On 5th August 2025, CICT (CapitaLand Integrated Commercial Trust) released their 1H2025 financial results. Last year, CICT acquired a 50.0% interest in ION Orchard for S$1,848.5 million. In May 2025, the manager divested 299-unit Service Residence at CapitaSpring. The Net proceeds were used to pare down debt and fund working capital requirements. Recently, the manager also launched a private placement to raise approximately S$500.0 million to finance the proposed acquisition of the remaining 55.0% interest in the office and retail component of CapitaSpring.

On 5th August 2025, CICT (CapitaLand Integrated Commercial Trust) released their 1H2025 financial results. Last year, CICT acquired a 50.0% interest in ION Orchard for S$1,848.5 million. In May 2025, the manager divested 299-unit Service Residence at CapitaSpring. The Net proceeds were used to pare down debt and fund working capital requirements. Recently, the manager also launched a private placement to raise approximately S$500.0 million to finance the proposed acquisition of the remaining 55.0% interest in the office and retail component of CapitaSpring.

Being well-known for Asset Enhancement Initiatives (AEI), CICT has successfully completed the phased AEI works at IMM Building. CICT will also progressively hand over the refreshed space at

Gallileo to the European Central Bank starting in 3Q2025, with the remaining tenants to follow

in 1Q2026. In 4Q2025, CICT will start AIE works on Lot One Shoppers’ Mall and Tampines Mall.

How big is CICT’s portfolio? As of 31st December 2024, CICT’s portfolio comprised of 21 properties in Singapore, two properties in Frankfurt, Germany, and three properties in Sydney, Australia. Currently, CICT is the largest holding in my stock portfolio. As a unitholder of CICT, I am excited to dive into its latest financial results to see how CICT’s divestments and AEI works strategy is helping CICT grow its Distribution Per Unit (DPU) year-on-year.

What is CapitaLand Integrated Commercial Trust share price? What is CapitaLand Integrated Commercial Trust dividend (Distribution Per Unit)? Let us take a look at CICT 1H2025 financial results below to find out these questions.

