On 19th April 2022, Keppel DC REIT has provided their 1Q2022 operational updates. The good news is that Distributable income and Distribution Per Unit (DPU) increased by 5.9% and 0.2% y-o-y respectively. The increase was attributed to recent data centre acquisitions and investment in debt securities.

The bad news is that the gains were partially offset by lower contributions

from Singapore assets as a result of provisions made for a client payment under dispute at Keppel DC Singapore 1 Ltd and higher electricity costs.

Let us look into the details of Keppel DC REIT’s 1Q2022 financial results.

1Q2022 Financial Results

Despite the increase in Distributable income and DPU, Gross revenue actually decreased by 0.9% y-o-y.

Net Property Income also decreased by 1.4% y-o-y. In terms of Net Asset Value (NAV), it only decreased by 0.7% which in my opinion is not much of a great deal.

| 1Q2022 (S$’000) |

1Q2021 (S$’000) |

Change | |

| Gross Revenue | 66,104 | 66,685 | (0.9)% |

| Net Property Income | 60,129 | 60,989 | (1.4)% |

| Net Asset Value (NAV) ($) | 1.33 | 1.34 | (0.7)% |

| Distributable Income | 44,528 | 42,029 | 5.9% |

| Distribution Per Unit (“DPU”) (cents) | 2.466 | 2.462 | 0.2% |

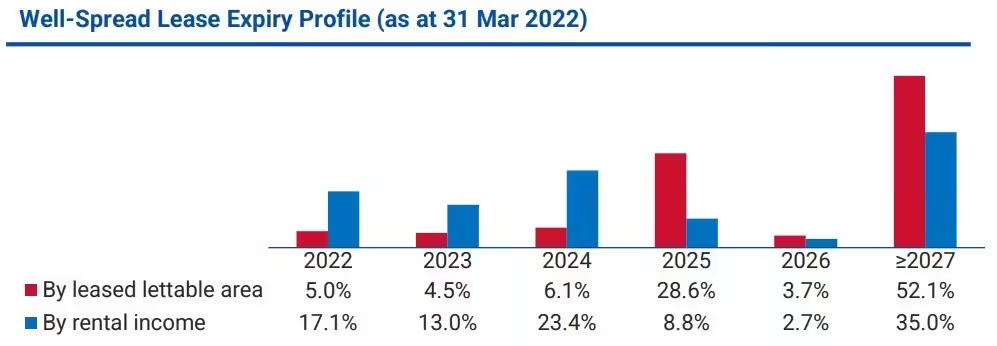

Portfolio Occupancy

Overall portfolio occupancy stood at 98.7% with a long Weighted Average Lease Expiry (WALE) of 7.7 years.

If you look at the lease expiries below, the expiries are well spread till beyond 2027.

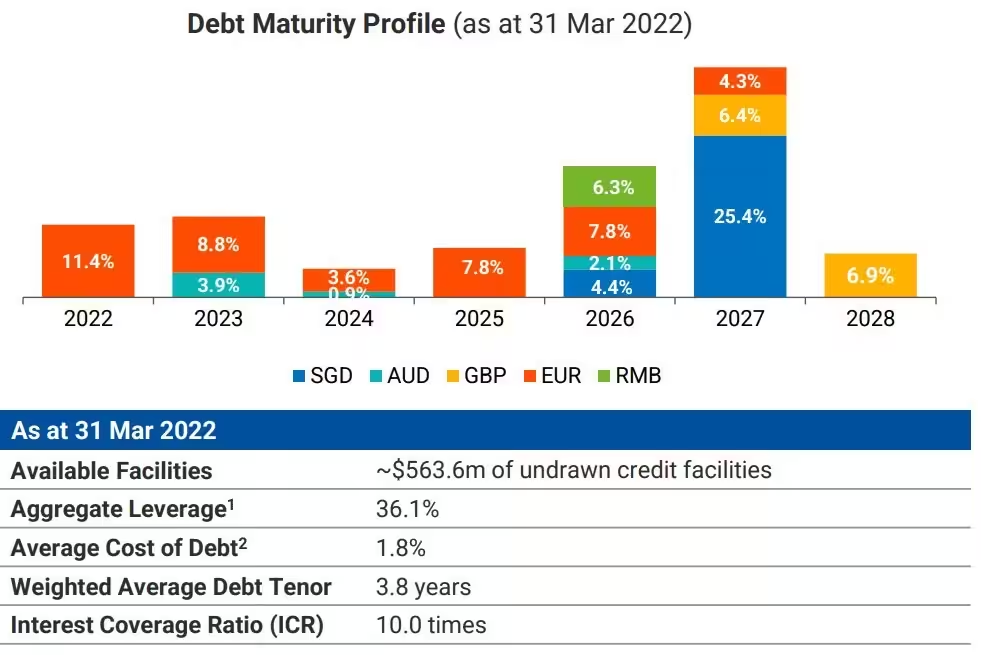

Debt

As of 31st March 2022, the gearing ratio stood at 36.1%. This means there is still plenty of room for more debt to fund future acquisitions.

76% of loans hedged through floating-to-fixed interest rate swaps, with the remaining unhedged borrowings in EUR.

Current Dividend Yield

If you look at the 1 year trend of Keppel DC REIT share price, it is on the downtrend.

Based on FY21 full year DPU of 9.851 cents and current share price of S$2.08, this translate to a current dividend yield of 4.74%.

Summary of Keppel DC REIT 1Q2022 Updates

In my opinion, Keppel DC REIT was once a unique REIT as it was the only one that comprises of pure Data Centres in its portfolio. Riding on the IT boom in cloud technologies and digitalisation, it has performed well over the years.

Nevertheless, good things have to end one day. Other REITs such as Digital Core REIT (SGX:DCRU), Mapletree Industrial (SGX:ME8U) and Ascendas REIT (SGX:A17U) have added data centres to form a hybrid portfolio. This means that investors now have more choices to choose from if they wanted to invest in Data Centres.

In summary, the pros are

- Pure data centre play.

- Acquisitions continue to drive the increase in DPU.

- Current dividend yield getting attractive (nearing 5%)

The cons are

- Higher electricity costs erode into profits.

- Global data centres exposure increased the risks of investing in Keppel DC REIT due to ongoing tensions between Russia, Ukraine, China and the Western countries.