On 31st January 2023, MPACT (Mapletree Pan Asia Commercial Trust) has released their 3Q FY22/23 financial results. Net Asset Value per Unit was up year-on-year to S$1.78 mainly due to higher investment properties resulting from the merger.

Gross revenue and Net Property Income (NPI) was up 84.0% and 76.8% year-on-year respectively. However, Distribution Per Unit (DPU) remain flat at 2.42 cents.

Let us take a look in more details below if MPACT is doing alright or anything we should be cautious of.

MPACT 3Q FY22/23 Financial Results

In 3Q FY22/23, even though Gross Revenue was lifted by the full quarter contribution from properties acquired through the merger and higher contribution from the Singapore portfolio, the Distribution Per Unit (DPU) was dampened by higher finance costs.

| 3Q FY22/23 (S$’000) |

3Q FY21/22 (S$’000) |

Change | |

| Gross Revenue | 239,752 | 130,277 | 84.0% |

| Net Property Income | 179,389 | 101,450 | 76.8% |

| Property expenses |

(60,363) | (28,827) | 109.4% |

| Amount Distributable To Unitholders | 127,038 | 80,347 | 58.1% |

| Distribution Per Unit (“DPU”) (cents) | 2.42 | 2.42 | – |

MPACT YTD FY22/23 Financial Results

Now, let us take a look at MPACT YTD FY22/23 financial results. Even though operating cost was higher, MPACT still managed to achieve a DPU increase of 8.1% y-o-y.

| YTD FY22/23 (S$’000) |

YTD FY21/22 (S$’000) |

Change | |

| Gross Revenue | 592,914 | 373,999 | 58.5% |

| Net Property Income | 454,564 | 291,305 | 56.0% |

| Property expenses |

(138,350) | (82,694) | 67.3% |

| Amount Distributable To Unitholders | 328,008 | 226,803 | 44.6% |

| Distribution Per Unit (“DPU”) (cents) | 7.36 | 6.81 | 8.1% |

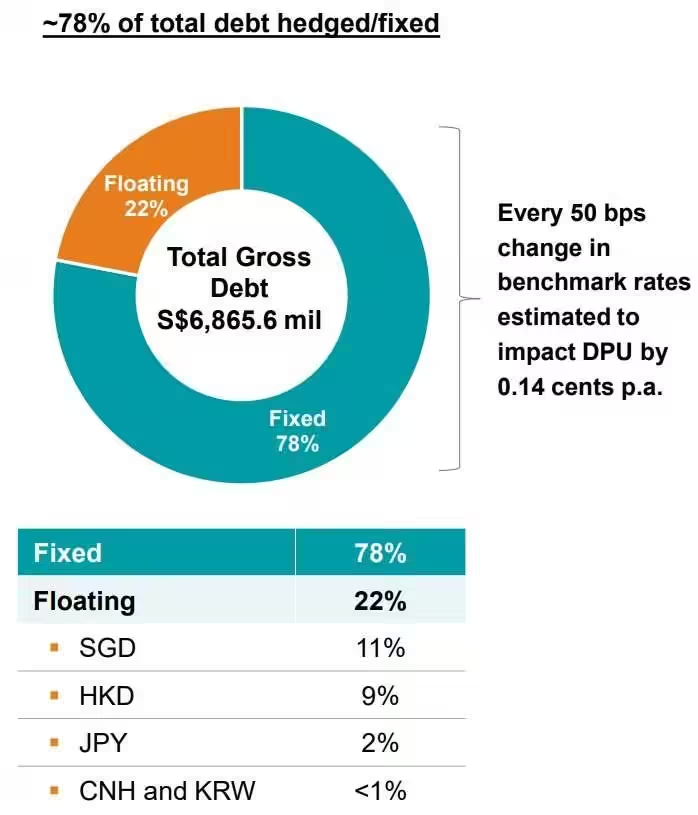

Debt

As of 31st December 2022, gearing ratio stood at 40.2%.

78.3% of its debt is hedged based on fixed rate to mitigate against sudden interest rate hikes.

If you look at the chart below, the debt maturity is well distributed. Average Term to Maturity of Debt stood at 2.8 years.

