I believe many of you have heard of First REIT. Recently, one of my readers asked me about First REIT. I have not looked into the details of First REIT but I do know that it is a healthcare REIT. Investing into the healthcare industry is considered low risk by many because healthcare services are something that everyone needs no matter the economy is good or bad. Now, let us look into First REIT and whether it is worth investing.

First REIT is Singapore’s first healthcare real estate investment trust that was listed on Singapore Exchange Securities Trading Limited (“SGX”) on 11th December 2006.

Portfolio

First REIT has a total of 20 assets in three countries which are Indonesia, Singapore and South Korea. They have 16 assets in Indonesia alone. I was quite amazed by the number of assets they have in Indonesia. First REIT have 3 assets in Singapore and 1 asset in South Korea.

Indonesia (16 assets)

- Siloam Hospitals Buton & Lippo Plaza Buton

- Siloam Hospitals Kupang & Lippo Plaza Kupang

- Siloam Hospitals Manado & Hotel Aryaduta Manado

- Siloam Hospitals Yogyakarta

- Siloam Hospitals Labuan Bajo

- Siloam Sriwijaya

- Siloam Hospitals Purwakarta

- Siloam Hospitals Bali

- Siloam Hospitals TB Simatupang

- Siloam Hospitals Makassar

- Mochtar Riady Comprehensive Cancer Centre

- Siloam Hospitals Lippo Cikarang

- Siloam Hospitals Lippo Village

- Siloam Hospitals Kebon Jeruk

- Siloam Hospitals Surabaya

- Imperial Aryaduta Hotel & Country Club

Singapore (3 assets)

- Pacific Healthcare Nursing Home @ Bukit Merah

- Pacific Healthcare Nursing Home II @ Bukit Panjang

- The Lentor Residence

South Korea (1 asset)

- Sarang Hospital

Occupancy

Occupancy stood at 100% with no leases expiring in 2020. There are only 5 assets expiring in 2021. As we can see below, most of the leases are long leases which is a good thing if you enjoy stability but of course, long leases means less growth since you cannot step up the rent until the lease expires.

Financial Summary

First REIT had released their 4Q2019 financial results on 29th January 2020. Gross revenue declined by 1.6% and Net Property Income (“NPI”) declined by 0.8%. However, First REIT has maintained their Distribution Per Unit (“DPU”) payout of 2.15 cents.

| 4Q2019 (S$‘000) |

4Q2018 (S$‘000) |

Change | |

| Gross Revenue | 28,860 | 29,321 | (1.6)% |

| Net Property Income | 28,304 | 28,530 | (0.8)% |

| Distributable Income | 17,169 | 17,014 | 0.9% |

| Distribution Per Unit (“DPU”) (S$ cents) | 2.15 | 2.15 | – |

Let us look at the full year 2019 versus 2018 financial results. Gross revenue and Net Property Income (“NPI”) declined by 0.8% and 1.3% respectively. There is no growth in the Annualized Distribution Per Unit which remains flat at 8.60 cents.

