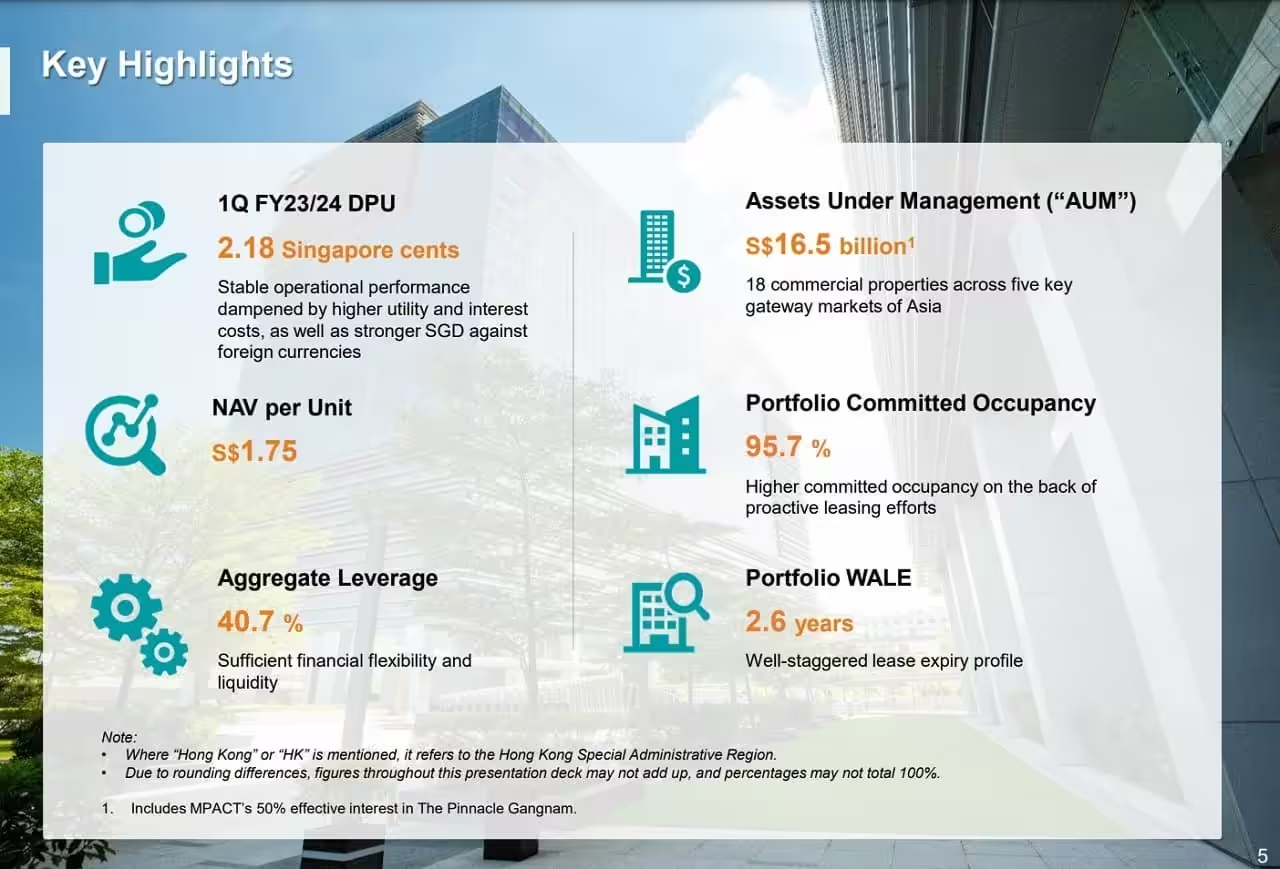

On 31st July 2023, Mapletree Pan Asia Commercial Trust (MPACT) announced its 1QFY23/24 Financial Results. MPACT’s portfolio comprises 18 commercial properties across five key gateway markets of Asia – five in Singapore, one in Hong Kong, two in China, nine in Japan and one in South Korea.

With the merger between Mapletree Commercial Trust and Mapletree North Asia Commercial Trust, how has MPACT fare?

