This month, I am going to perform my Personal Analysis of Mapletree North Asia Commercial Trust.

Mapletree North Asia Commercial Trust (“MNACT”) was listed on the Singapore Stock Exchange (SGX) on 7th March 2013. It is the first real estate investment trust (“REIT”) that offers investors the opportunity to invest in high quality commercial properties situated in prime locations in China and Hong Kong SAR. The flagship properties are Festive Walk in Hong Kong and Gateway Plaza in Beijing.

In the past few years, Mapletree North Asia Commercial Trust expanded its portfolio to include properties in Japan and South Korea.

Mapletree North Asia Commercial Trust Portfolio

Mapletree North Asia Commercial Trust portfolio comprises of commercial properties situated in prime locations in Hong Kong SAR, China, Japan and South Korea.

China

Mapletree North Asia Commercial Trust has two properties in China, namely Gateway Plaza and Sandhill Plaza.

Gateway Plaza is one of the largest and most sought-after Grade-A office building. Gateway Plaza comprises of two 25-storey towers connected by a three-storey podium area, as well as three underground floors.

Sandhill Plaza was acquired in June 2015. The Plaza is a premium quality business park development in the mature area of Zhangjiang Hi-tech Park, part of Shanghai’s Free Trade Zone.

Hong Kong

Festive walk is one of the top ten largest mall in Hong Kong. It comprises of a seven-storey territorial shopping mall, a four-storey office component on top of the mall, as well as three floors of underground car parks.

Japan

- ABAS Shin-Yokohama Building

- Fujitsu Makuhari Building

- Hewlett-Packard Japan Headquarters

- Higashi-nihonbashi 1-chome Building

- IXINAL Monzen-nakacho Building

- mBAY POINT Makuhari

- Omori Prime Building

- SII Makuhari Building

- TS Ikebukuro Building

South Korea

In October 2020, the Manager completed its acquisition of The Pinnacle Gangnam in Seoul. This was co-investment with the Sponsor, the total acquisition cost of the property was S$276.4 million (based on MNACT’s effective interest of 50.0%).

The Pinnacle Gangnam is located at 119, Nonhyeon-dong, Gangnam-gu, Seoul. It is a

20-storey freehold office building with six underground floors and 181 parking lots.

The office building has direct access to an underground subway station (Gangnam-gu Office station) and is within 10 minutes by car from Gangnam’s high-end retail district (Cheongdam)

and from COEX Convention & Exhibition Center.

Financial Summary

FY20/21 Financial Results

The Distributable Income in FY20/21 was lower than FY19/20 because there were top-ups to the distributable income in FY19/20 to mitigate the decline in DPU and to enable a certain level of distributable income to the Unitholders (until such time the loss of revenue was recovered through the insurance claims).

During FY19/20, there were no rentals collected during the period when Festival Walk mall was temporarily closed from 13 November 2019 to 15 January 2020 and its office tower from 13 to 25 November 2019 (“Festival Walk Temporary Closure”).

The decline in DPU was partially offset by the full-year contributions from MBP and Omori acquired on 28 February 2020, and The Pinnacle Gangnam (“TPG”) acquired on 30 October 2020.

| FY20/21 (S$’000) |

FY19/20 (S$’000) |

Change | |

| Gross Revenue | 391,415 | 354,478 | 10.4% |

| Net Property Income | 292,040 | 277,487 | 5.2% |

| Distributable Income | 210,150 | 227,928 | (7.8)% |

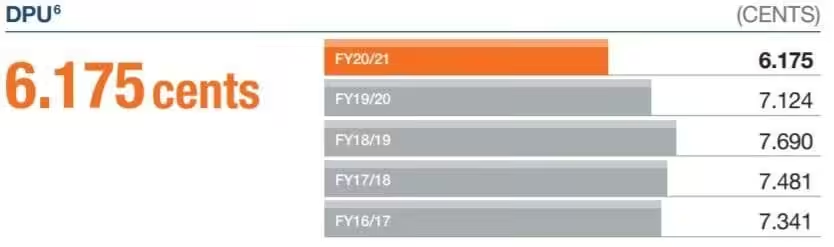

| Distribution Per Unit (“DPU”) (cents) | 6.175 | 7.124 | (13.3)% |

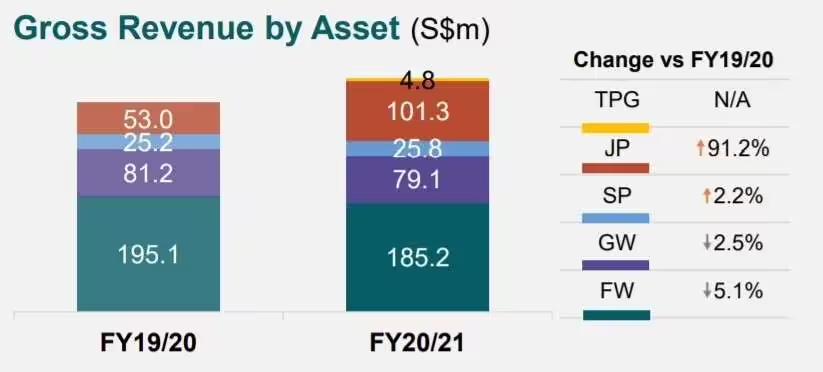

In FY20/21, Festive Walk and its Japan properties make up the bulk of the contribution of Gross Revenue by S$185.2m and S$101.3m respectively.

