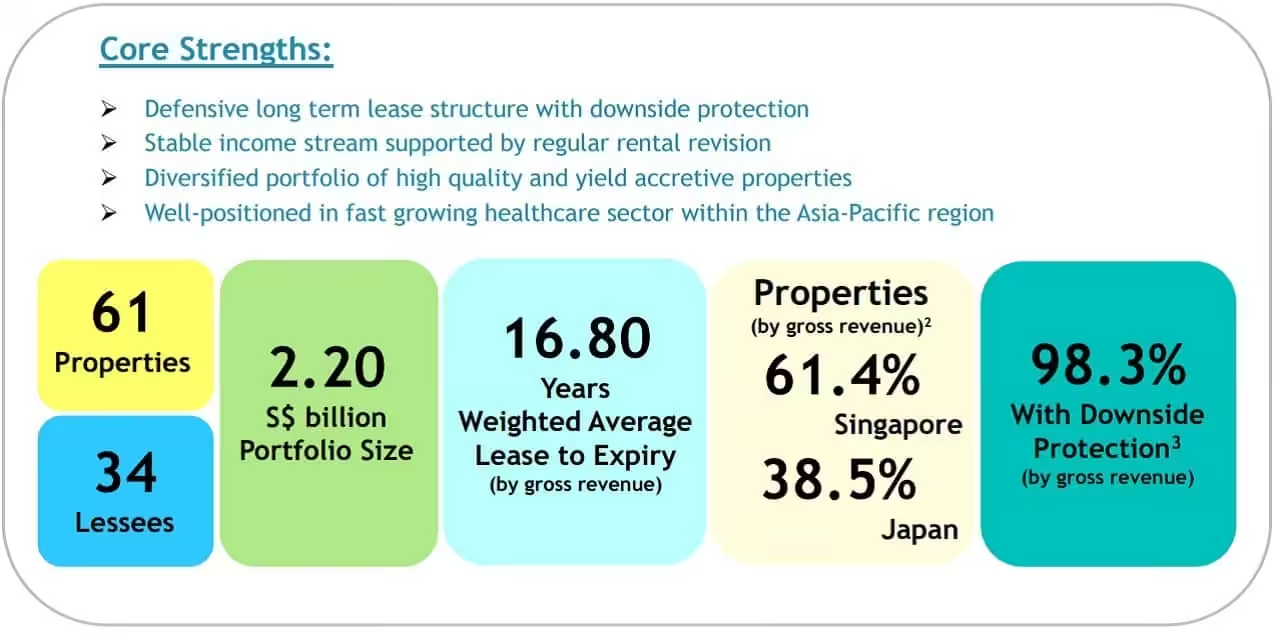

Today, ParkwayLife REIT shared their 1Q2023 business update. If you are not familiar with ParkwayLife REIT, it is one of the largest listed healthcare REITs in Asia with an enlarged portfolio of S$2.20 billion. The REIT have a track record of growing its Distribution Per Unit (DPU) year on year.

As of 31st March 2023, ParkwayLife REIT has 61 properties, 34 lessees across Singapore, Japan and Malaysia. Currently, ParkwayLife REIT makes up 7.13% of my stock portfolio. I have not been able to increase my position because the share price has been mostly on the uptrend.

In this business update, I shall be looking at ParkwayLife REIT’s overall performance and the current dividend yield.

Let us get started.

ParkwayLife REIT 1Q2023 Financial Performance

In 1Q2023, gross revenue increased 21.7% to S$37.3 million as compared to 1Q2022. The increase was attributed to higher rent from the Singapore hospitals due to straight-lining of rental income over the lease term. There is also additional revenue from the properties acquired in 2022. The higher rent was partially offset by the depreciation of the Japanese Yen.