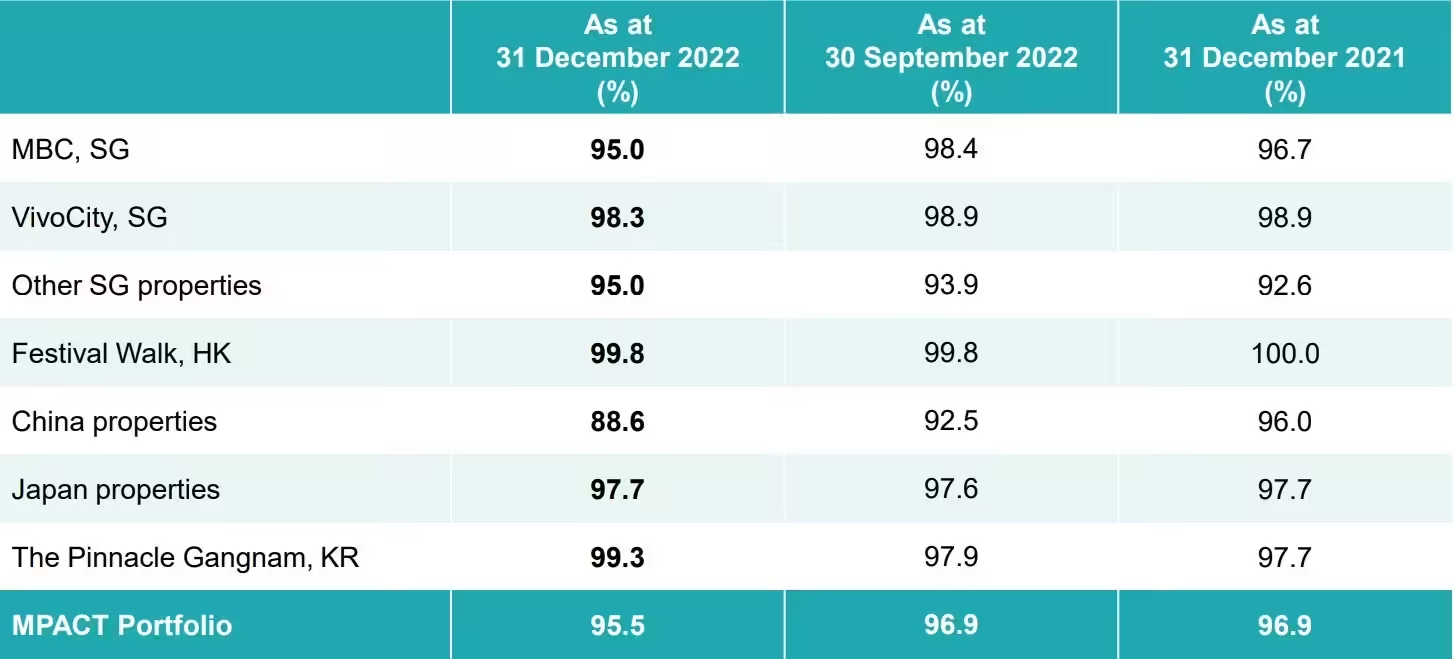

Occupancy

Overall portfolio occupancy stood at 95.5%. The breakdown is shown below.

As you can see, China properties is the lowest among the other properties at 88.6%. However, the manager has shared that they have successfully renewed lease of portfolio’s 2nd largest tenant for 5 years till 2028 despite COVID impact in China. I believe this should inject some form of stability in the occupancy for China properties.

Leases

Rental reversion is negative at -0.3%. MPACT shared that positive rental reversions recorded in all markets except Greater China, which is facing headwinds from prolonged COVID-19 restrictions.

Weighted Average Lease Expiry (“WALE”) stood at 2.6 years and the lease expiries are well staggered.

Current Dividend Yield

Based on the current share price of S$1.71 and FY21/22 distribution of 9.53 cents, this translate to a current dividend yield of 5.57%.

I notice the share price has came down slightly recently. Opportunity?

Summary of MPACT 3Q FY22/23 Financial Results

The positives for MPACT are:

- Higher Gross Revenue and Net Property Income due to contribution from properties acquired through the merger and higher contribution from the Singapore portfolio

- YTD FY22/23 MPACT still managed to achieve a DPU increase of 8.1% y-o-y.

- Attractive current dividend yield of 5.57%

The downside are:

- Higher operating cost erodes revenue

- High gearing ratio of 40.2%

- Negative rental reversion

Given that the share price has fallen recently, do you think it is a crisis or opportunity?