IREIT Global is the first Singapore-listed real estate investment trust (REIT) established with the investment strategy of principally investing, directly or indirectly, in a portfolio of income-producing real estate in Europe that is used primarily for office, retail and industrial (including logistics) purposes, as well as real estate-related assets.

I have done a stock analysis of IREIT Global in July last year. Since then, there has been some changes to the portfolio under IREIT Global which I think is worthy of an update to investors out there.

First, let us look at the FY19 full year financial results. As you can see from the table below, gross revenue increased by 1.3%. Net property income also improved by 0.1%. Distribution Per Unit in € cents declined by 0.6%. The weak EUR/SGD exchange rates caused the Distribution Per Unit in Singapore dollar cents to decline by 2.8%.

FY2019 Full Year Financial Results

| FY2019 (€‘000) |

FY2018 (€‘000) |

Change (%) | |

| Gross Revenue | 35,265 | 34,808 | 1.3 |

| Net Property Income | 30,662 | 30,630 | 0.1 |

| Distributable Income | 22,738 | 22,631 | 0.5 |

| Distribution Per Unit (“DPU”) (€ cents) | 3.57 | 3.59 | (0.6) |

| Distribution Per Unit (“DPU”) (S$ cents) | 5.64 | 5.80 | (2.8) |

Now, let us look at the updates for IREIT Global since my last review.

In December 2019, IREIT Global completed the acquisition of four freehold office buildings located in Spain. This is done via a joint venture whereby IREIT held 40% and 60.0% is held by Tikehau Capital SCA. Prior to the acquisition, IREIT Global own 5 properties. They are Berlin Campus, Bonn Campus, Darmstadt, Münster Campus and Concor Park. The newly acquired four Spain assets are Delta Nova IV, Delta Nova VI, II.Ilumina and Sant Cugat Green.

Debt

The acquisition was funded via a term loan facility of €32m maturing in May 2021. It was mentioned that the manager is looking at further debt to acquire the remaining 60% stake. As of 31st March 2020, the gearing ratio for IREIT Global stood at 38.0% which I am not comfortable with. Further debt could bring the gearing ratio higher.

However, I can see the effort that the manager is trying to bring the debt ratio down from a gearing ratio of 39.3% in December 2019 to the current lower gearing ratio of 38.0%.

Occupancy

As of 31st December 2019, the overall portfolio occupancy stood at 94.6%. The occupancy of the German portfolio stood at 99.7%. You may have guessed it right. The overall portfolio occupancy was dragged down by the Spain’s portfolio occupancy rate. On a positive note, the manager shared that the lower occupancy provides opportunity for rental upside from new leases and positive rental reversions.

As of 31st March 2020, the portfolio occupancy has increased slightly to 94.7%. The occupancy remained bogged down by its Spanish portfolio.

German Portfolio

| BERLIN CAMPUS |

BONN CAMPUS |

DARMSTADT CAMPUS |

MÜNSTER CAMPUS |

CONCOR PARK |

|

| City | Berlin | Bonn | Darmstadt | Münster | Munich |

| Occupancy | 100% | 100% | 100% | 100% | 97.5% |

Spanish Portfolio

| DELTA NOVA IV | DELTA NOVA VI | IL-LUMINA | SANT CUGAT GREEN | |

| City | Mandrid | Mandrid | Barcelona | Barcelona |

| Occupancy | 93.7% | 94.5% | 69.2% | 77.1% |

Portfolio WALE (“Weighted Average Lease Expiry”) remained healthy at 4.2 years with 97.7% of the portfolio leases due for renewal only from FY2022 and beyond.

Management

The effective date of Mr Aymeric Thibord’s cessation as Chief Executive Officer is on 23rd April 2020. Mr Louis d’Estienne d’Orves has taken over the position as Chief Executive Officer of the Manager. Mr d’Estienne d’Orves joined Tikehau Capital’s Real Estate team in November 2018. Before joining Tikehau Capital, Mr d’Estienne d’Orves spent 11 years at AXA IM Real Assets, most recently as the Co-Head of European Transactions – Special Situations.

