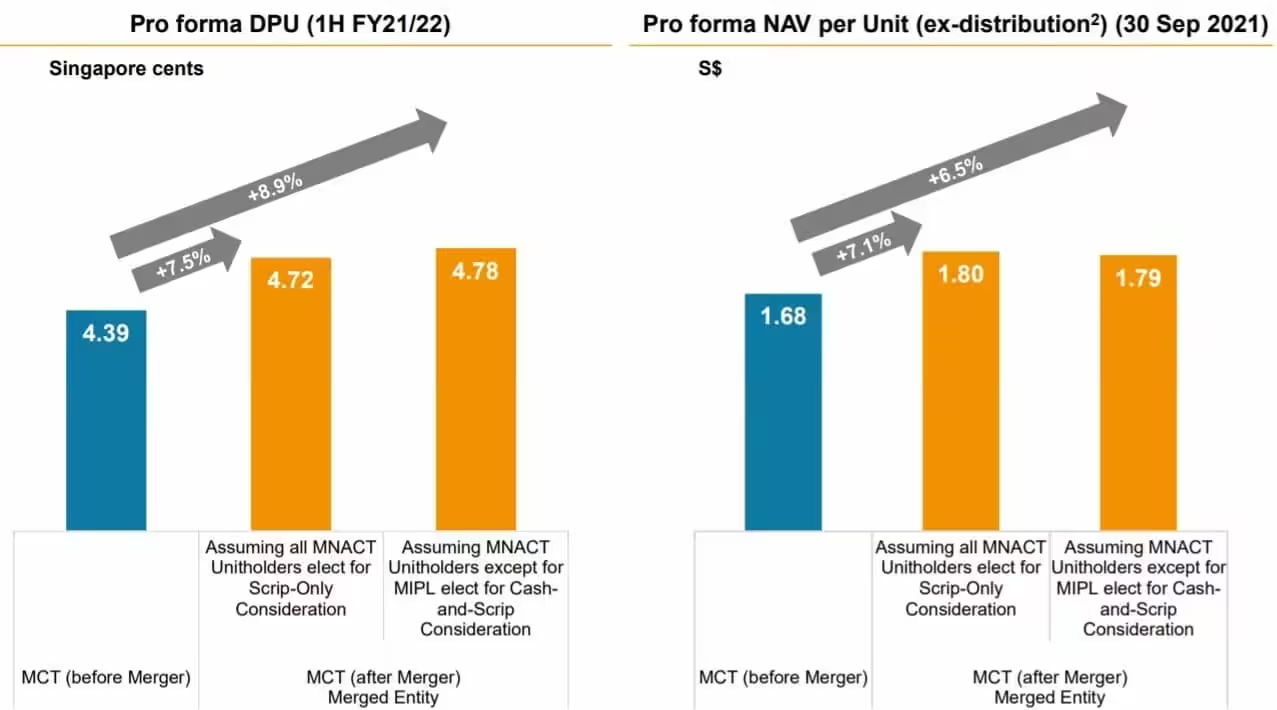

Pro forma DPU

I am ignoring the other mentioned key benefits mentioned in the presentation slides. As a dividend investor, I am more keen on the Pro forma Distribution Per Unit (DPU).

According to the presentation slides, DPU is expect to increase 7.5% or 8.9% depending on the scheme option that is chosen.

Net Asset Value (NAV) is also expected to increase 7.1% or 6.5%.

With every announcement of merger, the share price reflects whether the investors are supportive of the merger. The share price of Mapletree Commercial Trust has declined over the past few days.

On the other hand, the share price of Mapletree North Asia Commercial Trust has increased.

MCT and MNACT Merger Summary

The merger will position Mapletree Pan Asia Commercial Trust (MPACT) as the 7th largest REIT in Asia and most probably accelerate growth prospects.

However, as a Mapletree Commercial Trust shareholder, I am not supportive of the merger for the following reasons:

- The merger exposes Mapletree Commercial Trust to riskier markets such as China and Hong Kong.

- Gearing ratio for Mapletree Commercial Trust is 33.7%. With the merger, the gearing ratio of the merged entity is 39.2%.

Nevertheless, I guess there isn’t much I can do but wait for further announcements because the merger is most like to pass through.