Let us look at its 1QFY23/24 financial results to find out.

MPACT 1QFY23/24 Financial Results

Gross revenue and Net Property Income (“NPI”) for 1Q FY23/24 grew 75.6% and 68.0% on a year-on-year to S$237.1 million and S$179.2 million, respectively.

The gains were attributed to the contribution from overseas properties acquired through the merger, but dampened by stronger Singapore dollar against foreign currencies. There was also higher contribution from the Singapore properties due to their better performance.

The gains were offset by higher property operating expenses mainly due to property operating expenses incurred by the overseas properties acquired

through the merger. Utility costs was also higher.

Net finance costs was higher mainly due to higher interest rates.

Distribution Per Unit was weighed down by full quarter impact of higher utility

costs, effects of higher interest rates and stronger SGD against HKD,

RMB, JPY and KRW.

| 1QFY23/24 (S$’000) |

1QFY22/23 (S$’000) |

Change | |

| Gross Revenue | 237,118 | 134,997 | 75.6% |

| Net Property Income | 179,200 | 106,664 | 68.0% |

| Property expenses – Utility Expenses |

(57,918)

(9,896) |

(28,333)

(2,011) |

104.4%

392.1% |

| Net Finance Costs |

(54,101) | (19,074) | 183.6% |

| Amount Distributable To Unitholders | 114,752 | 83,287 | 37.8% |

| Distribution Per Unit (“DPU”) (cents) | 2.18 | 2.50 | (12.8)% |

Debt

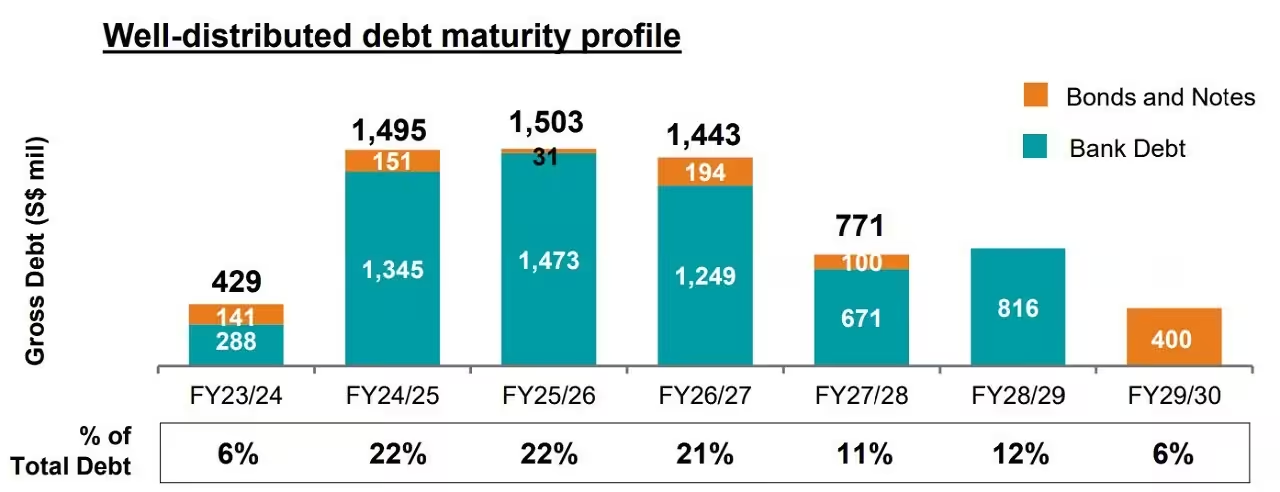

As of 30th June 2023, MPACT’s aggregate leverage stood slightly high at 40.7%.

74.2% of total debt was hedged at fixed interest rates to mitigate against sudden interest rate hikes.

The debt maturity profile remained well-spread with no more than 22% of debt expiring in any financial year.

Occupancy

As of 30th June 2023, MPACT’s committed occupancy stood healthy at 95.7%. MPACT’s retail and office/business park leases was 2.2 years and 2.8 years respectively, translating into an overall portfolio WALE of 2.6 years.