Current Dividend Yield

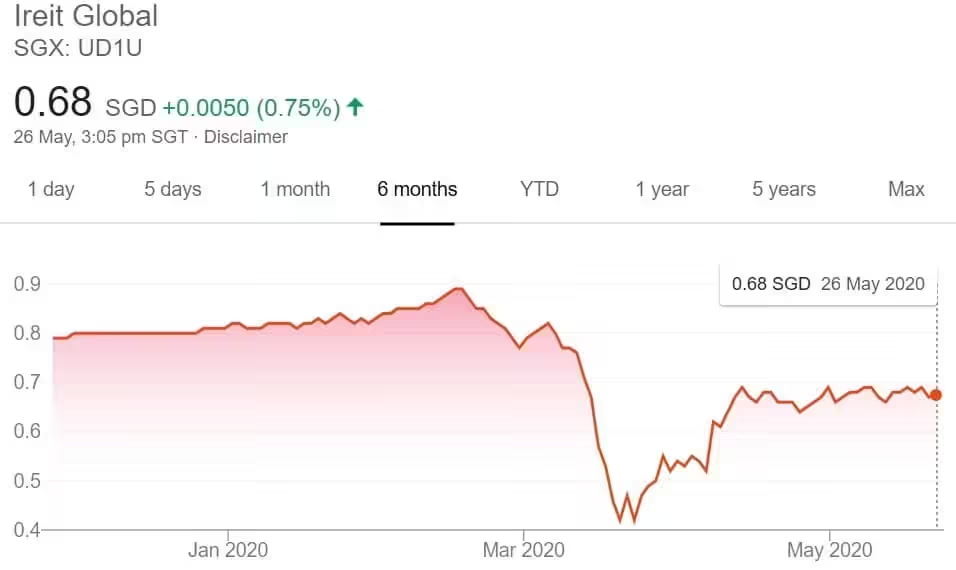

Based on the FY19 distribution pay out of 5.64 cents and current share price of S$0.68, this translate to a current dividend yield of 8.29%. The dividend yield is definitely attractive but of course you need to consider the risks involved such as further weakening of the EUR dollar.

Summary

As mentioned in my last review, IREIT Global has been suffering from lack lustre financial results and year on year distribution per unit has been rather inconsistent.

However, I do notice some positive points worth mentioning on IREIT Global.

- Newly acquired Spanish assets added to the portfolio which is a form of diversification.

- Debt has been reduced to current ratio of 38.0%.

- 96.5% of portfolio leases will be due for renewal only in FY2022 and beyond.

- Tikehau Capital and City Developments Limited (CDL) have substantially increased

their respective unitholdings in IREIT as a vote of confidence, bringing their combined stake to over 50%. Tikehau Capital now owns 29.20% while CDL owns 20.87% of the units in IREIT. - A new unitholder, AT Investments has also acquired a substantial 5.50% stake in IREIT, alongside Tikehau Capital and CDL. AT Investments is owned by Mr Arvind Tiku,

whose family office has an asset portfolio worth approximately US$2bn.

The following are downsides

- IREIT Global is also impacted by the COVID-19 pandemic. As a result of the pandemic, the eurozone economy is expected to contract. This results in the slow down of the take-up of office space and real estate investment in Europe.

- Recent change in CEO means a change of leadership which may take IREIT Global into a different direction. Time will tell.

- Foreign exchange risks (EUR to SGD). Thus, the Distribution Per Unit in SGD may decline further.

There are certainly more positives in IREIT Global than negatives right now. However, as a cautious investor, we should monitor the REIT for a longer period of time. Consistency is the key to success and time will tell whether the manager can turn the assets around.

For those who can’t resist buying into IREIT Global because the share price has been beaten down due to the pandemic, you may wish to split up your purchases over the next few quarters.