On 26th October 2022, Frasers Centrepoint Trust (FCT) announced their 2H2022 financial results. Full year revenue increase 4.6% year-on-year and Net Property Income (NPI) increase 4.9% year-on-year.

Even though FCT has reported a positive full year results, I noticed that the REIT did not perform well in 2H2022 as compared to 2H2021. DPU actually remain almost flat and distributable income had to include previously retained income in order to balance out the books.

Upon digging further, this was because of the absence of contribution from divested properties Bedok Point, Anchorpoint and YewTee Point in FY2021.

Frasers Centrepoint Trust 2H2022 Financial Results

Gross Revenue grew 7.9% to S$180.7 million. Net Property Income grew 6.0% to S$128.1 million.

In 2H2022, Frasers Centrepoint Trust had included $4.8 million of its taxable income available for distribution to Unitholders which was retained in 1H 2022 and retained $1.7 million of its current period tax-exempt income available for distribution to Unitholders.

Without this addition, the distribution to Unitholders would have been lower.

| 2H2022 (S$’000) |

2H2021 (S$’000) |

Change | |

| Gross Revenue | 180,744 | 167,535 | 7.9% |

| Net Property Income | 128,118 | 120,909 | 6.0% |

| Property expenses |

(52,626) | (46,626) | 12.9% |

| Amount Distributable To Unitholders | 103,776 | 103,576 | 0.2% |

| Distribution Per Unit (“DPU”) (cents) | 6.091 | 6.089 | – |

Frasers Centrepoint Trust Full Year FY2022 Financial Results

Gross Revenue for the full year grew 4.6% to S$356.9 million. Net Property Income (NPI) grew 4.9% to S$258.6 million.

Full year Distribution Per Unit (DPU) increased 1.2% to 12.227 cents.

| FY2022 (S$’000) |

FY2021 (S$’000) |

Change | |

| Gross Revenue | 356,931 | 341,149 | 4.6% |

| Net Property Income | 258,597 | 246,567 | 4.9% |

| Property expenses |

(98,334) | (94,582) | 4.0% |

| Amount Distributable To Unitholders | 208,190 | 204,674 | 1.7% |

| Distribution Per Unit (“DPU”) (cents) | 12.227 | 12.085 | 1.2% |

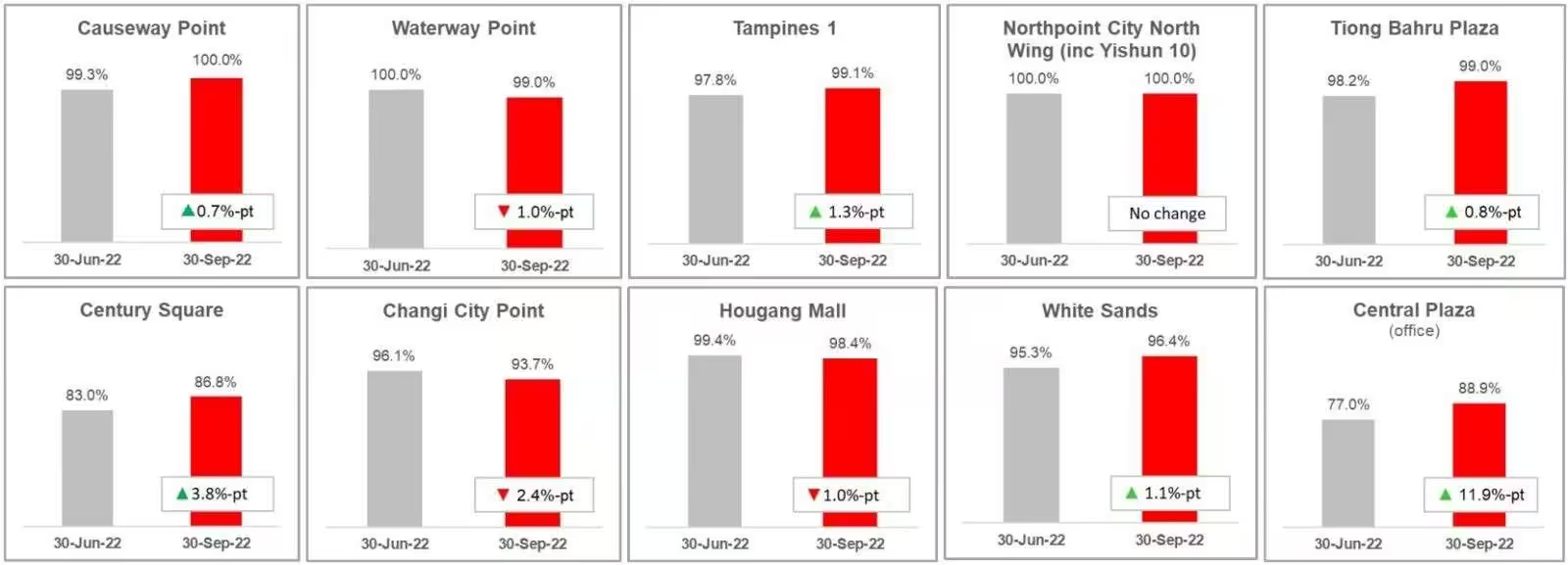

Occupancy

Overall portfolio stood healthy at 97.5%. As you can see below, most of the committed occupancy for its retail malls have risen except for Waterway Point, Changi City Point and Hougang Mall.

