On 25th April 2025, CICT (CapitaLand Integrated Commercial Trust) announced their 1Q2025 business updates. As this is a business updates, there will be minimal information shared regarding CICT’s financial performance. Currently, CICT makes up 9.08%, which is the largest percentage of my stock portfolio.

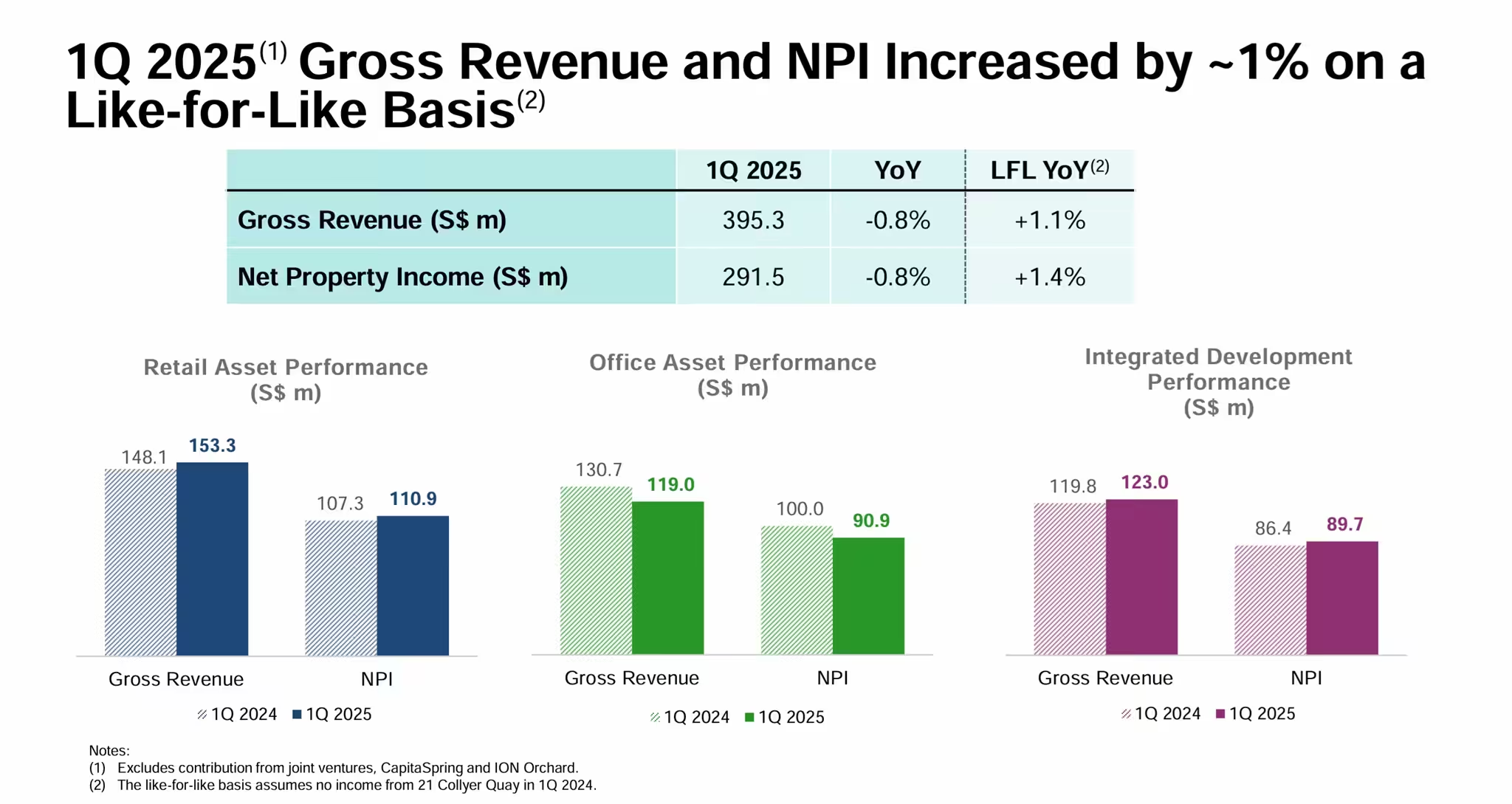

In 1Q 2025, CICT’s gross revenue and net property income declined by 0.8% year-on-year largely due to the absence of income from 21 Collyer Quay which was divested on 11 November 2024. On a like-for-like basis, CICT’s 1Q 2025 gross revenue and net property income were up by 1.1% and 1.4%, respectively. The like-for-like basis assumes no income from 21 Collyer Quay in 1Q2024.

