On 16th October 2023, Keppel DC REIT released their 3Q2023 Operational Updates. Despite being just an operational update, Keppel DC REIT shared their financial performance.

As you can see from the key highlights above, the financial performance is decent with the exception that DPU declined. In fact, I am expecting the DPU for most REITs to suffer like Keppel DC REIT because of higher financial costs.

As of 30th September 2023, Keppel DC REIT has $3.7 billion worth of assets and 23 data centres across 9 countries under its management.

I have been eyeing Keppel DC REIT for 4 years. Is now the right time to add Keppel DC REIT to my stock portfolio? Let me take a look into more details below to find out if fundamentals are still intact.

Keppel DC REIT 3Q2023 Financial Performance

In 3Q2023, Gross revenue and Net Property Income increased 0.5% and 0.8% respectively as compared to 3Q2022. The increase was attributed to contributions from acquisitions, positive income reversions and income

escalations.

The increase in gross revenue was partially offset by higher finance costs from the refinanced loans, as well as floating interest rates loans. Contributions from some of the Singapore colocation assets were also lower because of higher facilities expenses including electricity costs. Forex hedges was also less favourable.

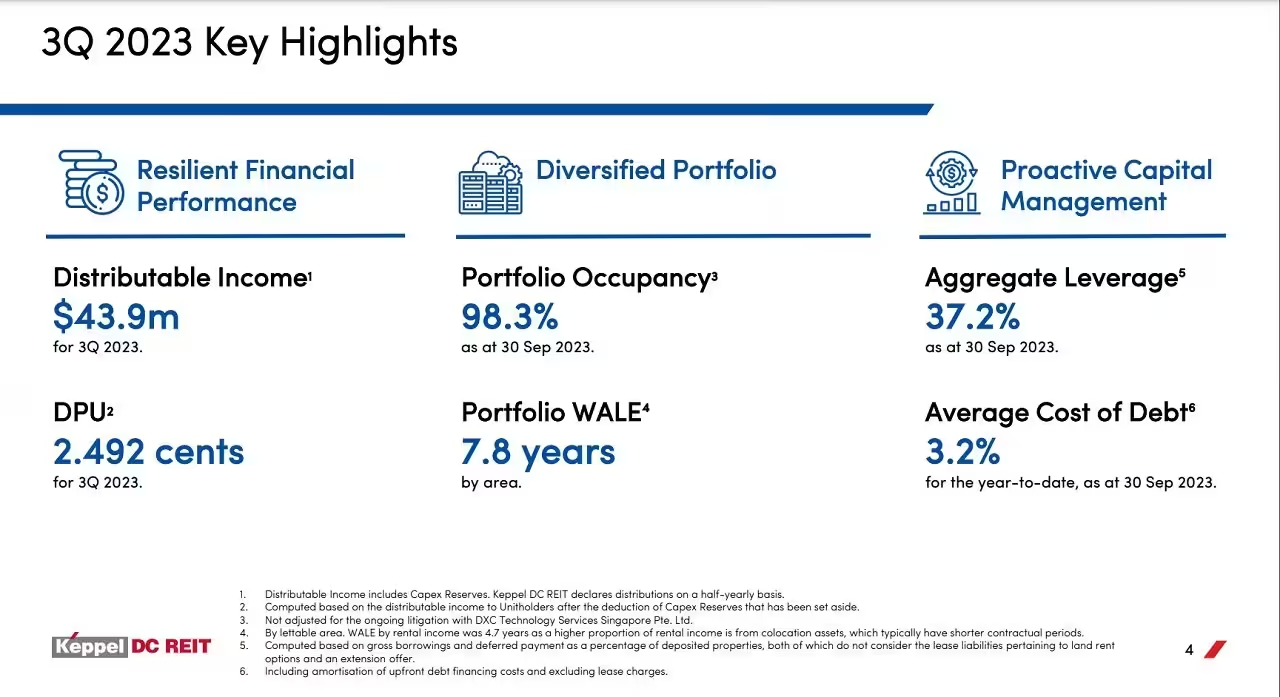

Because of the above negative factors, Distribution Per Unit (DPU) in 3Q2023 fell 3.6% to 2.492 cents as compared to 3Q2022.

