Do you want to know how to get paid daily hassle free? Recently, I found a savings account that pays me daily 2.38% per annum and up to 2.88% without me doing anything. If you think I am talking about the popular Chocolate Finance, then you are wrong. Do not get me wrong. Chocolate Finance is still fantastic because it pays 3.3% per annum on your first 20K which is higher than the savings account I am going to tell you about. However, my concern with Chocolate Finance is that your deposits are not covered by Singapore Deposit Insurance Corporation (SDIC) because Chocolate Finance is not a bank.

What is Singapore Deposit Insurance Corporation (SDIC)? The Singapore Deposit Insurance Corporation (SDIC) is a statutory board under the Ministry of Finance in Singapore. Its main purpose is to provide deposit insurance for depositors in Singapore. This means that in the event of a bank failure, depositors will be protected up to a certain limit by the SDIC.

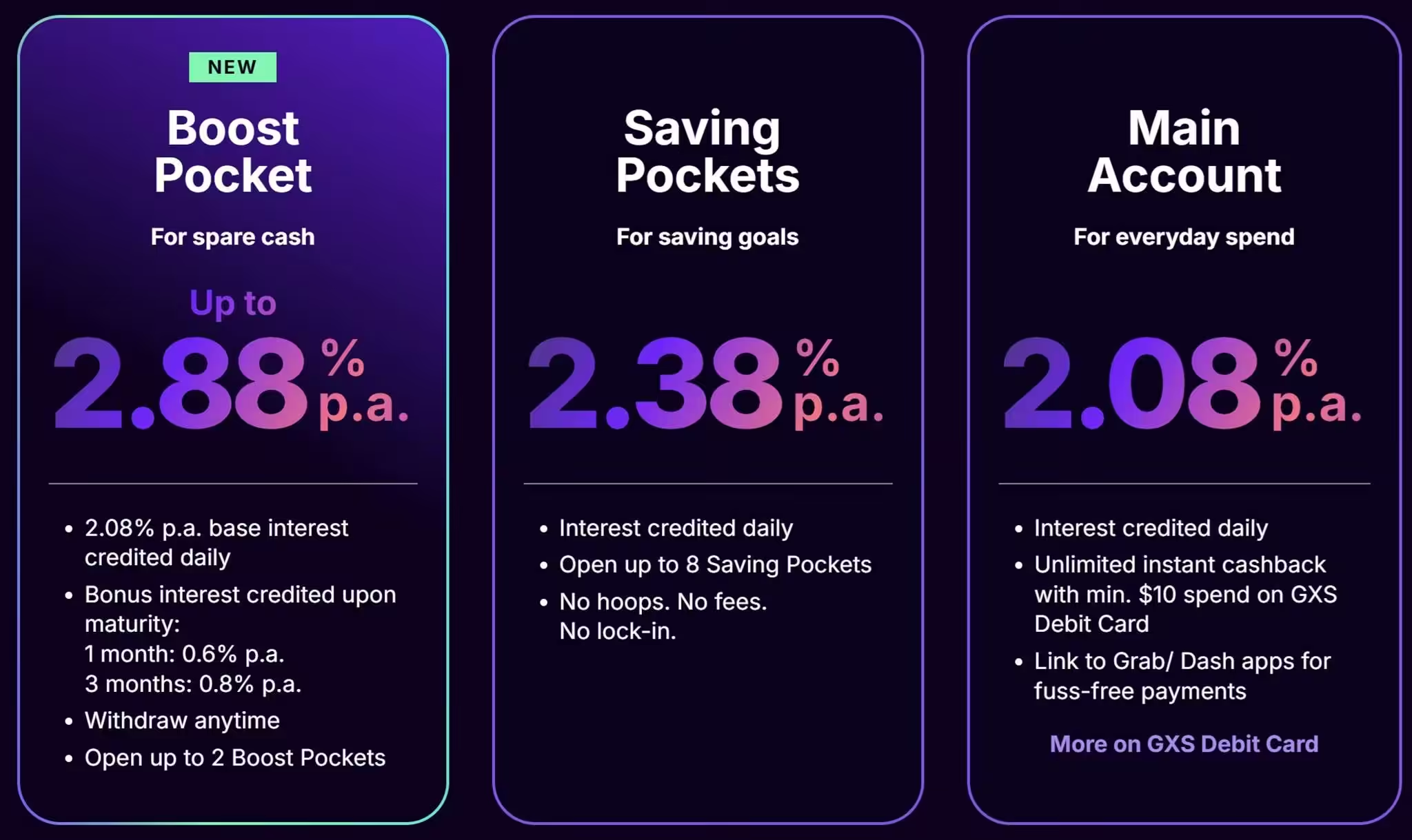

If you are a low-risk taker, the savings account that I found is covered by Singapore Deposit Insurance Corporation (SDIC) for up to S$100,000 per depositor per Scheme member by law. For your savings, you are paid 2.38% daily. Interest earned are credited daily.

To earn higher interests, you can also lock in your cash for 1 month or 3 months to earn the bonus interest of 0.6% per annum and 0.8% per annum respectively. In short, you earn 2.68% per annum for a 1-month placement and 2.88% per annum for a 3-months placement. If you compare this with the best fixed deposit rates in February 2025, CIMB Bank is only giving you 2.70% per annum for a 3-month fixed deposit placement.

Alright, let me reveal and introduce you to GXS Bank. GXS Bank is a digital bank, and it holds a banking licence issued by the Monetary Authority of Singapore. GSX Digital Bank is backed by a consortium consisting of Grab Holdings Inc. – Southeast Asia’s leading super app, and Singtel – Asia’s leading communications technology group.

GSX Digital Bank uses the concept of pockets. You can create up to 8 Saving Pockets and 2 Boost Pockets. The main account pays an interest rate of only 2.08% per annum. The current maximum balance allowed for GSX Savings Account is S$75,000. This means you cannot transfer funds into your GXS Savings Account once it reached the maximum.

For higher interests, I suggest creating Saving Pockets to earn 2.38% per annum because you can close these pockets anytime. If you have a lump sum, then I suggest creating a Boost Pocket to take advantage of the higher interest of 2.88% per annum. For all accounts, interests are credited daily. For Boost Pocket, the bonus interest is only credited upon maturity. This is how to get paid daily without doing anything!

At this point of writing, I have created three Saving Pockets. On a monthly basis, I plan to transfer money into the Supplementary Retirement Scheme (SRS) Saving Pocket. In November, I shall close this pocket and transfer them into my SRS account to maximize the tax relief for this year.

The second Saving Pocket will be twenty percent of my monthly salary. When I receive my monthly wage, I will transfer twenty percent into this pocket. This helps to build up my cash on hand where I can use it when I need them in future.

The third Saving Pocket will be the dividends from the REITs that I have in my stock portfolio. These are passive income and putting them into the saving pocket help me to compound the return further.

Last, I just want to share that this is not a sponsored post and solely based on my own research and opinion. There are no affiliate links in this post. With falling interest rates, I believe everyone like me is looking for the best place to park your idle money to earn extra cash. If you like this post, do check out GSX Digital Bank at GXS Savings Account | Earn 2.88% p.a. with Boost Pocket.

just curious. Why don’t you choose USD money Market fund? nowadays is pays 4%+. I think that’s quite safe right?

There is still low risk involved in a money market fund. Do look up the allocation on where your money is placed under the fund factsheet.