| 2019 (S$‘000) |

2018 (S$‘000) |

Change | |

| Gross Revenue | 115,297 | 116,198 | (0.8)% |

| Net Property Income | 112,894 | 114,391 | (1.3)% |

| Distributable Income | 68,463 | 67,681 | 1.2% |

| Annualized Distribution Per Unit (“DPU”) (S$ cents) | 8.60 | 8.60 | – |

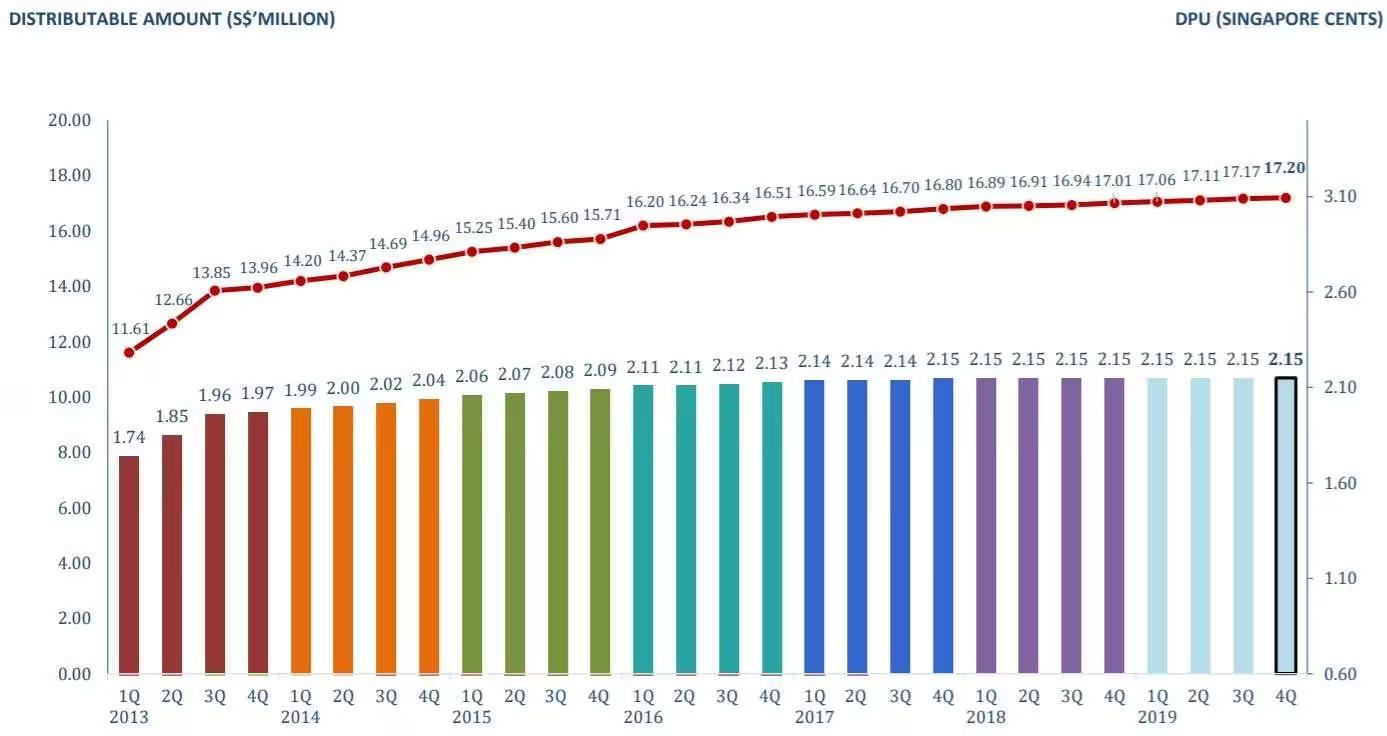

Distribution History

If you are looking at growth in DPU, it is slightly disappointing to see the DPU flat at 2.15 cents since 2018 but on the positive note, First REIT has been consistently paying out and maintaining their DPU. You get 8.60 cents per financial year.

Debt

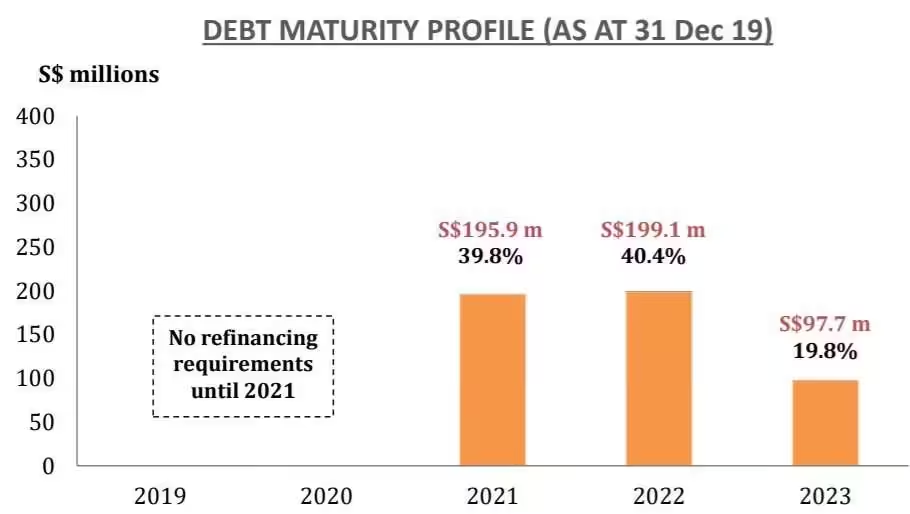

The gearing ratio as of 31st December 2019 stood at 34.5%. The weighted average debt maturity is at 2.01 years. As you can see below, they have no refinancing requirements until 2021 which is a good thing.