| 3Q2023 (S$’000) |

3Q2022 (S$’000) |

Change | |

| Gross Revenue | 70,676 | 70,322 | 0.5% |

| Net Property Income | 64,585 | 64,087 | 0.8% |

| Property expenses |

(6,091) | (6,235) | (2.3)% |

| Distributable Income | 43,876 | 46,943 | (6.5)% |

| Distribution Per Unit (“DPU”) (cents) | 2.492 | 2.585 | (3.6%) |

Debt

As of 30th September 2023, Keppel DC REIT’s gearing ratio stood at 37.2%. There is still available debt headroom of $182m to internal cap of 40%.

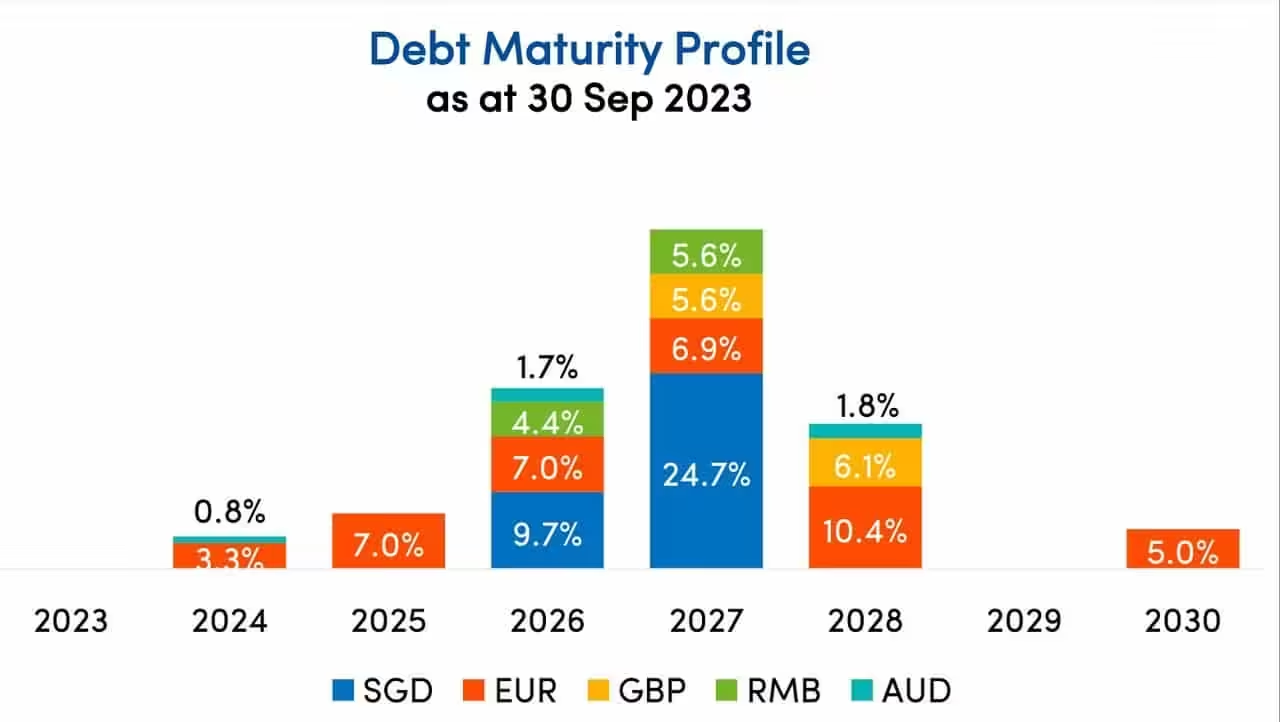

As you can see from the chart above, there is no further refinancing for 2023, bulk of debt expiring from 2026 and beyond.

