Today, Frasers Logistics and Commercial Trust has released their 2HFY22 Financial Results. The 2HFY22 and Full Year FY22 results are in a sea of red.

What happen? Let us take a look in details on why Gross Revenue and Distribution Per Unit (DPU) has fallen.

Frasers Logistics and Commercial Trust 2HFY22 Financial Results

| 2HFY22 (S$’000) |

2HFY21 (S$’000) |

Change | |

| Gross Revenue | 214,517 | 237,627 | (9.7%) |

| Net Property Income | 162,053 | 181,271 | (10.6%) |

| Finance Cost |

(19,303) | (22,271) | 13.3% |

| Amount Distributable To Unitholders | 139,645 | 139,649 | 0.0% |

| Distribution Per Unit (“DPU”) (cents) | 3.77 | 3.88 | (2.8%) |

Frasers Logistics and Commercial Trust Full Year FY22 Financial Results

Similar to the above reasons for 2HFY22, Gross Revenue and Net Property Income for the full year declined 4.1% and 3.7% respectively.

Distribution Per Unit (DPU) was 0.8% lower at 7.62 cents.

| FY22 (S$’000) |

FY21 (S$’000) |

Change | |

| Gross Revenue | 450,187 | 469,328 | (4.1%) |

| Net Property Income | 342,138 | 355,161 | (3.7%) |

| Finance Cost |

(41,595) | (45,687) | 9.0% |

| Amount Distributable To Unitholders | 281,753 | 270,075 | 4.3% |

| Distribution Per Unit (“DPU”) (cents) | 7.62 | 7.68 | (0.8%) |

Debt

Gearing stood at 27.4% with Average Weighted Debt Maturity standing at 2.7 years. In my opinion, the gearing is at pretty low level. I believe the low gearing is because the manager has repaid S$504.9 million of borrowings with the net divestment proceeds from Cross Street Exchange.

81.7% of the debt is hedged at fixed rates to further mitigate against interest rate hikes.

As you can see below, Frasers Logistics and Commercial Trust has a well spread debt maturity profile and the manager shared that they have sufficient internal funds and facilities to refinance or repay the debt maturing in FY2023.

The manager shared that for every potential 50 bps increase in interest rates on variable rate borrowings is estimated to impact DPU by 0.05 Singapore cents.