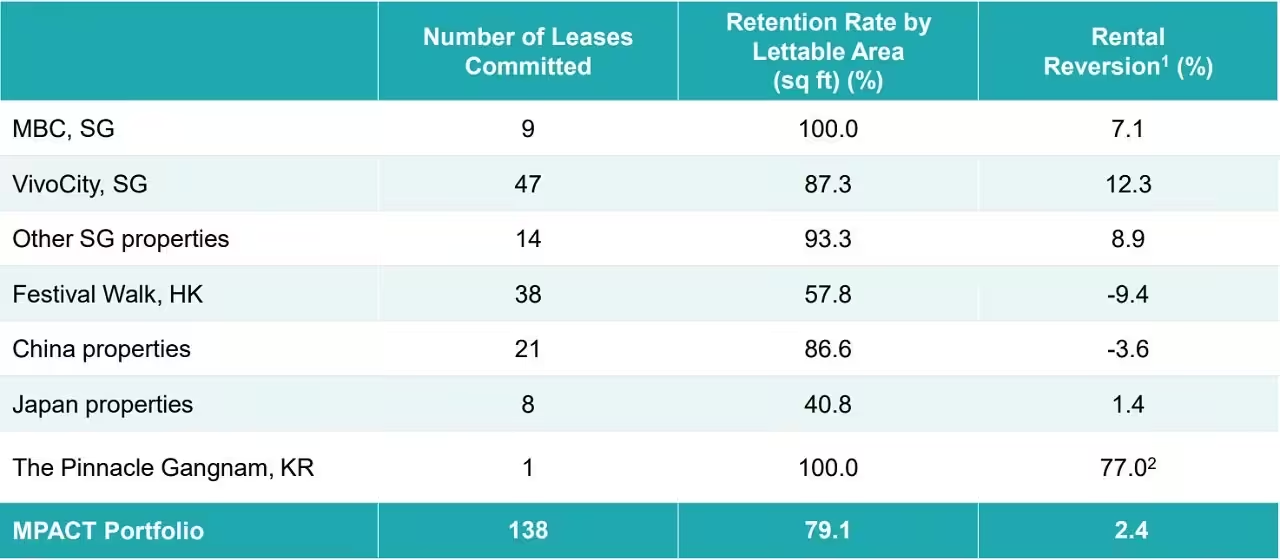

All markets except Greater China recorded positive rental uplifts, contributing to a portfolio rental reversion of 2.4%. In particular, the properties in Singapore achieved strong rental uplifts ranging from 7.1% at Mapletree Business City to 12.3% at VivoCity.

Festival Walk continued to show improvement in rental reversion, signalling ongoing progress towards rental stabilisation.

Current Dividend Yield

Based on MPACT’s current share price of S$1.60 and FY22 full year distribution of 9.61 cents, this translate to a current dividend yield of 6.01%.

Summary of MPACT 1QFY23/24 Financial Results

As usual, let me summarize the pros and cons of MPACT based on its 1QFY23/24 financial results.

The pros are:

- Gross revenue and Net Property Income (“NPI”) grew 75.6% and 68.0% on a year-on-year to S$237.1 million and S$179.2 million, respectively.

- 74.2% of total debt was hedged at fixed interest rates to mitigate against sudden interest rate hikes.

- The debt maturity profile remained well-spread.

- MPACT’s committed occupancy stood healthy at 95.7% which could be higher if not for the drag down by the occupancy of its China assets.

- Portfolio rental reversion of 2.4% with signs of improvement Festival Walk’s rental reversion.

- Current dividend yield of 6.01%.

The cons are:

- Property operating expenses and utility costs were higher.

- Similarly, Net finance costs was higher mainly due to higher interest rates.

- Because of the above factors, Distribution Per Unit was lower at 2.18 cents.

- MPACT’s aggregate leverage is slightly high at 40.7%.

- Festive Walk’s rental reversion is negative 9.4%.

The Hong Kong and China properties were inherited from Mapletree North Asia Commercial Trust as a result of the merger.

From the above, these properties are underperforming. This is probably the reason why shareholders who once held Mapletree Commercial Trust are selling off MPACT.

Even as a shareholder of MPACT, I am disappointed with its performance and hope for the day the manager to divest Festival Walk and its China properties.