In my last screening for dividend stocks, US Manulife REIT appeared top in the results with 8.736% dividend yield. This has got me interested to drill deeper and understand this REIT further. On a high level note, Manulife US REIT is a Singapore REIT established with the investment strategy principally to invest, directly or indirectly, in a portfolio of income-producing office real estate in key markets in the United States, as well as real estate-related assets.

Manulife US REIT was listed on SGX on 20 May 2016 and is the first pure play US office REIT to be listed in Asia. The IPO price of Manulife US REIT was 0.83 US cents.

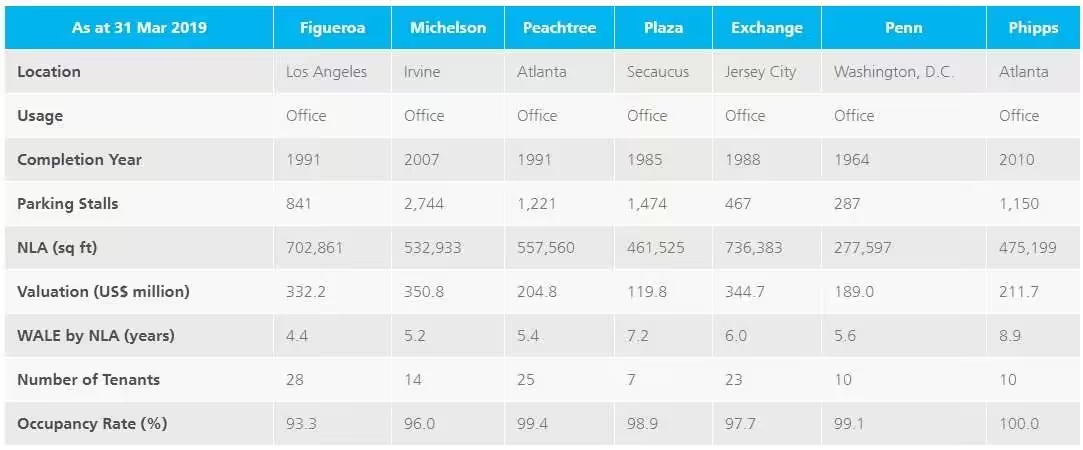

Portfolio

Manulife US REIT comprises of eight office properties in the United States. The portfolio consists of Figueroa in Los Angeles, Michelson in Irvine, Peachtree in Atlanta, Plaza in Secaucus, Exchange in Jersey City, Penn in Washington, D.C. and Phipps in Atlanta. In April this year, Manulife US REIT has announced the acquisition of Centerpointe I & II. This makes a total of eight office properties in its portfolio.

Occupancy

As of 31 March 2019, the overall average occupancy stood at 97.4% which I consider as healthy. In the portfolio, I notice that the occupancy rate of Figueroa is only 93.3%. The Weighted Average Lease Expiry (WALE) is 6.0 years.

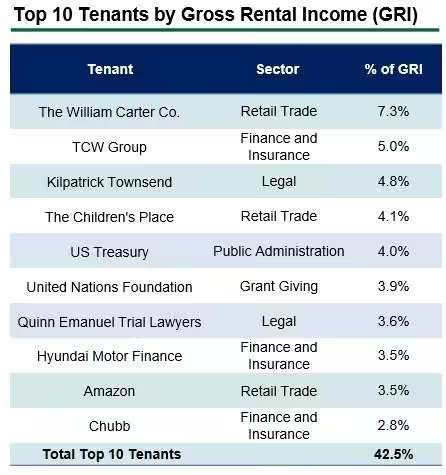

Based on the top 10 tenants, there is no tenant contributing more than 7.3% of gross rental income which means Manulife US REIT is well defended against a major tenant defaulting on its rental.

