I was casually screening for office REITs to add to my stock portfolio when I came across IREIT Global. Based on what I read about, the dividend yield of IREIT Global was estimated to be as high as 8%. The thought of “Is it really true?” came across my mind as most of the dividend yields of the REITs that I know of has dividend yield ranging from 4.7% to 5.5% given the current run up in most REIT prices which in turn cause the dividend yield to decline.

On 30 April 2019, IREIT announced the introduction of a new strategic investor, City Developments Limited (CDL), which has acquired a 50% stake in the Manager and 12.4% stake in IREIT units.

In summary, IREIT Global is the first Singapore-listed real estate investment trust (REIT) established with the investment strategy of principally investing, directly or indirectly, in a portfolio of income-producing real estate in Europe that is used primarily for office, retail and industrial (including logistics) purposes, as well as real estate-related assets.

IREIT Global initial offering was S$0.88 back in August 2014.

Portfolio

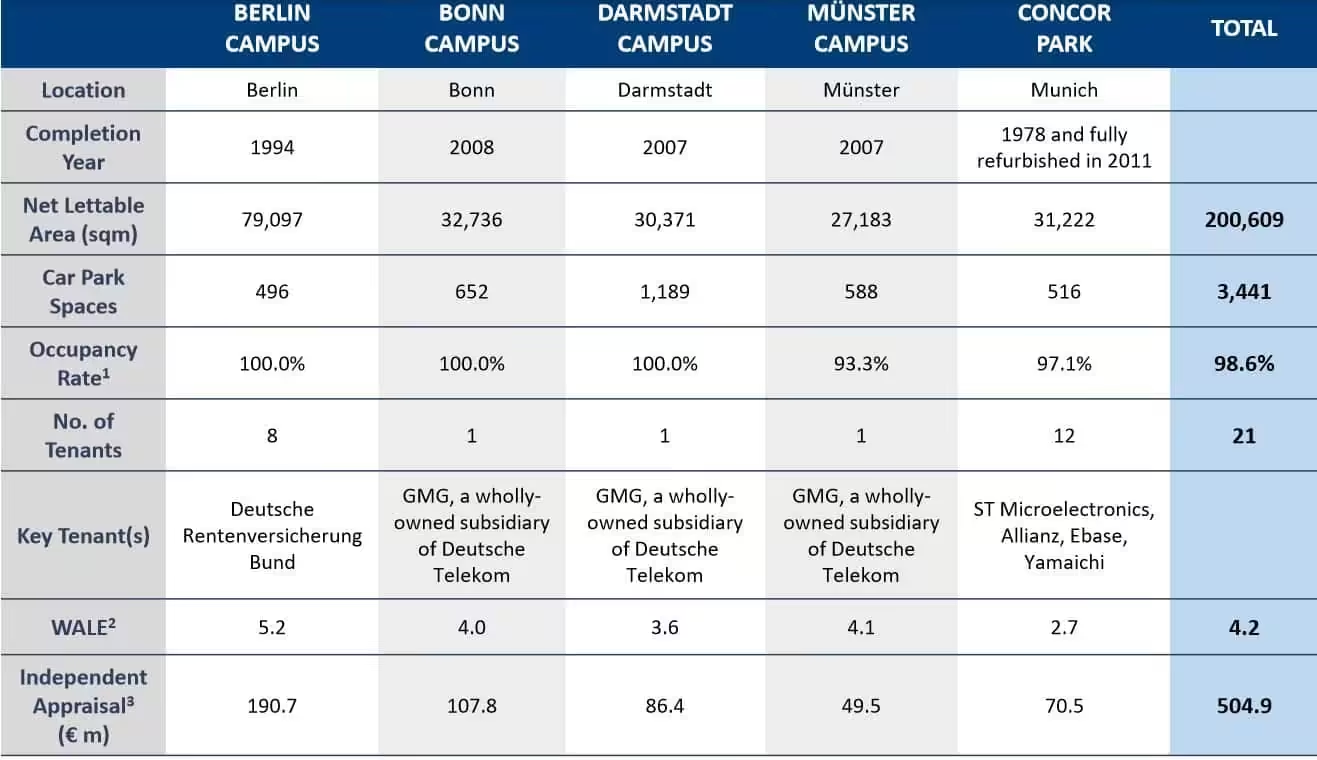

IREIT Global’s portfolio consists of 5 freehold office assets in Germany, with total NLA of c.200,600 sqm and valuation of €504.9m. The 5 properties are Berlin Campus, Bonn Campus, Darmstadt, Münster Campus and Concor Park.

Occupancy

As of 31st March 2019, the overall occupancy is 98.6% which I consider to be healthy. I noticed that there is only 1 major tenant (GMG, a wholly owned subsidiary of Deutsche Telekom) for Bonn Campus, Darmstadt Capmus and Münster Campus.