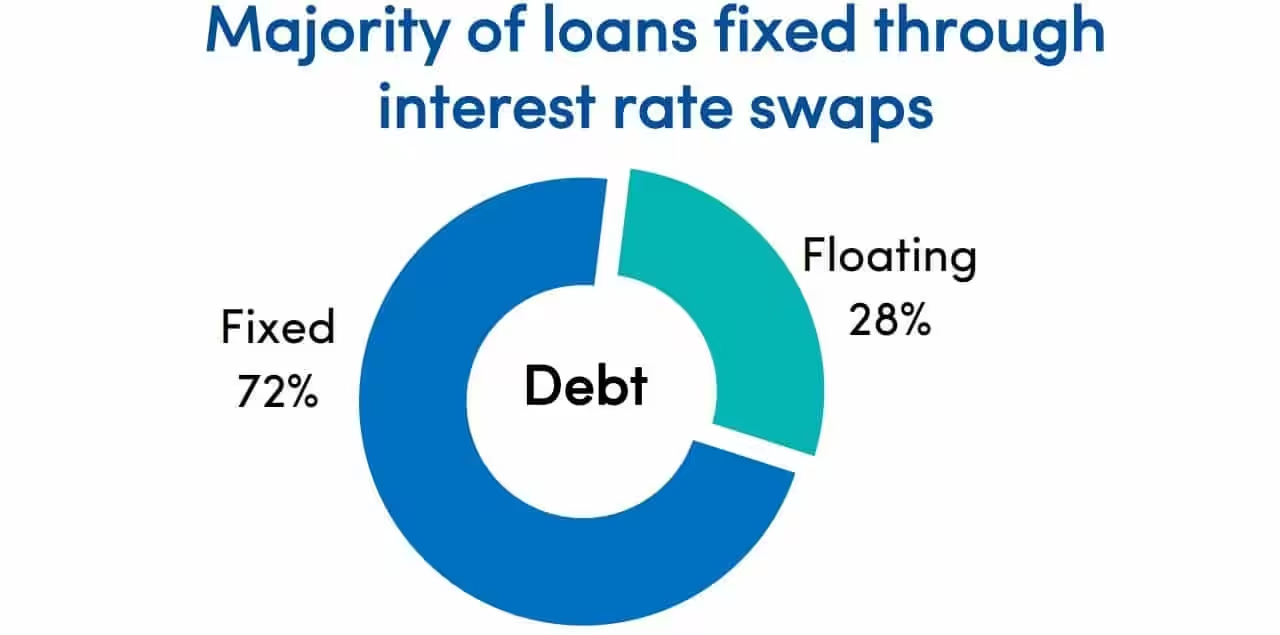

72% of Keppel DC REIT’s debt is hedged at fixed interest rate. This means that an increase in interest rates would only affect the remaining 28% unhedged borrowings. A 100bps increase would have an estimated 2.4% impact to 3Q 2023’s DPU on a pro forma basis.

Occupancy

Keppel DC REIT’s overall portfolio occupancy stood high at 98.3%. Weighted Average Lease to Expiry (WALE) also stood long at 7.8 years, representing income stability.

The manager of Keppel DC REIT also shared that they have secured new and renewal contracts in Singapore, Australia, Ireland and the Netherlands with overall positive reversions.

Keppel DC REIT’s lease expiry profile is well-spread with only 1.1% lease pending renewal in 2023.