Debt

Moody’s Ratings has affirmed CICT’s A3 rating with a stable outlook on 5 September 2024. Moody’s A3 rating is a medium investment-grade credit rating. It signifies that the issuer has financial backing and some cash reserves, with a low risk of default.

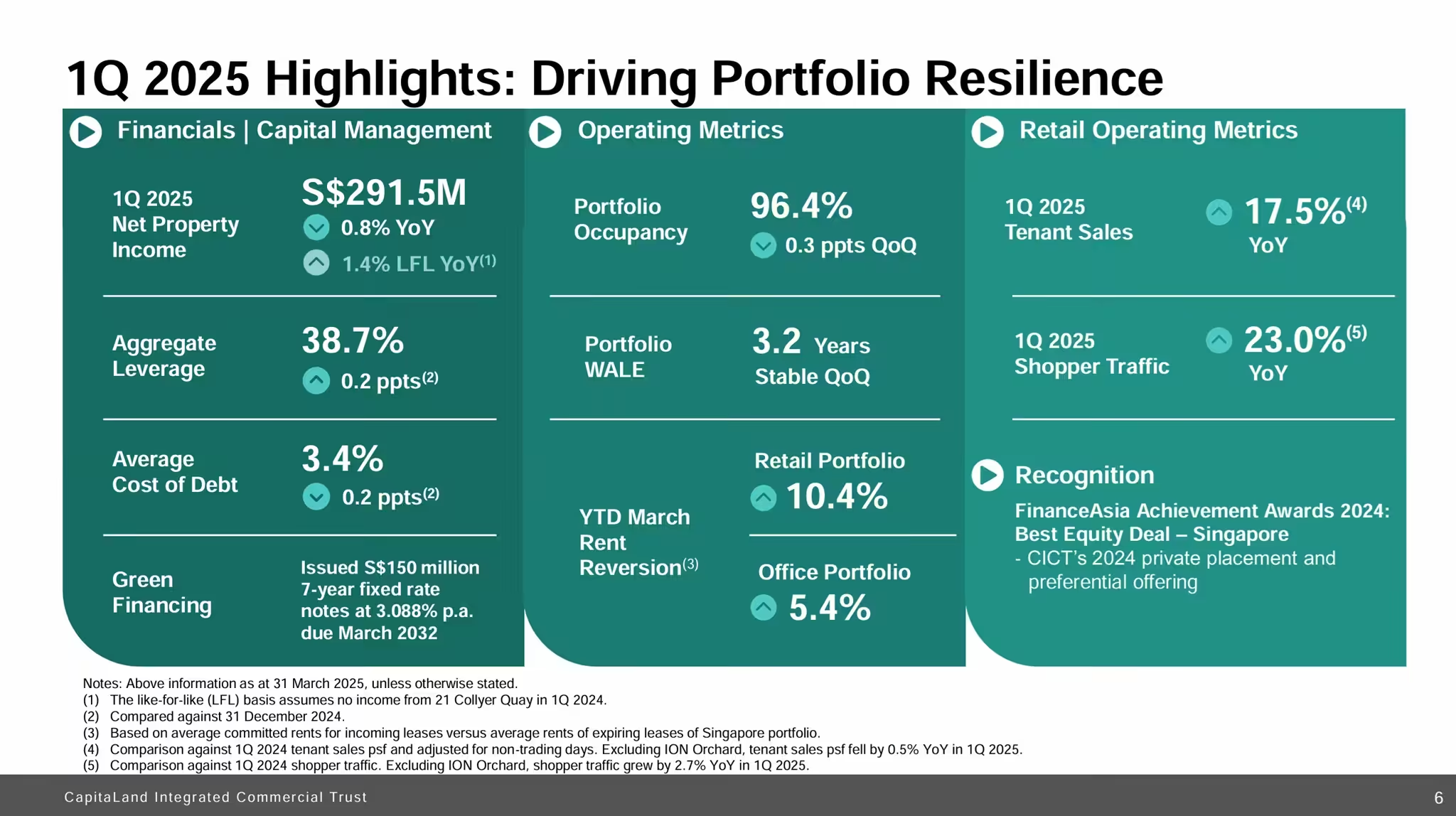

In terms of debt, CICT’s aggregate leverage stood healthy at 38.7%. Aggregate leverage, also known as gearing ratio, refers to the ratio of a real estate investment trust’s (REIT) debt to its total assets.