CICT 1H2025 Financial Results

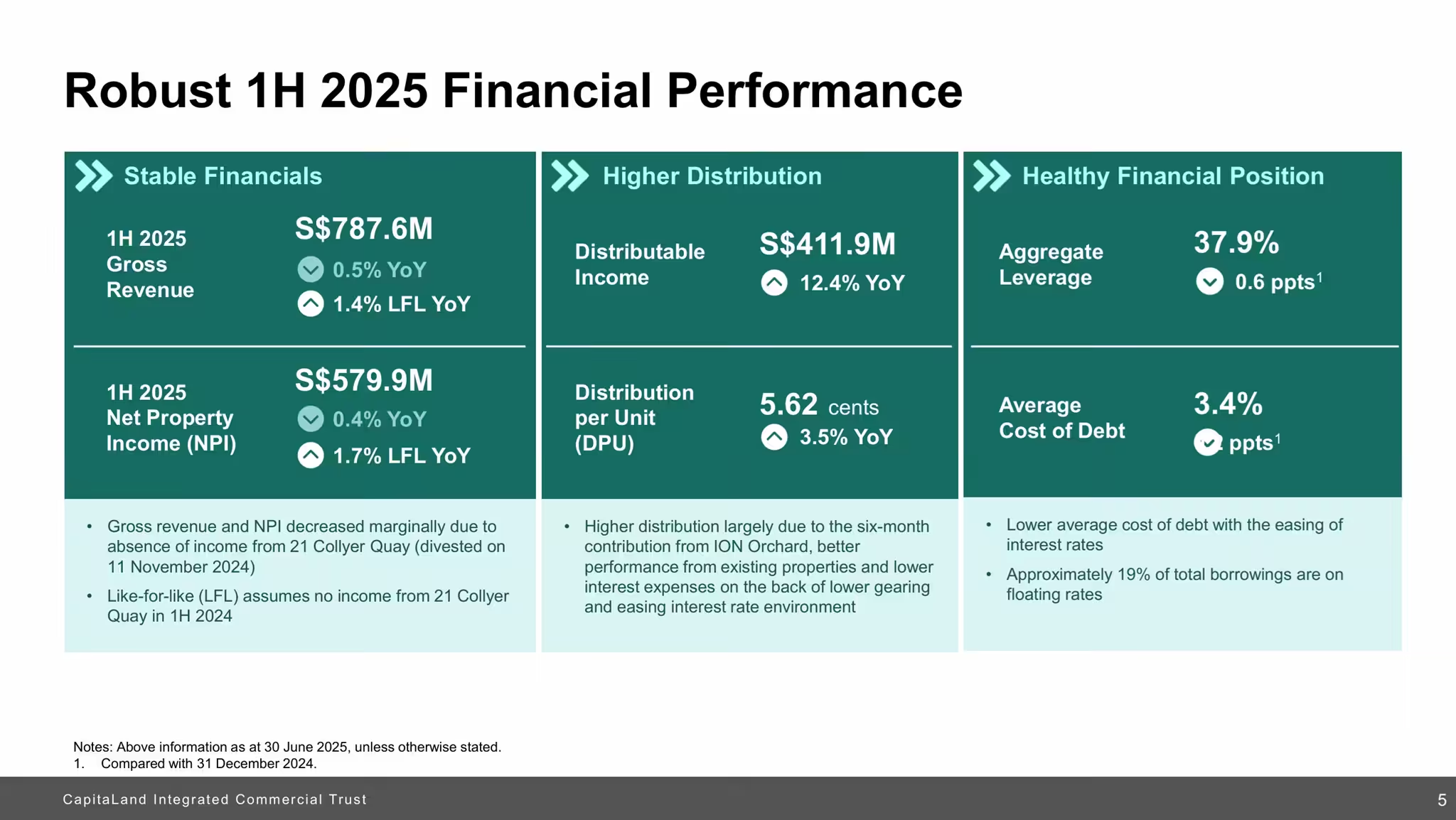

In 1H2025, CICT’s gross revenue fell by 0.5% year-on-year to S$787.6 million, resulting in a corresponding 0.4% year-on-year decrease in its net property income to S$579.9 million. The decline was due to the absence of income from the divestment of 21 Collyer Quay and Gallileo which has been undergoing an asset enhancement initiative since February 2024.

Distributable income grew 12.4% to S$411.9 million. According to the press release, the gain was mainly driven by the acquisition of a 50.0% interest in ION Orchard, better performance of its existing operating properties and lower interest expenses on the back of lower gearing and easing interest rate environment.

CICT’s 1H2025 Distribution Per Unit (DPU) grew 3.5% to 5.62 cents.

