Frasers Logistics and Commercial Trust has announced their FY21 full year results on 11th November 2021. The financial results are simply solid!

The REIT has achieved a year-on-year growth in DPU of 7.9%. Net Asset Value (“NAV”) also increased 12.7% from S$1.10 to S$1.24.

Frasers Logistics and Commercial Trust FY21 Full Year Results

In 2H2021, gross revenue and adjusted net property income was higher due to the acquisitions undertaken in FY2020 and the 2021.

A Distribution Per Unit (“DPU”) of 3.88 Singapore cents was declared in 2H2021 which is 6.3% higher than 2H2020.

| 2H2021 (S$’000) |

2H2020 (S$’000) |

Change | |

| Gross Revenue | 237,627 | 213,284 | 11.4% |

| Net Property Income | 181,271 | 161,355 | 12.3% |

| Distributable Income | 139,649 | 124,863 | 11.8% |

| Distribution Per Unit (“DPU”) (Singapore cents) | 3.88 | 3.65 | 6.3% |

The DPU for the full year FY2021 stood at 7.68 Singapore cents which is 7.9% higher than FY2020.

| FY2021 (S$’000) |

FY2020 (S$’000) |

Change | |

| Gross Revenue | 469,328 | 332,029 | 41.4% |

| Net Property Income | 355,161 | 258,335 | 37.5% |

| Distributable Income | 270,075 | 201,080 | 34.3% |

| Distribution Per Unit (“DPU”) (Singapore cents) | 7.68 | 7.12 | 7.9% |

Debt

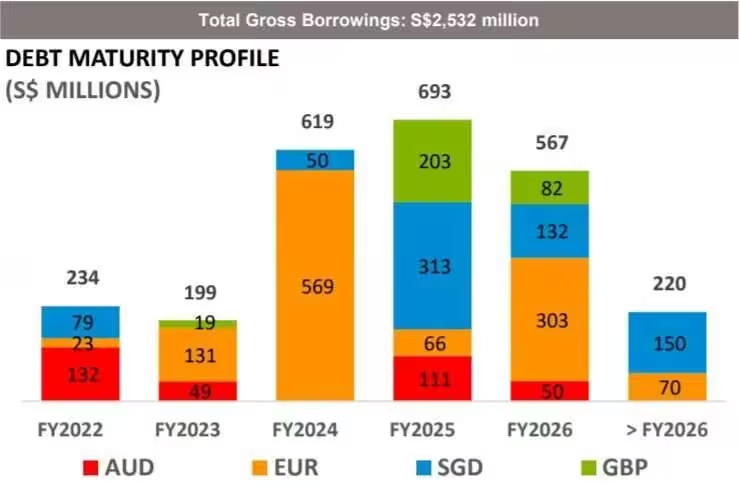

Gearing ratio stood at 33.7%. Average weighted debt maturity improved by 0.3 years to 3.4 years, with the 7-year notes issuance in July 2021 and new financings entered into in FY2021.

Frasers Logistics and Commercial Trust has a credit rating (S&P) of BBB+ / Stable.