78% of CICT’s debt are hedged at fixed interest rates which means any sudden fluctuation in interest rates are unlikely to cause any major impact to CICT.

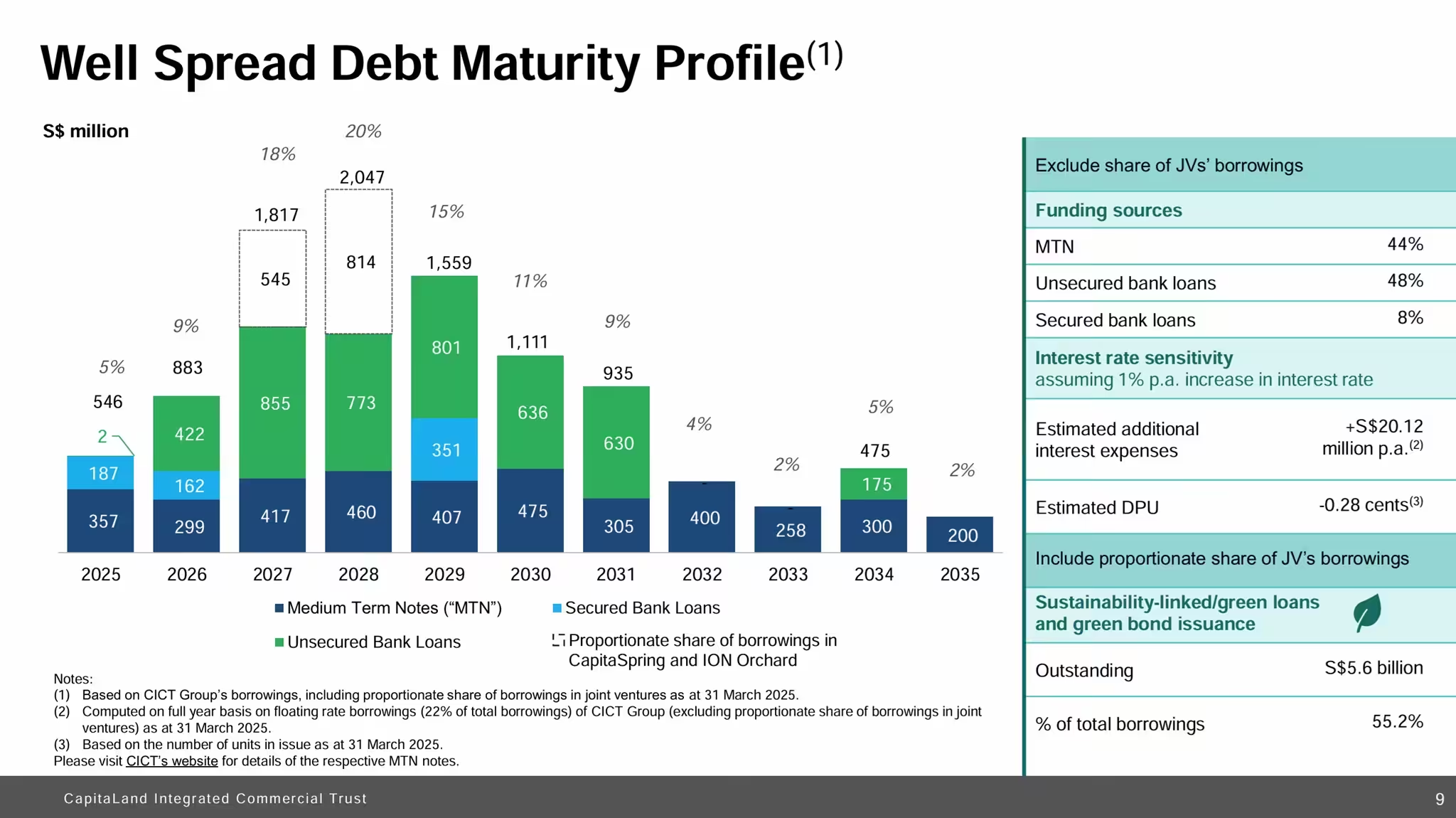

As you can see from the above chart, CICT has a well-distributed debt maturity profile. Having a well-staggered debt maturity profile is crucial for CICT to manage its debt obligations effectively. By spreading out debt repayments over different time periods, CICT can avoid liquidity crunches and reduce the risk of default.

Furthermore, a well-staggered debt maturity profile allows CICT to take advantage of changes in interest rates. For example, if interest rates drop, REITs with debt maturing in the future can refinance at lower rates, reducing their interest expenses.