Financial Summary

Here are the 1Q2019 financial results compared with 1Q2018.

| 1Q2019 (US$’000) |

1Q2018 (US$’000) |

Change | |

| Gross Revenue | 40,025 | 31,153 | 28.5% |

| Net Property Income | 25,084 | 19,650 | 27.7% |

| Distributable Income | 19,343 | 15,633 | 23.7% |

| Distribution Per Unit (“DPU”) (US cents) | 1.51 | 1.50 | 0.7% |

Let us look at the full year 2018 versus 2017 financial results.

| 2018 (US$’000) |

2017 (US$’000) |

Change | |

| Gross Revenue | 144,554 | 92,040 | 57.1% |

| Net Property Income | 90,665 | 58,351 | 55.4% |

| Distributable Income | 70,981 | 46,716 | 51.9% |

| Distribution Per Unit (“DPU”) (US cents) | 5.57 | 5.77 | (3.5%) |

| Distribution Per Unit (“DPU”) (US cents) *Adjusted | 6.05 | 5.84 | 3.6% |

* FY 2018 DPU was lower than FY 2017 DPU largely due to the enlarged Unit base from the issuance of Preferential Offering to partially fund Penn and Phipps acquisitions, but income contribution from

Penn and Phipps was only from acquisition date on 22 Jun 2018.

All financial results are positive which is a good sign the REIT is coping well.

Distribution History

As Manulife US REIT is only listed in 2016, there is not much distribution history to do a comparison if Manulife US REIT can grow its DPU year on year. Based on the adjusted DPU, distributions increased by 3.6% if we compare FY18 and FY17.

| FY18 | FY17 | FY16 (3Q and 4Q) | |

| Distribution (US cents) | 6.05 * | 5.84 * | 3.55 |

* Please note that I have used the adjusted DPU in the distribution history to account for the preferential offering.

Debt

Based on 1Q2019 financial results, the gearing ratio stood at 37.6% which means there is still a slight headroom for further debt. Below shows the debt maturity profile which is well spreaded.

Management

We all know about Manulife. The sponsor’s parent company, Manulife Financial Corporation (MFC), is a leading international financial services group providing forward-thinking solutions to help people with big financial decisions. It operates as John Hancock in the U.S., and Manulife elsewhere providing financial advice, insurance and wealth and asset management solutions for individuals, groups and institutions.

US Manulife REIT is managed by Manulife US Real Estate Management Pte. Ltd. (the Manager) which is wholly owned by the Sponsor, The Manufacturers Life Insurance Company (Manulife), part of the Manulife Group.

The REIT has a strong sponsor.

Current Valuation

Based on the total DPU of 5.57 US cents and current share price of 0.84 USD, this translates to a dividend yield of 6.63%.

Let’s compare US Manulife REIT with a similar REIT such as Frasers Commercial Trust. The current share price of Frasers Commercial Trust is S$1.47 and based on the FY18 total distribution per unit of 9.60 cents, the current yield of Frasers Commercial Trust is 6.53%.

Thus, US Manulife REIT in terms of dividend yield is slightly higher.

Conclusion

At 6.63% dividend yield, this is definitely attractive as compared to other REITs. Manulife US REIT does not have much historical results to look at given that it only IPO in 2016. A quick glance at its financial results shows that it has performed well in the short span of 3 years.

The current share price has also not appreciated much above its IPO price of 0.83 US cents which pose a good opportunity to invest early and hold while it continues its growth.

The risk of investing in this pure US play is any hiccups or announcement in the US economy will hit Manulife US REIT hard. The pros of investing in this REIT is that the US economy is doing well under Trump’s administration with employment rate falling and jobs returning to the US. This is definitely a boost for Manulife US REIT.

I will keep this in my watch list given the attractive dividend yield, decent financial results and the growth opportunity in Manulife US REIT.

Hi there, I was thinking either your dividend per unit is very conservative or you might get it wrong. Wouldn’t it be closer to 6 cents?

Hi Kyith, if you are refering to the 6.05 US cents, that was what was listed in their financial results presentation.

Thank you for the sharing!

I am just starting to look into US office reits and would really appreciate your thoughts.

Looking at the share prices, the 3 performed very widely over the last 6 months:

Keppel Pacific Oak (CMOU) gained 24.5%

Prime US Reit (OXMU) gained 16.7%

Manulife US (BTOU) gained 2.7%

Manulife is the largest of the 3, with trophy class assets, yet is the worst performing.

Any idea why the huge disparity? Appreciate your thoughts!