In line with the increase in gross revenue, Net Property Income (NPI) also increased by 23.5% in 1Q2023 as compared to 1Q2022.

| (S$’000) | 1Q 2023 | 1Q 2022 | % Change |

| Gross Revenue | 37,335 | 30,675 | 21.7 |

| Net Property Income | 35,275 | 28,552 | 23.5 |

| Amount available for distribution |

22,075 | 21,534 | 2.5 |

| Distribution per unit (DPU) | 3.65 cents | 3.56 cents | 2.5 |

The best part of this business update is the increase in Distribution Per Unit (DPU) by 2.5% to 3.65 cents. As ParkwayLife REIT makes distribution on a semi annual basis, there is no distribution for 1Q2023.

The Distribution Per Unit (DPU) of 3.65 cents will form part of the 1H2023 distribution when the REIT announces its 1H 2023 results.

Debt

In this section, let us take a look at the debt of ParkwayLife REIT. Gearing ratio is the financial ratio between the equity (capital) versus the borrowings. Borrowings also refers to debt.

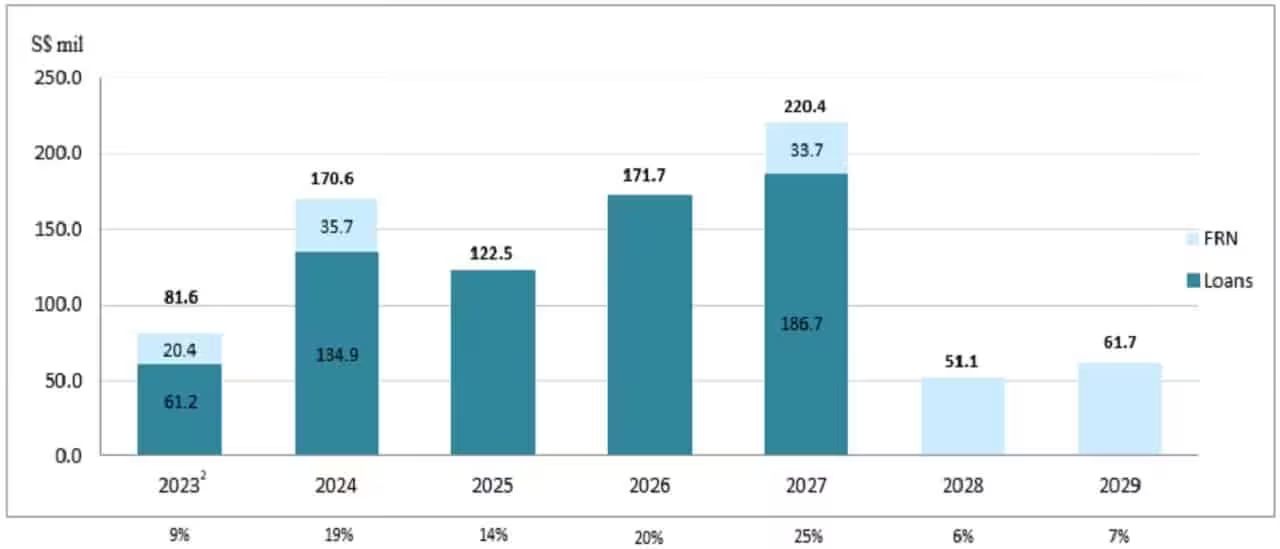

As of 31st March 2023, ParkwayLife REIT’s gearing ratio stood healthy at 37.5%. I like the way ParkwayLife REIT shared that they have ample debt headroom of S$318.3 million and S$584.5 million before reaching 45% and 50% gearing respectively.

Current weighted average debt term to maturity of 3.1 years. There is no long-term debt refinancing needs till February 2024.

In summary, ParkwayLife REIT has a good capital and financial management strategy. For convenience sake, I shall list them here but you can read more about them in their presentation slides.