Occupancy

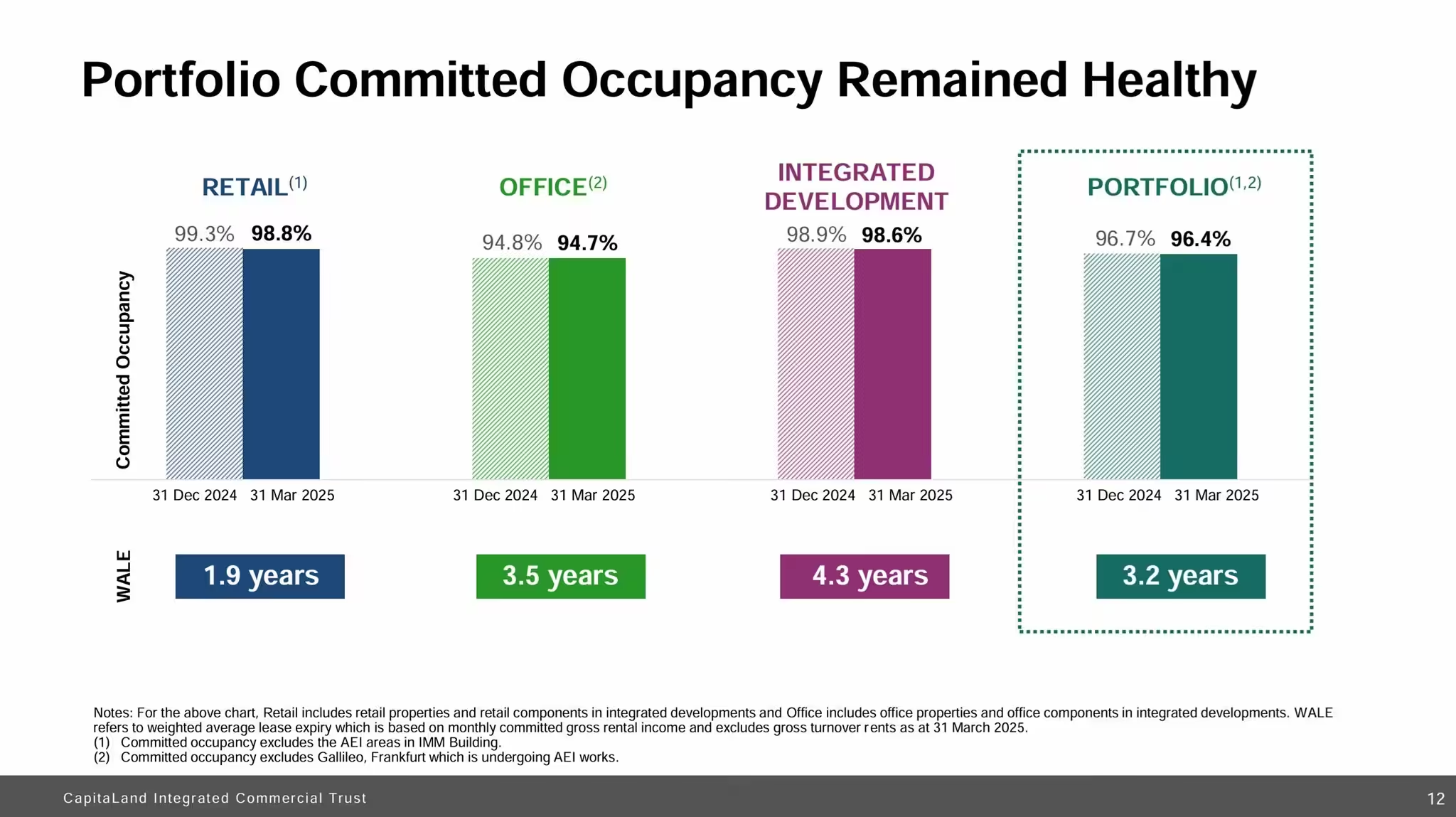

As of 31st March 2025, CICT’s portfolio occupancy stood healthy at 96.4% and Weighted Average Lease Expiry (WALE) stood at 3.2 years.

Weighted Average Lease Expiry (WALE) is a key metric in commercial real estate that measures the average time remaining on leases across a property or portfolio. It helps investors assess the stability of rental income and the risk of vacancies.

WALE is calculated by weighting each lease’s remaining term by either the tenant’s occupied area or rental income. A longer WALE generally indicates lower leasing risk, as tenants are committed to longer contracts, reducing turnover and vacancy concerns.

