First REIT is going to restructure Master Lease Agreements of its Indonesian Hospital Assets. Earlier this year in June 2020, I wrote about the opportunity to buy into First REIT given the high attractive yield of 11.62%.

However, with such a high yield, there can be potentially high risks involved such as the debt profile of its sponsor Lippo Karawaci. The sponsor’s escalating debt caused First REIT’s share price to fell in 2018.

On 1 June 2020, PT Lippo Karawaci Tbk (“LPKR”) unilaterally announced its intention to restructure all of the Master Lease Agreements which LPKR had entered into with First REIT for the LPKR Hospitals (the “LPKR MLAs”). Subsequently in September 2020, the Manager of First REIT received a non-binding rental restructuring proposal from LPKR.

As you can see from the chart below, the share price of First REIT went on a downtrend.

Rationale For First REIT Restructure Master Lease Agreements

The sponsor LPKR is facing severe liquidity pressure due to its significant recurring expenses, weak operating cash flows and its inability to divest assets. This is worsened by the impact of the Covid-19 pandemic on LPKR’s business which has further weakened its operating performance in the medium term. LPKR’s dire liquidity position has been confirmed by rating agencies in their most recent reports and credit ratings.

The situation is exacerbated by the depreciation of the Indonesian Rupiah against the Singapore Dollar by approximately 44.8% since the IPO of First REIT which adds further pressure on LPKR as rent payments under the existing LPKR MLAs have to be made in Singapore Dollars.

The Manager understands that without the Proposed LPKR MLA Restructuring, there

is a real risk and high probability that LPKR would default under the existing LPKR MLAs.

If LPKR defaults, What Will Happen?

Should LPKR default, this will

- Result in an immediate loss of approximately 72.1% of First REIT’s rental income for the financial year ended 30 December 2019 (“FY2019”).

- Cause breaches in First REIT’s debt covenants.

- Impair First REIT’s ability to execute any refinancing and meet its repayment obligations, in particular the S$196.6 million debt coming due in March 2021.

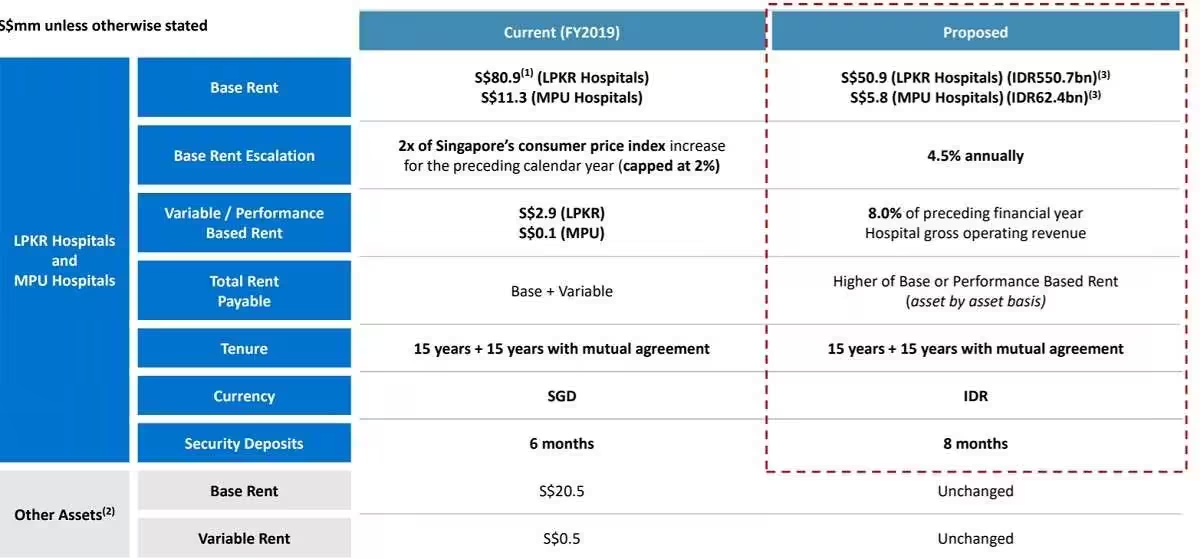

Restructuring #1 – Proposed Rent Structure

Under the new proposed rent structure, this will result in higher fixed escalation rate which is 4.5% per annum as compared to the current step-up mechanism which is two times the Singapore consumer price index subject to a cap of 2.0%.

Buffer against depreciation is baked in which is approximately 2.45% in 2022 and 40.35% in 2035 when compared against the growth in the base rent of First REIT under the LPKR MLAs using the existing base rent formula assuming maximum growth at 2.0% per annum.

Restructuring #2 – Revised Performance Based Rent Structure

Revised performance based rent structure will replace the existing variable rent structure, which has contributed not more than 4.2% and 0.7% to the total rent received for each year over the past three years under the existing LPKR MLAs and MPU MLAs respectively, and provides improved upside sharing for First REIT.

Restructuring #3 – Increased WALE

WALE for First REIT will be extended from 7.4 years as at 31 December 2019 to 12.6 years, which provides a more certain and stable lease profile to reposition First REIT for future growth.

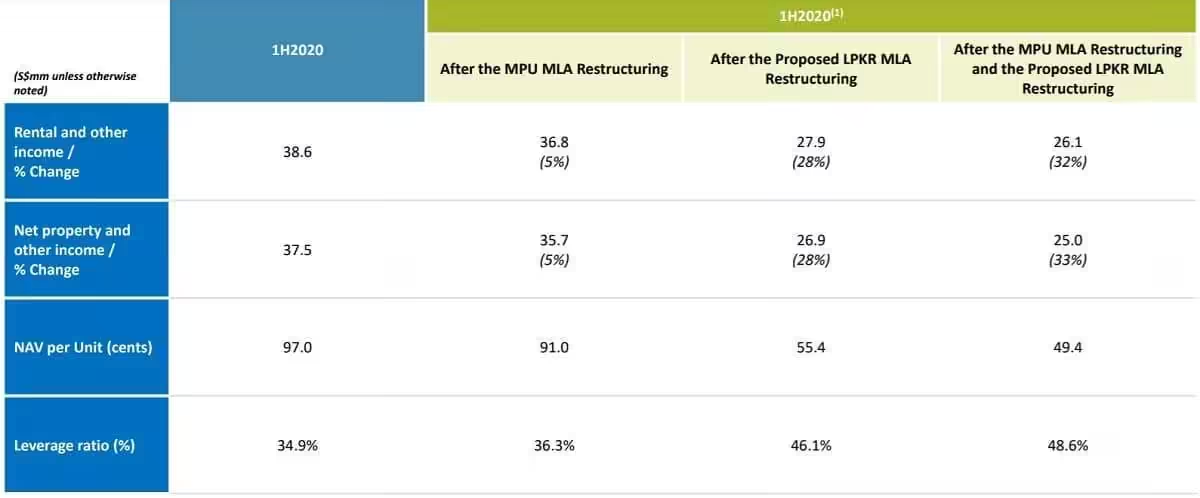

What Does it Mean for Shareholders?

From what I can see, this means a lower NAV after restructuring. Gearing ratio has also increased significantly. Valuation for its assets will also fall.

Summary

In my opinion, the restructuring is necessary to avoid the collapse of First REIT. In the short term, existing shareholders have to bear the pain of falling share price, NAV and high gearing ratio. All these can destroy investors confidence in First REIT.

If you divest First REIT now, you will suffer from a loss if you have bought at a higher price. Existing shareholders should bet on the positive outcomes of this restructuring which may bring the REIT back to stability.

Keep calm and collect dividends!