| 1H2025 (S$’000) |

1H2024 (S$’000) |

Change (%) | |

| Gross Revenue | 787,646 | 791,961 | (0.5) |

| Net Property Income | 579,865 | 582,364 | (0.4) |

| Amount Available for Distribution | 416,525 | 370,704 | 12.4 |

| Distributable Income |

411,889 | 366,479 | 12.4 |

| Distribution Per Unit (“DPU”) (cents) | 5.62 | 5.43 | 3.5 |

Debt

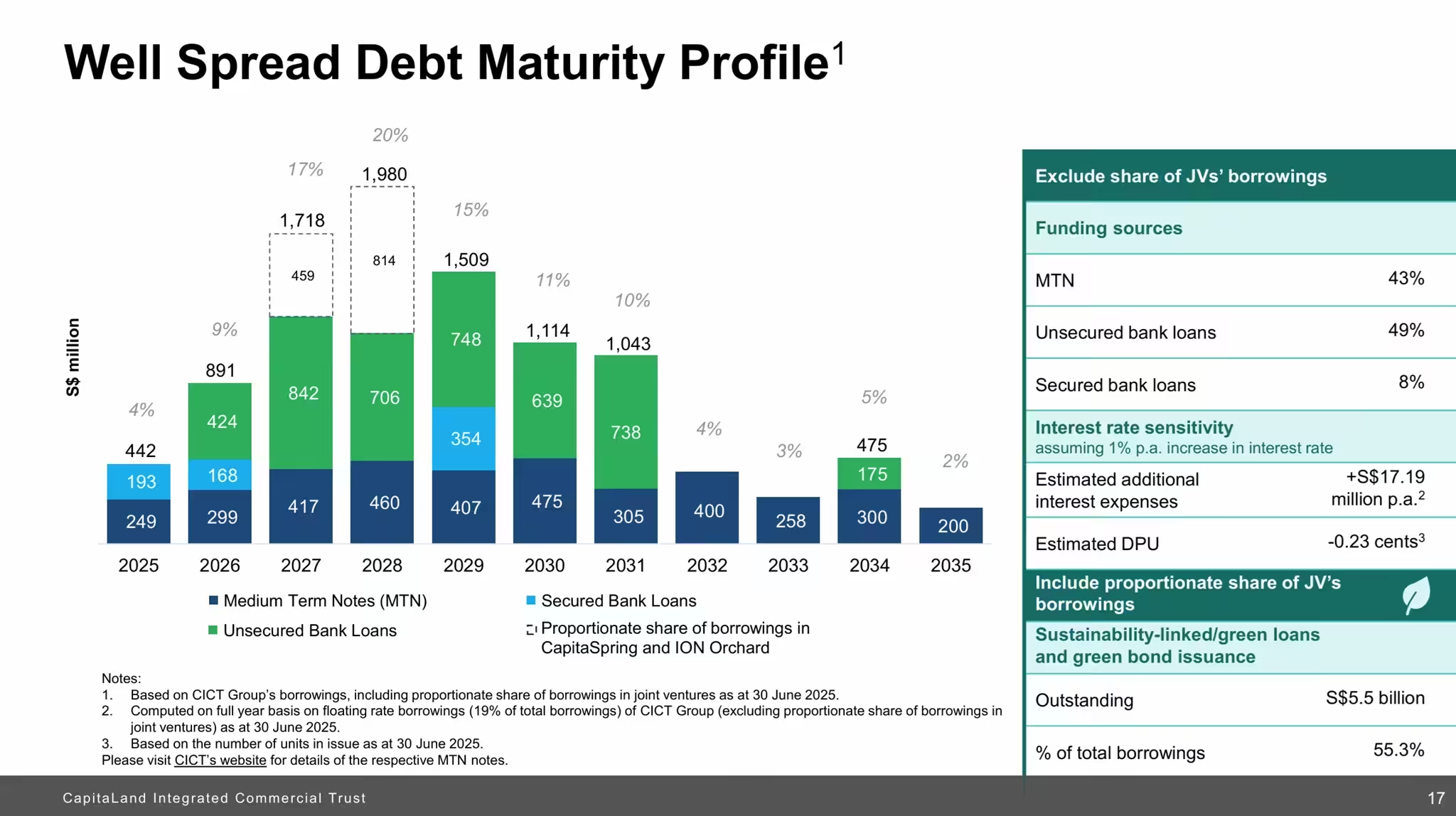

As of 30th June 2025, CICT’s aggregate leverage stood at 37.9%. Average cost of debt was 3.4%, down from the 3.6% as of 31st December 2024. 81% of CICT’s total borrowings remained on fixed interest rates. As you can see from the above chart, CICT’s debt maturity profile is well-staggered across various tenures, with an average term-to-maturity of 4.0 years, reducing refinancing risks in any single year.

