On 16th October 2023, CICT (CapitaLand Integrated Commercial Trust) announced their 3Q2023 business updates. Since this is only a business update, there is no details on its financial performance.

In 3Q2023, CICT’s Gross Revenue increased 4.6% year-on-year to $391.3 million. Net Property Income (NPI) increased 0.6% to S$275.0 million. The increase in gross rental income was offset by a rise in operating expenses largely due to higher actual occupancy and shopper traffic.

As reflected in the chart below, we can see that its retail assets, office assets and integrated development all performed better year-on-year as compared to 2022.

Debt

As of 30th September 2023, CICT’s aggregate leverage stood at a high of 40.8%. It is fortunate to CICT that the Fed has decided not to increase interest rates for now, otherwise the aggregate leverage is expected to trend higher.

78% of CICT’s borrowings are hedged at fixed interest rates.

CICT has a long debt average term to maturity of 4.1 years. If you look at the debt maturity profile below, there is nothing of immediate concern but perhaps CICT should explore refinancing their future debt early like Frasers Centrepoint Trust or consider reducing its aggregate leverage.

Occupancy

As you can see, committed occupancy increase across its portfolio. As of 30th September 2023, overall portfolio occupancy stood at 97.3%.

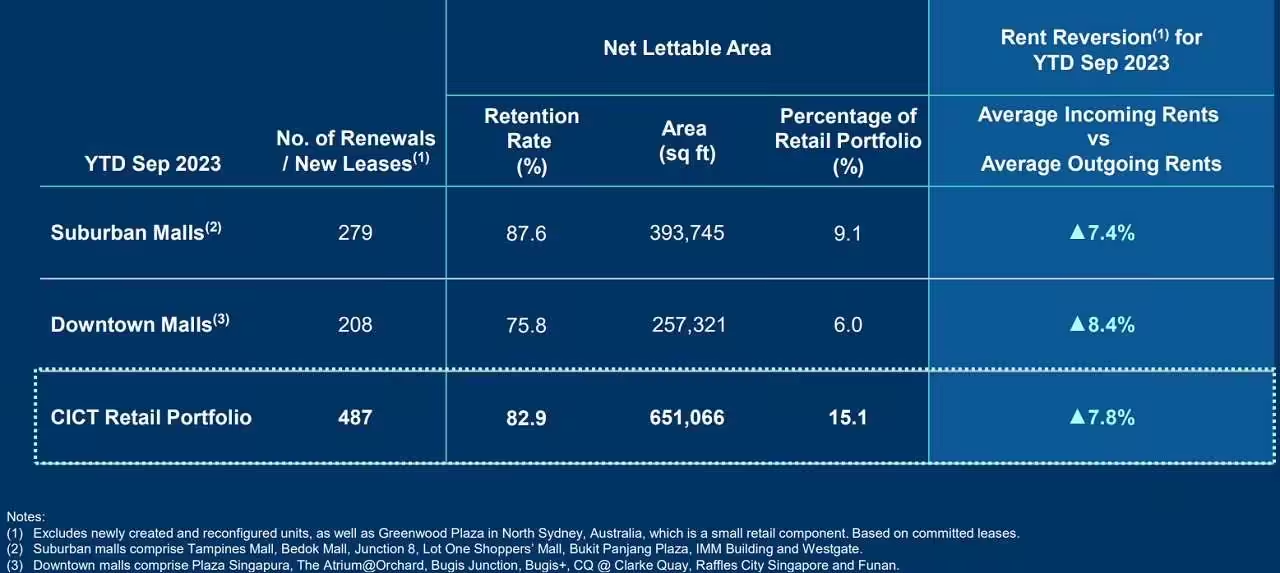

Lease expiry are well-spread and thus nothing is of immediate concern. It was shared by CICT that the retention rate for retail leases and office leases are 82.9% and 90.4% respectively.

A good piece of news from CICT is the positive rental reversion. A positive rental reversion means an increase in rental rates for the REIT, while the converse would be termed negative rental reversion.

Current Dividend Yield

Based on the current share price of S$1.84 and FY22 full year distribution of 10.58 cents, this translate to a current dividend yield of 5.75%.

Summary of CICT 3Q2023 Business Updates

As usual, based on CICT’s 3Q2023 business updates, the pros are:

- Gross Revenue increased 4.6% year-on-year to $391.3 million.

- Net Property Income (NPI) increased 0.6% to S$275.0 million.

- 78% of CICT’s borrowings are hedged at fixed interest rates.

- Long debt average term to maturity of 4.1 years.

- Overall portfolio occupancy stood high at 97.3%.

- Achieved positive rental reversion.

- Current dividend yield of 5.75%.

The cons are:

- High aggregate leverage stood at 40.8%.