![]()

I have been holding M1 for the longest time since 2008 for its good dividend payouts over the years. On 18th October 2016, M1 announced its 3Q2016 financial results. We can see how much the financials have deteriorated. Thus, I made the decision to divest M1 in my stock portfolio.

A telco operator’s revenue is very much predictable based on its prepaid and postpaid revenue. Operating revenue, profit after tax and prepaid, postpaid revenue all fell for M1 over the quarters.

Given the higher risks than benefits, below are few of the reasons I decided to divest M1.

1. Decreasing Operating Revenue

For the nine months ended 30 September 2016, service revenue decreased 1.4% year on year to S$604.5 million.

2. Profit After Tax Fell by 23.4%

Profit after tax (S$m) and margin on service revenue fell as much as 23.4% to S$34.4 million in 3Q2016 as compared to 3Q2015. This is worst than expected by analysts.

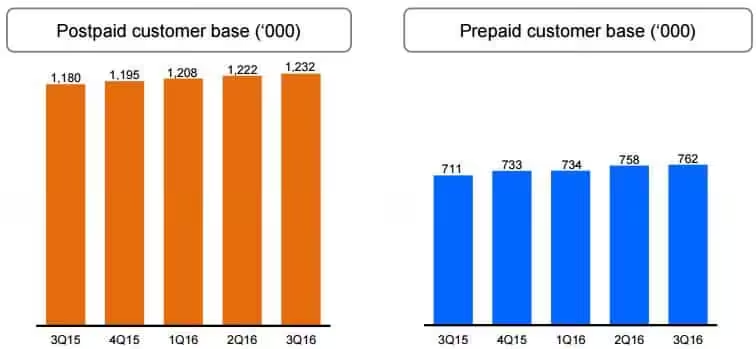

3. Postpaid and Prepaid Revenue Fell

Although customer based can be seen increasing, if we compare 3Q2016 with 3Q2015, postpaid revenue fell 6.1% while prepaid revenue fell 10.4%.

4. Entry of 4th Operator

M1 being the smallest in terms of market share will be most impacted by the entry of the 4th operator. It was speculated the 4th operator will own 7% of the market share in future if it were to come.