Occupancy

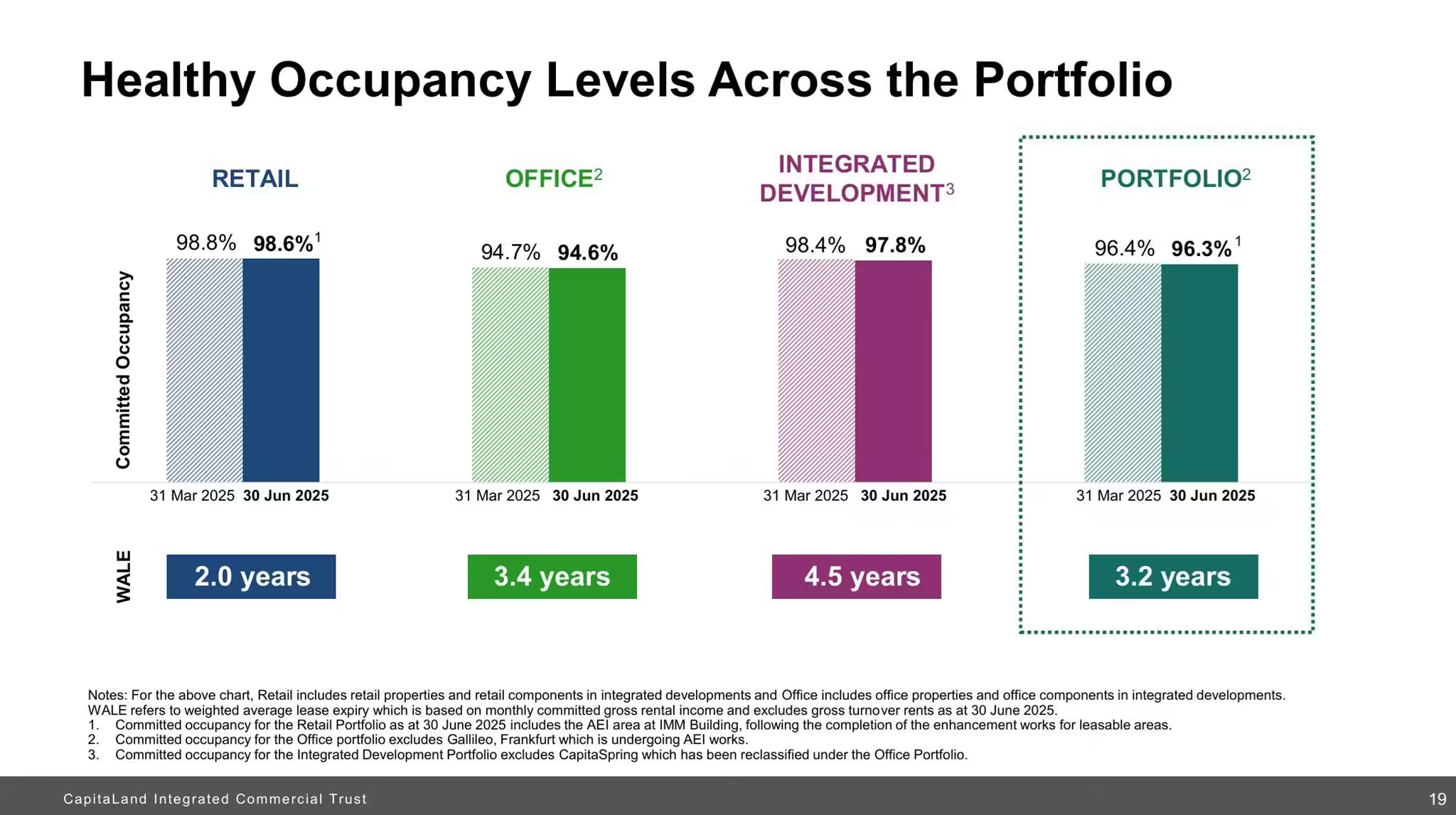

As of 30th June 2025, CICT’s portfolio committed occupancy remained robust at 96.3% with the respective retail, office portfolios and integrated development recording 98.6%, 94.6% and 97.8% respectively. Occupancy declined slightly across all segments as compared to the last quarter.