Management

Bowsprit Capital Corporation Limited is the manager of First REIT. Mr Tan Kok Mian Victor is the Chief Executive Officer since 2017. Mr Victor Tan was formerly the chief financial officer of Bowsprit, and joined the company in 2008. As the chief financial officer, he oversees the financial operations and managing the financial risks of the trust. I will say First REIT is in good hands since Mr Tan has been with First REIT since 2008.

The troubling part of First REIT is actually with its sponsor. Originally, First REIT have only a single sponsor, Lippo Karawaci. In 2018, Lippo Karawaci ran into debt problems and thus sold 100% stake in Bowsprit Capital to OUE Limited (“OUE”) and OUE Lippo Healthcare (“OUELH”) and 10.63% of the total unitholdings of First REIT to OUE Lippo Healthcare (“OUELH”). In January 2020, Lippo Karawaci raised $325m from successful bond issuance, which will be used to pay off most of the company’s debts due in 2022.

The above explains why First REIT have two sponsors. I am not sure if it is a blessing in disguise, but First REIT benefited from the two sponsor’s healthy pipelines:

- Right-of-First-Refusal (ROFR) to Lippo Karawaci’s properties in Indonesia.

- Right-of-First-Refusal (ROFR) from OUE Lippo Healthcare and opportunities to tap on OUE Lippo Healthcare’s growing healthcare network.

Current Valuation

I am using 6 months chart so that you can see the price crash due to COVID-19.

Based on the current share price of S$0.74 and historical DPU payout of 8.60 cents, this translate to a super attractive dividend yield of 11.62%.

Based on the current share price of S$0.74 and historical DPU payout of 8.60 cents, this translate to a super attractive dividend yield of 11.62%.

However, the COVID-19 situation has caused the temporary closure of

- Lippo Plaza Kupang (“LPK”) (which is part of the Kupang property comprising Siloam

Hospitals Kupang & Lippo Plaza Kupang); and - Lippo Plaza Buton (“LPB”) (which is part of the Buton property comprising Siloam

Hospitals Buton & Lippo Plaza Buton)

From the manager

The temporary closures affect only retail assets which comprise a small proportion of assets within First REIT’s portfolio, which is predominantly healthcare and/or healthcare related. As the situation remains uncertain, it is currently difficult for the Manager to ascertain the full financial impact of the outbreak on the financial performance of First REIT. Nevertheless, First REIT remains in compliance of its debt financial covenants and has adequate financial reserves to fulfil its obligations in the foreseeable future. The Manager will continue to monitor the situation closely across Indonesia, Singapore and South Korea, and will provide updates on any material developments as soon as practicable.

Summary

The current COVID-19 situation seems like a good opportunity to buy into First REIT as this gives you an attractive dividend yield of 11.62%. Like what the manager said, the assets are mainly predominantly in healthcare and/or healthcare related but it is difficult to ascertain the full financial impact of the COVID-19 outbreak on the financial performance of First REIT.

Investors should continue to monitor First REIT sponsor Lippo Karawaci’s debt profile even though $325m was raised to pay off due debts. We have seen how the sponsor’s escalating debt caused First REIT’s share price to fall in 2018.

Taking note of the current attractive dividend yield but unknown financial impact to First REIT, it is good to use the strategy of buying into First REIT in tranches until there is more clarity on the COVID-19 impact to healthcare REITs.

Do not forget if the sponsor gets hit by COVID-19, so will the REIT itself!

Hi

What about exchange rate risk?

Thanks

Hi Lkenggee, yes that is one of the risks as well. From what was shared with me by fellow financial friends, the exchange rate risks comes in during lease renewal where lease rental may be pegged to a lower rate (IDX/SGD) which may affect 5% of the income.