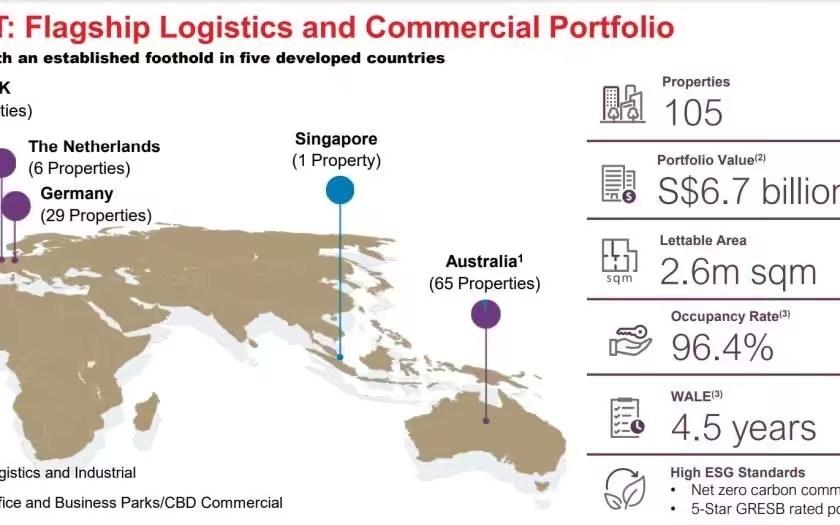

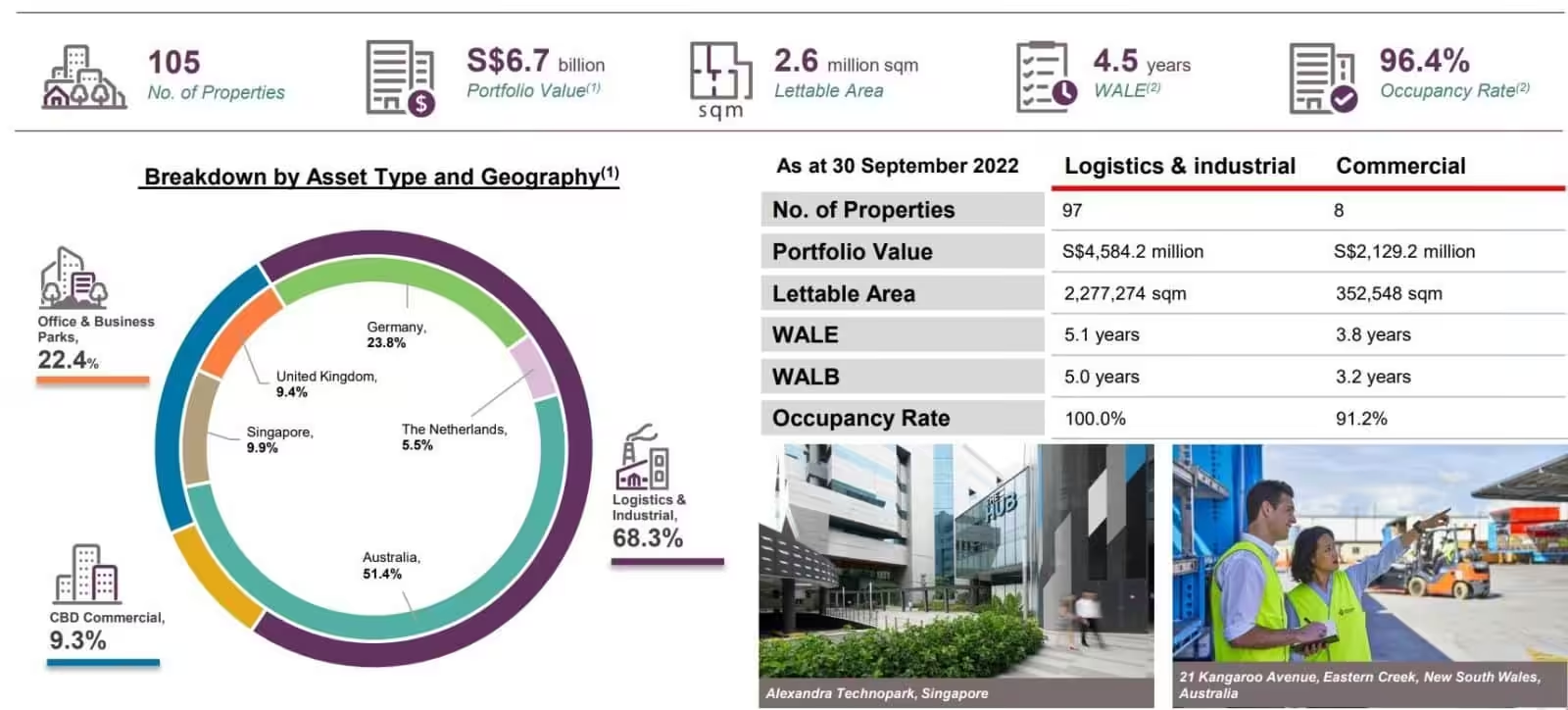

Occupancy

Overall portfolio occupancy stood at 96.4%. The occupancy for the Logistics and Industrial segment stood at 100% while the occupancy rate for Commercial stood at 91.2%.