A WALE of 3.2 years is generally considered moderate, neither particularly long nor short. It suggests that tenants have committed to leases for a reasonable duration, but there is still some turnover risk in the near future.

Short WALE (1-3 years): Indicates higher tenant turnover, which can lead to increased leasing costs and potential vacancies.

Long WALE (5+ years): Suggests stability, with tenants locked into longer contracts, reducing risk.

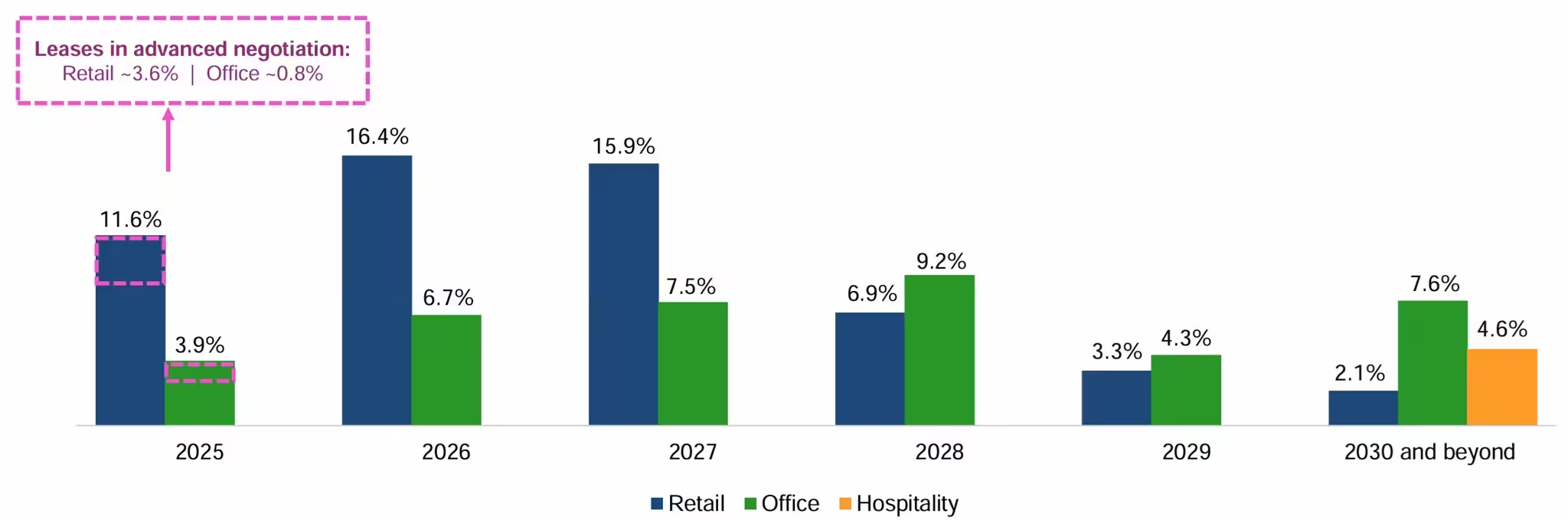

Lease Expiry

CICT’s lease expiry is well-spread and thus nothing is of immediate concern and the manager is in advanced negotiation on the lease renewals.

CICT maintains its positive rental reversion. A positive rental reversion means an increase in rental rates for the REIT, while the converse would be termed negative rental reversion.

CICT Share Price and Dividend Yield

Based on CICT share price of S$2.15 on 2nd May 2025 and FY24 full year distribution of 10.88 cents, CICT’s current dividend yield is 5.06%.

Summary of CICT 1Q2025 Business Updates

We have come to the last section and again I will summarize the pros and cons based on CICT 1Q2025 business updates. The pros are:

- CICT’s aggregate leverage stood healthy at 38.7%. Moody’s gave it a A3 rating with a stable outlook.

- 78% of CICT’s debt are hedged at fixed interest rates to mitigate against sudden interest rate hikes.

- Portfolio occupancy stood healthy at 96.4%.

- Lease expiry is well-spread.

- Moderate WALE of 3.2 years suggesting that tenants have committed to leases for a reasonable duration, but there is still some turnover risk in the near future.

- Maintained its positive rental reversion.

- Acceptable current dividend yield of 5.06% based on S$2.15 per unit.

The cons are:

- Gross revenue and Net Property Income (NPI) declined 0.8% year-on-year due to divestment of 21 Collyer Quay.

- Multiple Asset Enhancements Initiatives to refresh its malls which means temporary loss of income. (AEIs at IMM Building in Singapore and Gallileo in Germany are on track for completion in 2H 2025)