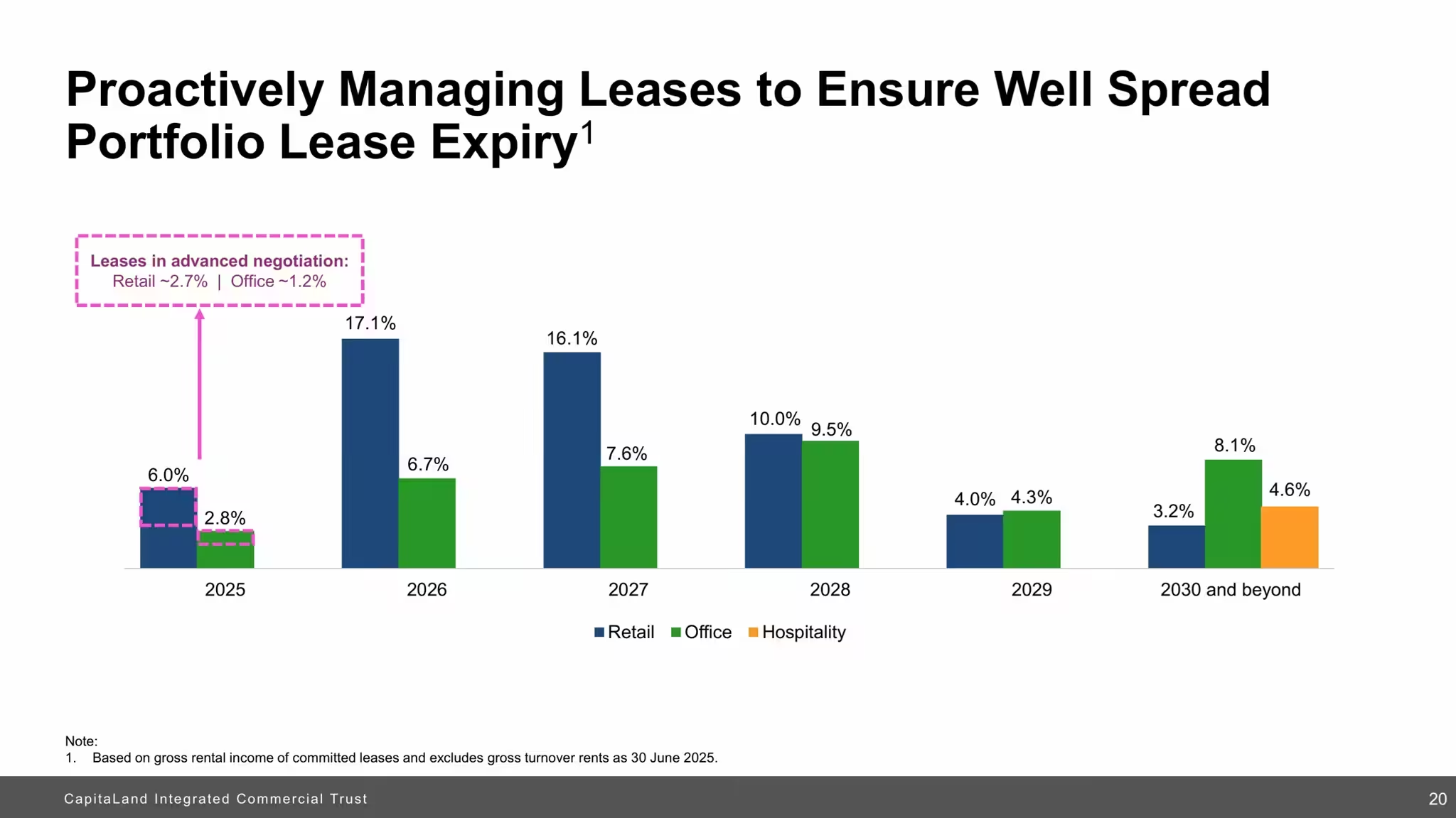

As you can see from the above, lease expiries remained well spread. Singapore retail and office portfolios continued to achieve positive rent reversions of 7.7% and 4.8%, respectively, based on the

average rents of newly signed leases in 1H2025, compared to the average rents of expiring leases.

CICT Share Price and Current Dividend Yield

As you can see from the above chart, CICT share price has been on the uptrend over the past 6 months. CICT share price closed at S$2.26 on Friday, 8th August 2025. Based on CapitaLand Integrated Commercial Trust share price of S$2.26 and FY24 full year DPU of 10.88 cents, CICT dividend works out to be 4.81%.

Summary of CICT 1H2025 Financial Results

We have come to the last section and again I will summarize the pros and cons based on CICT 1H2025 full year financial results. The pros are:

- Distributable income grew 12.4% to S$411.9 million, contributed by ION Orchard.

- Distribution Per Unit (DPU) grew 3.5% to 5.62 cents.

- Healthy aggregate leverage at 37.9%.

- Debt maturity profile is well-staggered.

- CICT’s portfolio committed occupancy remained robust at 96.3%.

- Lease expiries remained well spread.

- Singapore retail and office portfolios achieved positive rent reversions of 7.7% and 4.8% respectively.

The cons are:

- Gross revenue fell by 0.5% year-on-year to S$787.6 million.

- Net property income fell by 0.4% year-on-year to S$579.9 million.

- Based on S$2.26 per share, CapitaLand Integrated Commercial Trust dividend yield is lacklustre at 4.81%.