- Acquisition financing has to be long-term: at least 3 years or more

- Diversify funding sources

- Maintain an unencumbered portfolio for financing flexibility

- Adopt natural hedge financing strategy to achieve stable net asset value

- Prudent financial risk management strategy for distribution stability

Occupancy

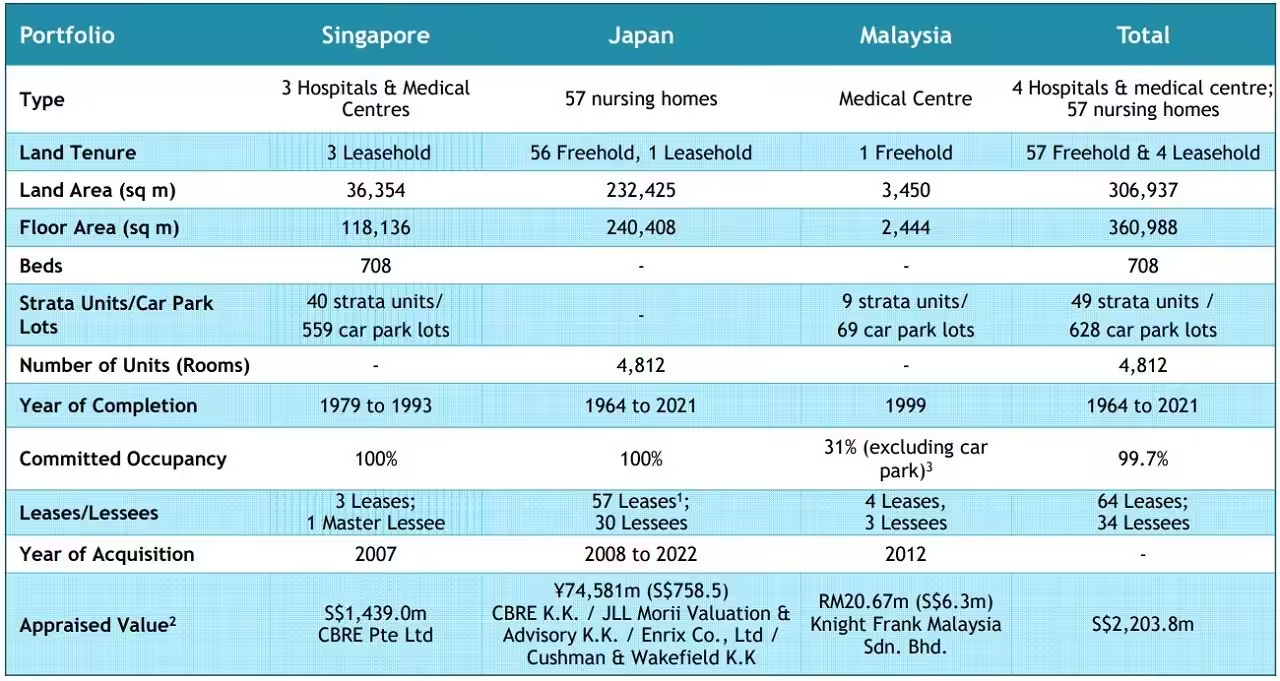

As of 31st March 2023, ParkwayLife REIT’s overall portfolio occupancy stood at 99.7%.

As you can see from the table above, the committed occupancy for both its Singapore and Japan properties are at 100%. Similar to past quarters, the Medical Centre in Malaysia remain a drag to its overall occupancy.

Current Dividend Yield

The Distribution Per Unit has grown 127.5% since IPO.

Now, we come to the big question. What is the current dividend yield of ParkwayLife REIT?

Based on the current share price of S$3.95 and FY22 distribution per unit of 14.38 cents, this translate to a current dividend yield of 3.64%. In my opinion, the current dividend yield is pretty low as compared to other REITs.

Summary of ParkwayLife REIT 1Q2023 Business Update

We have came to the last section of this post. As usual, let me summarize the pros and cons.

Pros

- Gross revenue and Net Property Income grew 21.7% and 23.5% respectively year on year.

- Distribution Per Unit continue to grow year on year. In face, it has grown 127.5% since IPO.

- Healthy gearing ratio at 37.5% with further room for debt to fund acquisitions.

- No long-term debt refinancing needs till February 2024.

- High occupancy near to 100%.

Cons

- Depreciation of the Japanese Yen, thus offsetting the distribution income which is in Singapore Dollar.

- Lack lustre current dividend yield of 3.64% based on share price of S$3.95

In consideration of the above, I will not add more of ParkwayLife REIT given the low current dividend yield of 3.64%.