Occupancy Rates

As of 31st March 2021, overall portfolio occupancy stood healthy at 97.0%.

Overall Weighted Average Lease Expiry (“WALE”) stood at 2.3 years.

As you can see above, 14.6% of the leases at Festive Walk are expiring in FY21/22. With the current COVID-19 pandemic conditions and possible riot conditions in Hong Kong, it is unknown whether MNACT will have issues renewing the leases. Investors should continue to monitor the lease renewal.

The lease expiries for the assets in China, Japan and Korea remains low.

Distribution History

Distribution per unit (“DPU”) in FY20/21 was 13.3% lower than that in FY19/20.

This was due to top-ups to the distributable income (“Festival Walk Top-ups”) in FY19/20 to enable a certain level of distributable income and DPU to mitigate the loss of rental during the Festival Walk Temporary Closure.

Debt

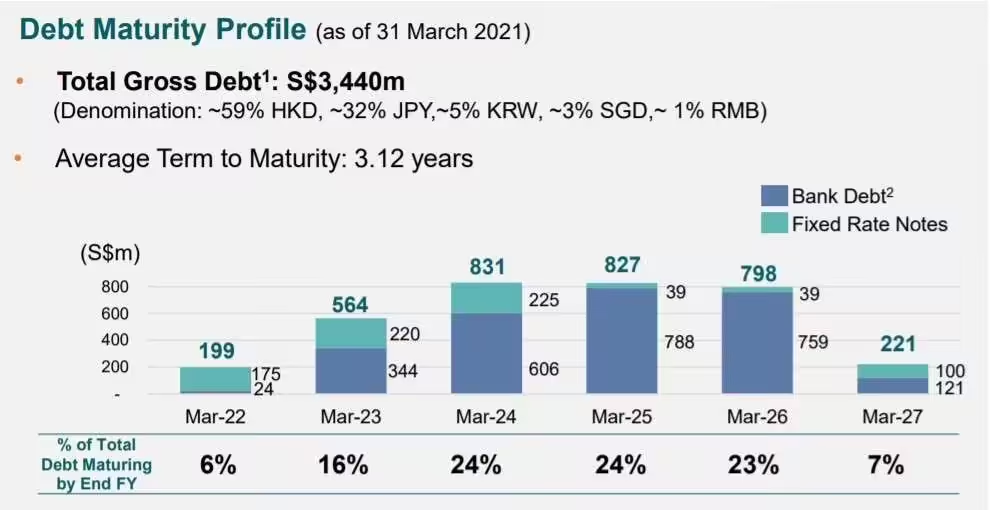

As of 31st March 2021, gearing ratio stood at 41.5%. This was an increase of 2.2% as compared to 39.3% in 31st March 2020.

The Debt Average Term to Maturity stood at 3.12 years. From what I can see, there is no worrying debt in the short term since 6% of total debt are maturing only in March 2022.

Management

Ms. Cindy Chow Pei Pei is both an Executive Director and the Chief Executive Officer of the Manager.

She has more than 23 years of investment experience in the region, including China, Hong Kong SAR, India, Japan, Singapore, Thailand and Vietnam. Prior to joining the Manager, Ms. Chow was Chief Executive Officer, India with the Sponsor, where she was instrumental in establishing the Sponsor’s investments in India.

A quick check on MNACT’s latest news shows that she has participated in the Distribution Reinvestment Plan. This means she held more shares in MNACT. This is a positive sign which shows the CEO’s confidence in MNACT.

Current Valuation

Based on the current share price of S$1.03 and FY20/21 DPU of 6.175 cents, this translate to a current dividend yield of 6.00%.

Summary of My Analysis of Mapletree North Asia Commercial Trust

From what I can see, the manager of Mapletree North Asia Commercial Trust is still working on its strategy of diversifying its assets into multiple countries. The Hong Kong riots has taught the manager the importance of diversification when its flagship mall Festive Walk was damage during the riots and had to close for damage repairs.

In summary

- Festive Walk remains the top revenue contributor of 47% with Japan properties contributing 26%. A good sign that MNACT continues to diversify its asset.

- Gearing ratio is high at 41.5%, however, there is no worry debt maturity in the short term.

- 14.6% of the leases at Festive Walk are expiring in FY21/22. With the current COVID-19 pandemic conditions and possible riot conditions in Hong Kong, it is unknown whether MNACT will have issues renewing the leases. Investors should continue to monitor the lease renewal.

- CEO opted for Distribution Reinvestment Plan which shows her confidence in MNACT.

- Decent current dividend yield of 6.00%. The dividend yield can trend higher if Hong Kong situation related to COVID-19 and riot improves. However, I foresee the DPU to remain depressed in the short term.

I will invest into MNACT if it is a long term play. In the short term, I will give MNACT a miss given the low vaccination rates in Hong Kong. I have not heard any more riot situations in Hong Kong but it may be due to the COVID-19 situation and rioters are staying indoors.

I hope you enjoy my Personal Analysis of Mapletree North Asia Commercial Trust!