Occupancy for Northpoint City stood strong at 100%!

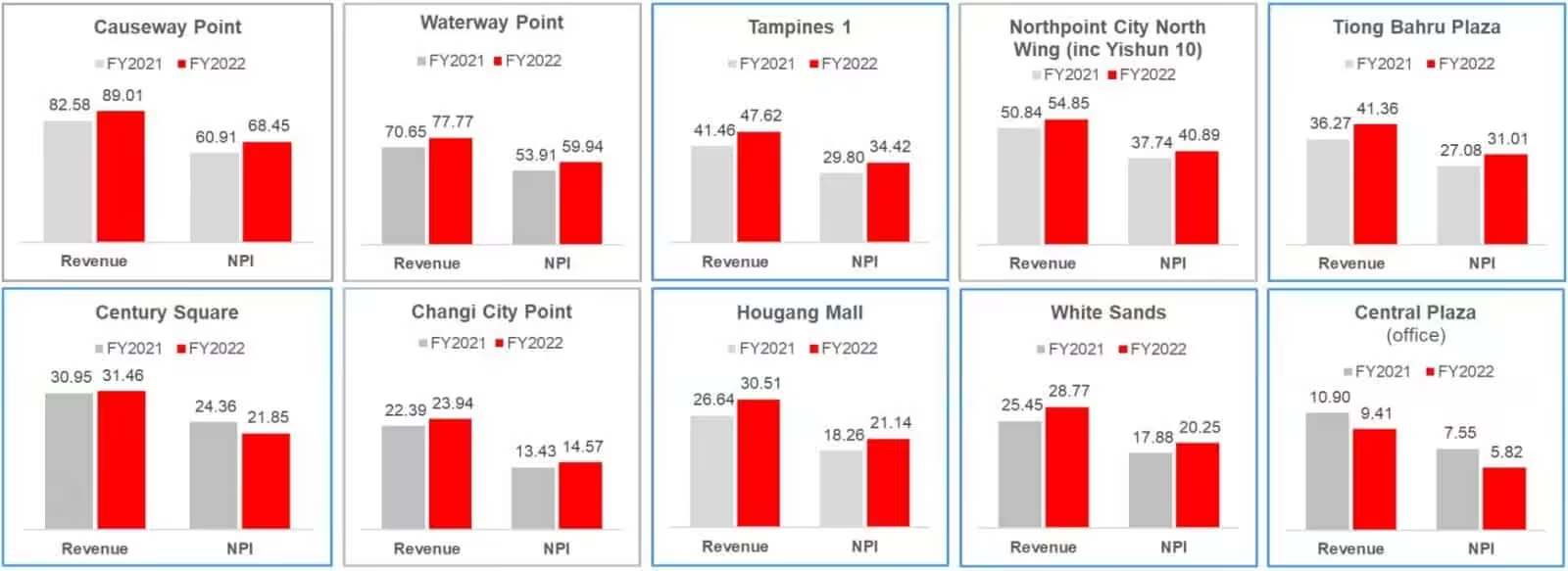

All the properties were able to increase their revenue contribution in FY2022 except for Central Plaza (office).

Debt

Gearing ratio stood at 33.0%. I think this is at a pretty comfortable level and nothing worrying about.

Frasers Centrepoint Trust has a well spread debt maturity profile with 71% of borrowings hedged to fixed rate.

Current Dividend Yield

Based on the full year distribution of 12.227 cents and today’s closing share price of S$2.07, this translate to a current dividend yield of 5.91%.

Summary of Frasers Centrepoint Trust 2H2022 Financial Results

I am glad Frasers Centrepoint Trust has gotten rid of its non performing properties such as Bedok Point, Anchorpoint and YewTee Point from its portfolio.

The manager has added performing malls such Tampines 1, Tiong Bahru Plaza, Century Square, Hougang Mall, White Sands and Central Plaza to its portfolio via acquiring the remaining 63.11% stake in Asia Retail Fund Limited (ARF).

As you can see from above, the full year results is pretty decent even though not excellent. Even though there are continued challenges from the impact of inflation, increase in utilities cost and rising interest rates, I believe Frasers Centrepoint Trust will perform well or even better.

This is on the note that shoppers are returning and this will drive strong sales across all shopping malls.

Agree with you on disposal of Bedok Point, Anchorpoint and YewTee Point. Along with the 10% in Waterway Point, it’ll be even better.