Occupancy

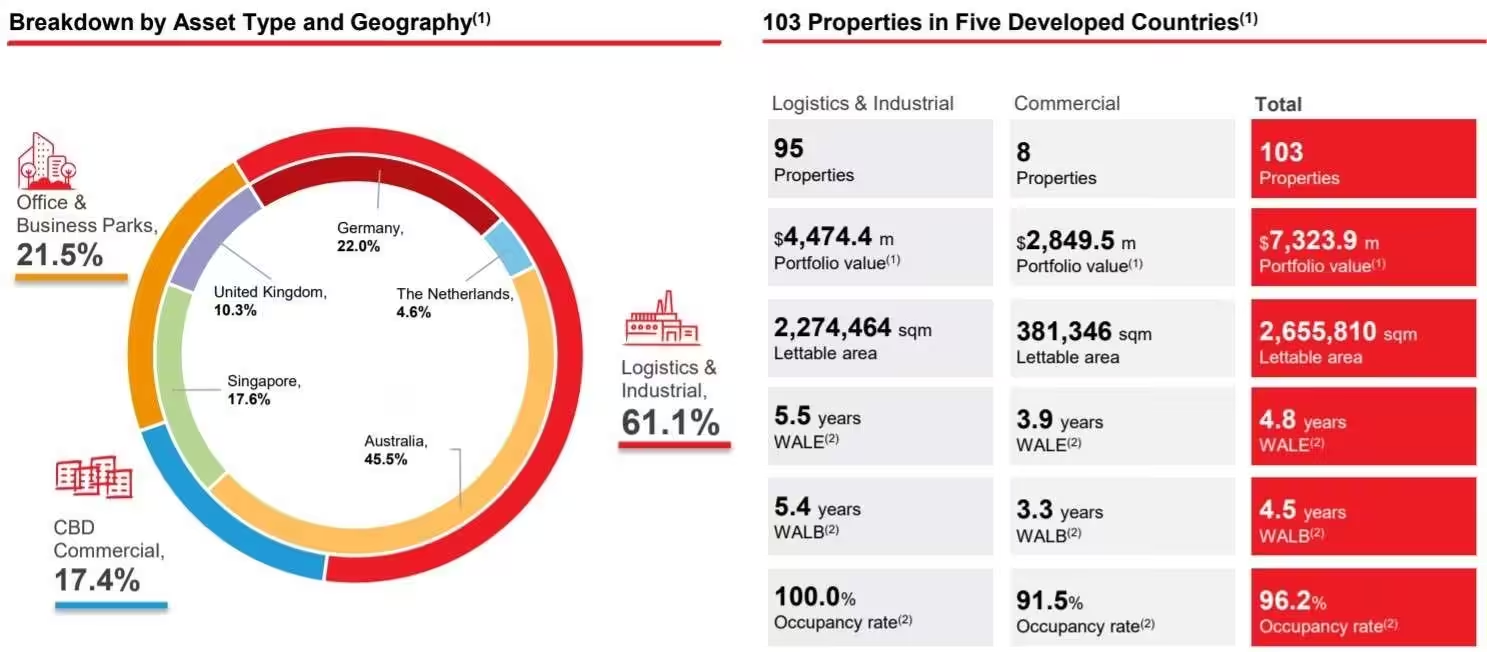

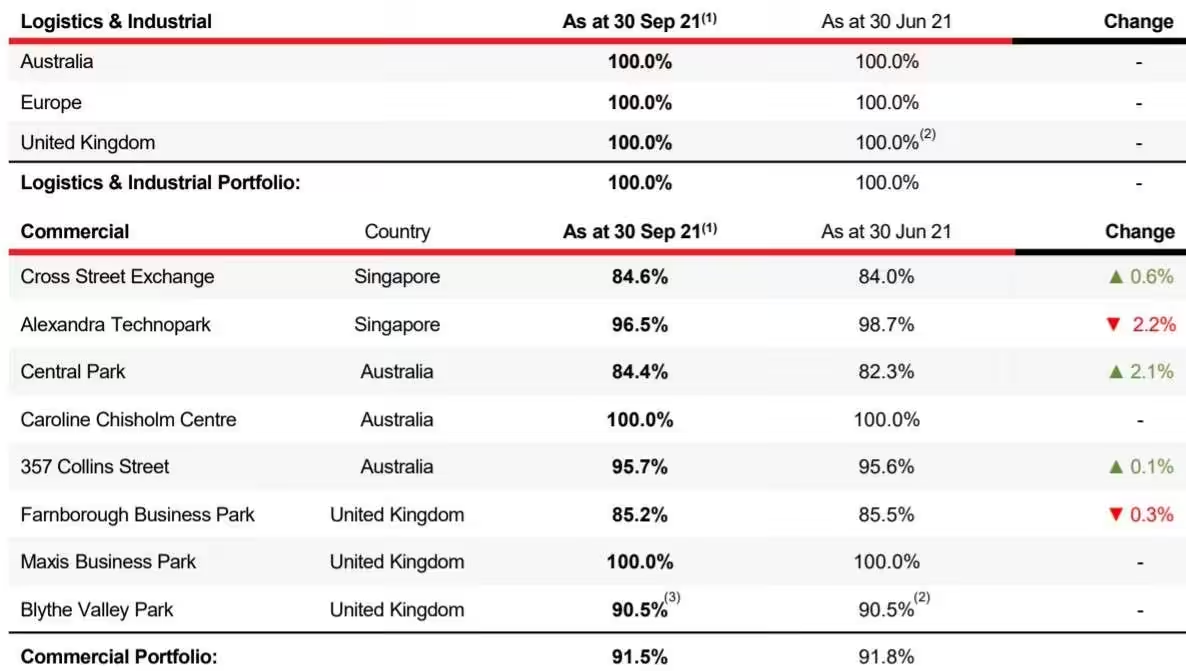

Overall portfolio occupancy stood at 96.2%. The occupancy for the Logistics & Industrial Portfolio and Commercial Portfolio stood healthy at 100% and 91.5% respectively.

Current Dividend Yield

As you can see below, Frasers Logistics and Commercial Trust has been paying dividends consistently year-on-year. In fact, DPU increased year-on-year.

Based on the current share price of S$1.51 and FY2021 full year payout of 7.68 Singapore cents, this translate to a current dividend yield of 5.09%.

Summary of Frasers Logistics and Commercial Trust FY21 Full Year Results

In my opinion, this is one solid REIT to invest in for the following reasons.

- Healthy occupancy.

- Low gearing ratio of 33.7% which means there is room for more debt for further acquisitions.

- DPU increase year-on-year.

Having said that, here are some considerations.

- Low current dividend yield at 5.09%. Patient investors can wait for the share price to come down so that current dividend yield will go up.