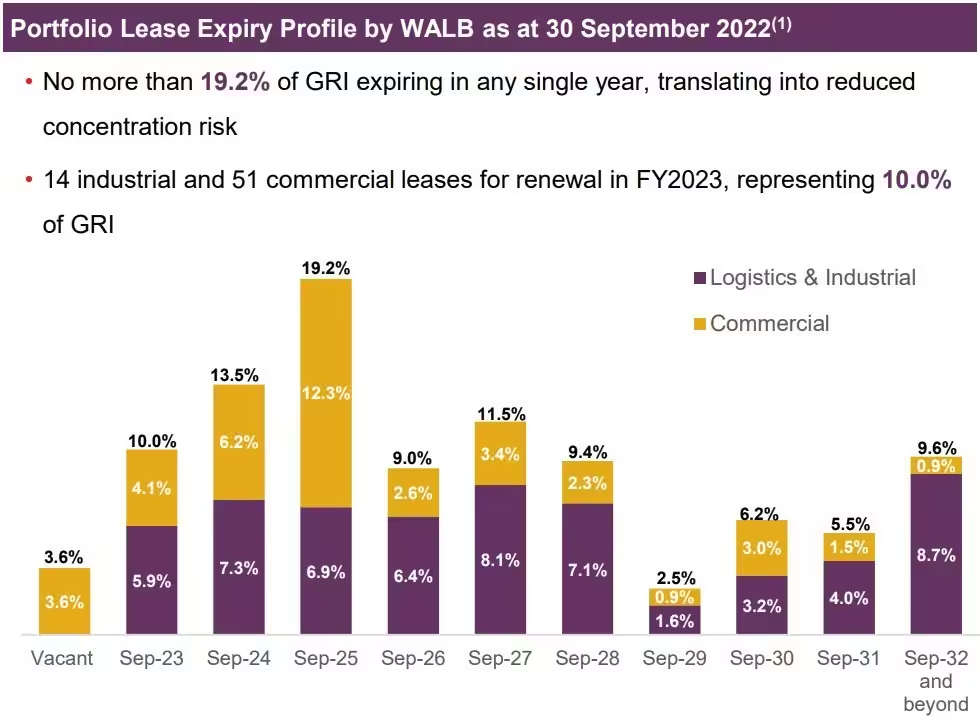

Lease Expiry Profile

The lease expiry is also well-spread with no more than 19.2% of Gross Rental Income expiring in any single year, reducing concentration risk.

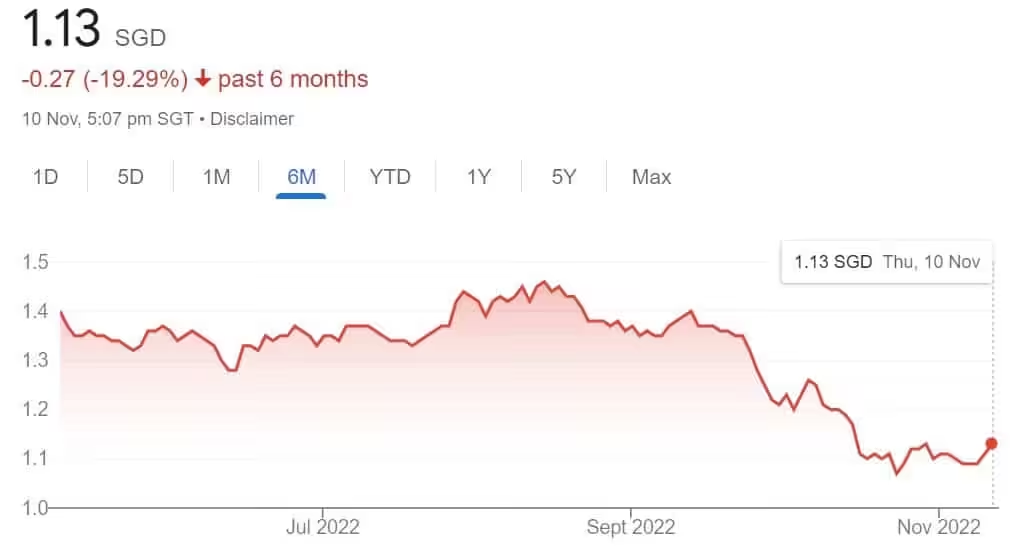

Current Dividend Yield

Based on the share price of S$1.13 and FY22 full year DPU of 7.62 cents, this translate to a current dividend yield of 6.74%.

Summary of Frasers Logistics and Commercial Trust 2HFY22 Financial Results

The Distribution Per Unit (DPU) has been disappointing given that Frasers Logistics and Commercial Trust has a AUM of S$6.7billion. I lament this on the weaker exchange rates which resulted in lower DPU paid in Singapore cents.

As you can see below, Frasers Logistics and Commercial Trust has a track record in value creation and this is the first time I have seen its financial results in a sea of red.

The impact of the COVID-19 pandemic, which has plagued the world for over two years, together with disruptions from the Russia-Ukraine conflict, has continued to hamper economic growth. Rising energy costs, high levels of inflation and the consequential interest rate hikes, together with supply chain issues formed some of the biggest global challenges, exacerbating the risk of a global recession.

All the above reasons are why logistics and commercial REITs are currently being hit by this setback. However, if we bear in mind that such situations will not last forever, the current price of S$1.13 is probably a good level to jump onto this REIT given the attractive 6.74% current dividend yield. Given its track record, I am sure Frasers Logistics and Commercial Trust will be able to grow its DPU when all these global tensions are over.