One of my readers asked me for advice on the below scenario that he is facing.

Chance upon your blog since you had one of the REITs that long disposed of but yet I’m still keeping till date (i.e. SoilBuild Business Space REITs). Really enjoy reading your blog and analysis.

I’m 57 years old and currently still in the rat race, having a job that isn’t passionate about and feeling the anxiety and pressure despite already pass the benchmark 55th. I’m not good in investing but saving prudently and working hard, having a bit of equities in CASH, CPF, SRS. Yet the worst performance are those parked in SRS, guess it’s more than 50% lost. The psychologically not willing to let go, couple with the emotional fear of further losing, had since been holding me back from reshuffle the portfolio.

Appreciate any advice you can share.

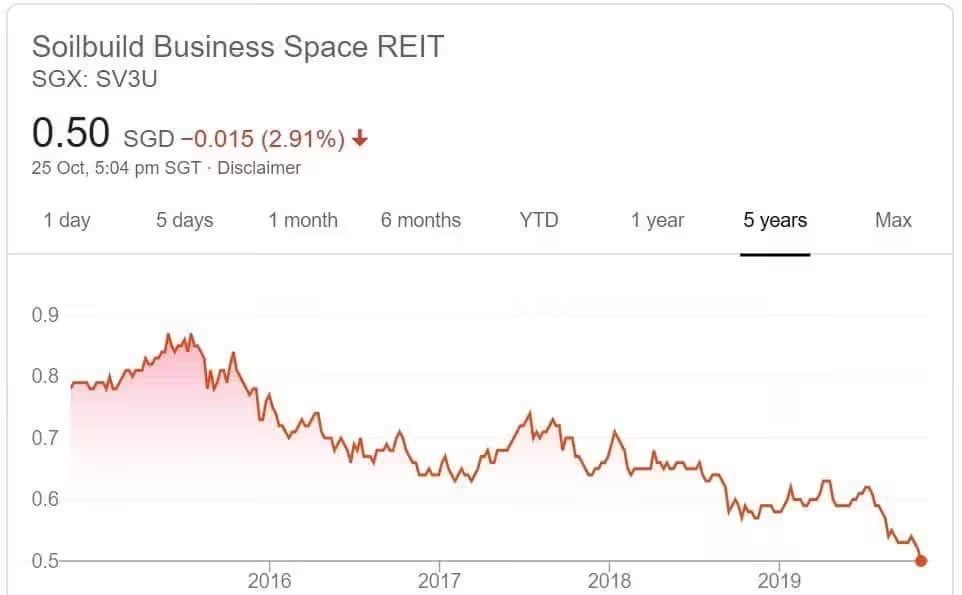

The first problem that he is encountering is that the REIT that he is holding on is actually on a downtrend which is Soilbuild Business REIT which I have sold long ago. Believe me, it was a hard decision to make when I sold off Soilbuild Business REIT at a loss of 11% and I can understand the feeling of holding a REIT whereby you do not know how much further the value will drop. Like I have mentioned in my previous post, Soilbuild Business REIT is in a risky business whereby 11% of its tenants are in the Marine Oil and Gas Business. This puts SoilBuild Business Space REIT in a high risky position should more tenants default their rent.

My advice is to sell off Soilbuild Business REIT and reinvest the monies into something more stable such as healthcare REITs or retail REITs. Avoid industrial and office REITs as these industries tend to be cyclical. There are plenty other REITs out there such as SPH REIT, CapitaMall Trust and Mapletree Commercial Trust whereby there is still further room for growth.

The second problem is what to do with extra Cash, CPF and SRS? Given his age of 57, I would not put my cash into fixed deposits as this will lock down the monies. I will place the extra cash and SRS into Singapore Savings Bond as there is no lock down period which means you can redeem Singapore Savings Bond any time you want without any penalty. I know the interest rate for SRS is petite and if you didn’t know yet, you can invest in Singapore Savings Bond using SRS which should give you an interest rate of 1.62% for a period of 1 year.

Singapore Savings Bond is an extremely safe investment and I hope the above advice helps!

Hi,

My take is to remain invested in Soilbuild Reit and earn the generated dividend. A good stock counter may end becoming a bad counter and the same vice versa. I think that the best approach is to spread the eggs across various baskets and the effect will eventually cancel one another. The main gain will be the generated dividends over the year plus the existing value of the investment portfolio. There is no need for one to monitor the progress on a daily basis. Weekly check is sufficient and one can focus on the things of his/her interest.

WTK

Hi,

I shared with you about my journey investing in SoilBuild Business Space REITs in Oct 2019.

I did not make a disposal then and hold on till now that the REITS has been delisted.

Albeit the capital that I eventually received and the quarterly payouts that I had been collecting over the years are not that awesome but overall I’m still in the black.

Now is to re-invest the returns I got and pick up another REITS counter to generate quarterly income. I did take reference to your portfolio of REIT holdings, but would you share of thoughts and views as to which sector of REITS to invest?

Appreciate your insight sharing. Thank you.

Hi, look at retail reits for stability. I am personally accumulated US Manulife REIT, betting on the recovery and its current attractive dividend yield.

Hi, thank you for your kind sharing.

But US Manulife REIT is transacted in USD. Any REITS with potential capital appreciation and increasing dividends payout in SGD that you are able to advise and share?

Capitaland Integrated Commercial Trust

Thank you for advice and sharing.