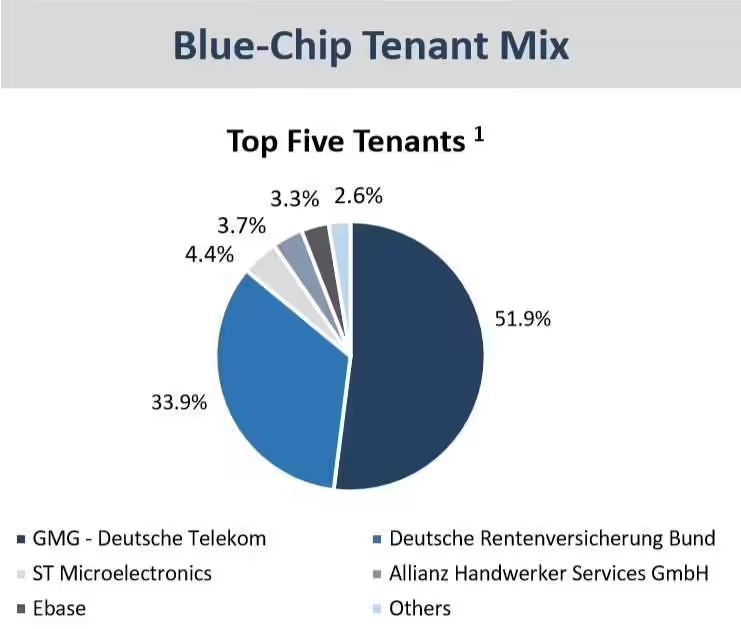

As shown below, GMG Deutsche Telekom makes up 51.9% of IREIT Global’s gross rental income. The risk here is IREIT Global is highly dependent on rental income from GMG Deutsche Telekom and in the event there is a loss of rental income from GMG Deutsche Telekom, this will have a high impact on IREIT Global.

Here are some basic information about the top 5 tenants.

Financial Summary

Here are the 1Q2019 financial results compared with 1Q2018. The results does not seem so rosy. Distribution Per Unit (DPU) in EUR decline by 1.0% and Distribution Per Unit (DPU) in S$ terms was impacted by weaker SGD/EUR exchange rates.

| 1Q2019 (€‘000) |

1Q2018 (€‘000) |

Change | |

| Gross Revenue | 8,696 | 8,579 | 1.4% |

| Net Property Income | 7,587 | 7,727 | (1.8)% |

| Distributable Income | 5,657 | 5,684 | (0.5)% |

| Distribution Per Unit (“DPU”) (€ cents) | 0.99 | 1.00 | (1.0)% |

| Distribution Per Unit (“DPU”) (S$ cents) | 1.58 | 1.63 | (3.1)% |

Let us look at the full year 2018 versus 2017 financial results. The full year results does not seem so bright either. Revenue, Net Property Income and DPU declined.

| 2018 (€‘000) |

2017 (€‘000) |

Change | |

| Gross Revenue | 34,808 | 34,959 | (0.4)% |

| Net Property Income | 30,630 | 31,528 | (2.8)% |

| Distributable Income | 22,631 | 23,378 | (3.2)% |

| Distribution Per Unit (“DPU”) (€ cents) | 3.99 | 4.15 | (3.9%) |

| Distribution Per Unit (“DPU”) (S$ cents) | 6.46 | 6.44 | 0.3% |

Distribution History

The distribution yield is as high as 8% based on IREIT’s FY2018 DPU of 5.80 Singapore cents and closing unit price of SGD0.725 as at 31 December 2018. There is a distribution policy of at least 90% of annual distributable income whereby the distributions are to be made on a semi-annual basis.

The distribution per unit in Euro cents seems to be on a decline since FY2016.

| FY2014 | FY2015 | FY2016 | FY2017 | FY2018 | |

| Distribution Per Unit (“DPU”) (€ cents) | 1.53 | 3.39 | 4.14 | 3.72 | 3.59 |

| Distribution Per Unit (“DPU”) (S$ cents) | 2.57 | 5.24 | 6.33 | 5.77 | 5.80 |

Debt

IREIT Global has a gearing of 38.0%. While other REITs are parring down its debt, the current gearing seems high for IREIT Global. Weight Average Debt Maturity stood at 6.8 years.

Management

Mr Aymeric Thibord took over as the Chief Executive Officer of IREIT Global since 2016. He has 20 years of experience, having worked for several major real estate investors such as Archon Group France (Goldman Sachs’ real estate arm) and Société Générale Asset Management.

Mr Choo Boon Poh is the Chief Financial Officer. He has more than 18 years of experience in audit, banking and corporate finance-related work. Previously served as Director of Corporate Finance for Southeast Asia with BNP Paribas Capital (Singapore) Ltd. Focusing mainly on the real estate sector and REIT transactions, he and his team successfully launched several initial public offerings of REITs in Singapore.

Overall, the management is decent with no bad track records.

Current Valuation

Based on the current share price of S$0.78 and past distribution of 5.80 cents, this translates to a current dividend yield of 7.44%.

Summary

In current market conditions, it certainly is hard to find a REIT that gives you 7.44% yield. I have observed that the past distribution is actually not consistent which means DPU is not growing year on year. The distribution is also subjected to the forex risk (EUR to SGD).

Even though the tenants are of quality tenants (blue chips), I personally feel that there is a lack of tenant mix. The pull out of GMG Deutsche Telekom as a tenant can have a major impact on the rental revenue.

I am not sure how IREIT Global will restructure itself or its portfolio with the introduction of the new strategic investor City Developments Limited (CDL) but it may still be early to jump into IREIT Global just because of CDL.

I probably give IREIT Global a miss as there seems to be too much uncertainty and risk for my current appetite.

Good sharing, thanks!

Hi, would you be able to share on some of the taxation risks for IREIT concerning their german assets?

Hi Freddy, I am afraid I am not be able to advise. I have not been following up on IREIT Global since the last analysis.