Current Dividend Yield

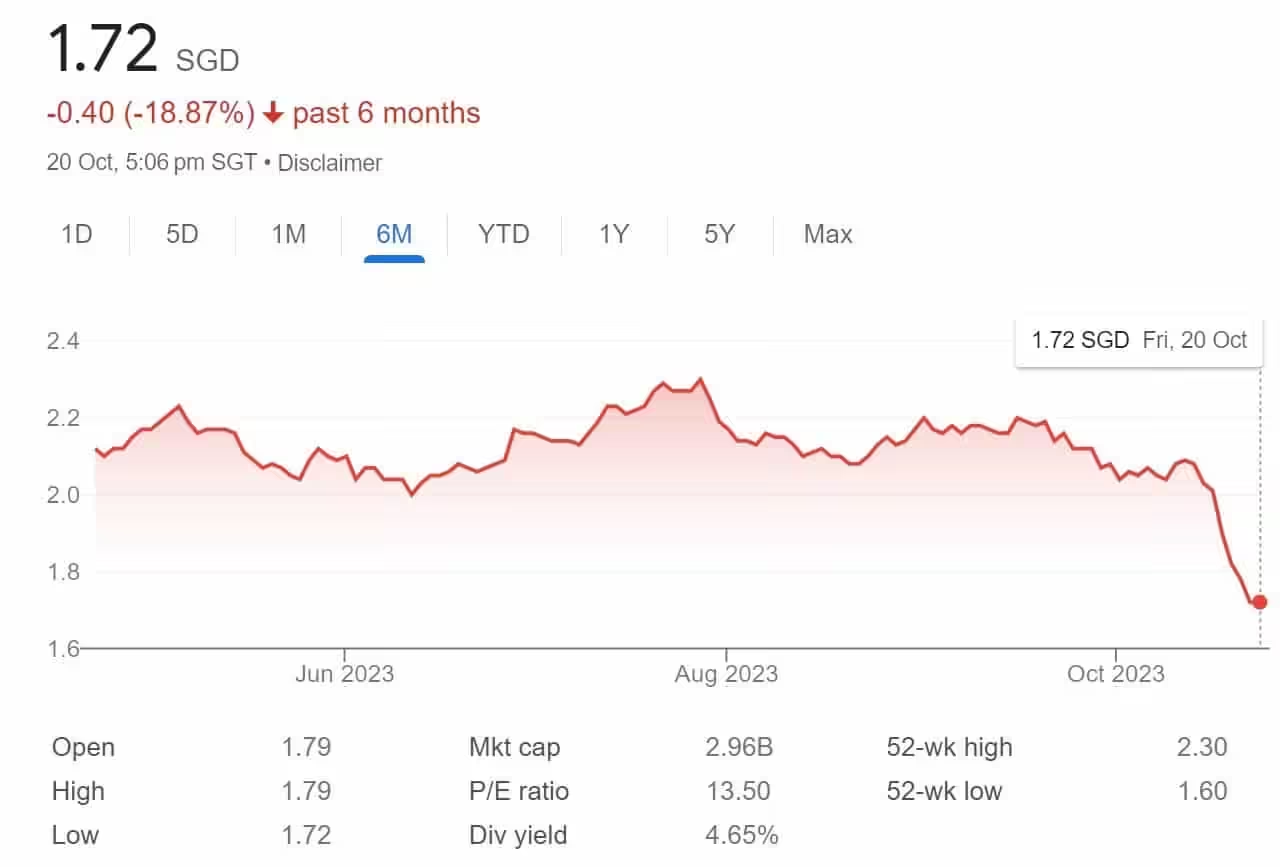

As of 20th October 2023, Keppel DC REIT share price closed at S$1.72 which is very near to its 52 week low of S$1.60.

Based on the closing share price of S$1.72 and FY 2022 full year distribution of 10.214 cents, this translate to a current dividend yield of 5.94%.

In FY2023, I am expecting full year distribution to be lower than FY 2022. Based on the current share price of S$1.72, the estimated dividend yield may range from 5.5% to 5.8%.

Summary of Keppel DC REIT 3Q2023 Operational Updates

As usual, let me summarize the pro and cons based on Keppel DC REIT’s 3Q2023 operational updates.

The pros are

- Gross revenue and Net Property Income increased 0.5% and 0.8% respectively as compared to 3Q2022.

- Keppel DC REIT’s gearing ratio stood at an acceptable range of 37.2%.

- No further refinancing for 2023, bulk of debt expiring from 2026 and beyond.

- Overall portfolio occupancy stood high at 98.3%.

- Weighted Average Lease to Expiry (WALE) also stood long at 7.8 years, representing income stability.

- Lease expiry profile is well-spread with only 1.1% lease pending renewal in 2023.

- Attractive current dividend yield of 5.94%.

The cons are:

- Higher finance costs from the refinanced loans, as well as floating interest rates loans.

- Higher facilities expenses including electricity costs. Forex hedges was also less favourable.

- Distribution Per Unit (DPU) in 3Q2023 fell 3.6% to 2.492 cents as compared to 3Q2022.

I am expecting the share prices to decline further because of the decrease in DPU. Taking opportunity of the weakness, I have added Keppel DC REIT to my stock portfolio.

If the share price decline further, I shall continue my accumulation strategy.