On 26th April 2023, Frasers Centrepoint Trust released their 1HFY23 Financial Results. Earlier this year, I wrote about Frasers Centrepoint Trust. Subsequently, I made my maiden entry and added the REIT to my stock portfolio.

With the relaxation of COVID-19 measures and borders reopening, most retail REITs have benefited from the return of shopper traffic. How has Frasers Centrepoint Trust fare in FY23 with its portfolio of suburban malls?

Let us find out more below.

Frasers Centrepoint Trust 1HFY23 Financial Results

In 1HFY23, Gross Revenue and Net Property Income increased by 6.5% and 5.7% respectively. The increase was driven by higher atrium income and rent growth.

In 1H2022, Frasers Centrepoint Trust had retained $4.8 million of its taxable income available for Distribution to Unitholders.

In 1H2023, Frasers Centrepoint Trust had released $1.7 million of its tax-exempt income available for distribution to Unitholders which was retained in 2H2022 and retained $3.0 million of its current period’s tax-exempt income available for distribution to Unitholders.

Despite the increase in Gross Revenue and Distribution to Unitholders, Distribution Per Unit (DPU) declined by 0.3% from 6.136 cents to 6.13 cents. I am not so much concern because the difference is merely 0.006 cents.

| 1HFY23 (S$’000) |

1HFY22 (S$’000) |

Change | |

| Gross Revenue | 187,592 | 176,187 | 6.5% |

| Net Property Income | 137,963 | 130,479 | 5.7% |

| Distribution to Unitholders | 104,679 | 104,413 | 0.3% |

| Distribution Per Unit (“DPU”) (cents) | 6.13 | 6.136 | (0.1)% |

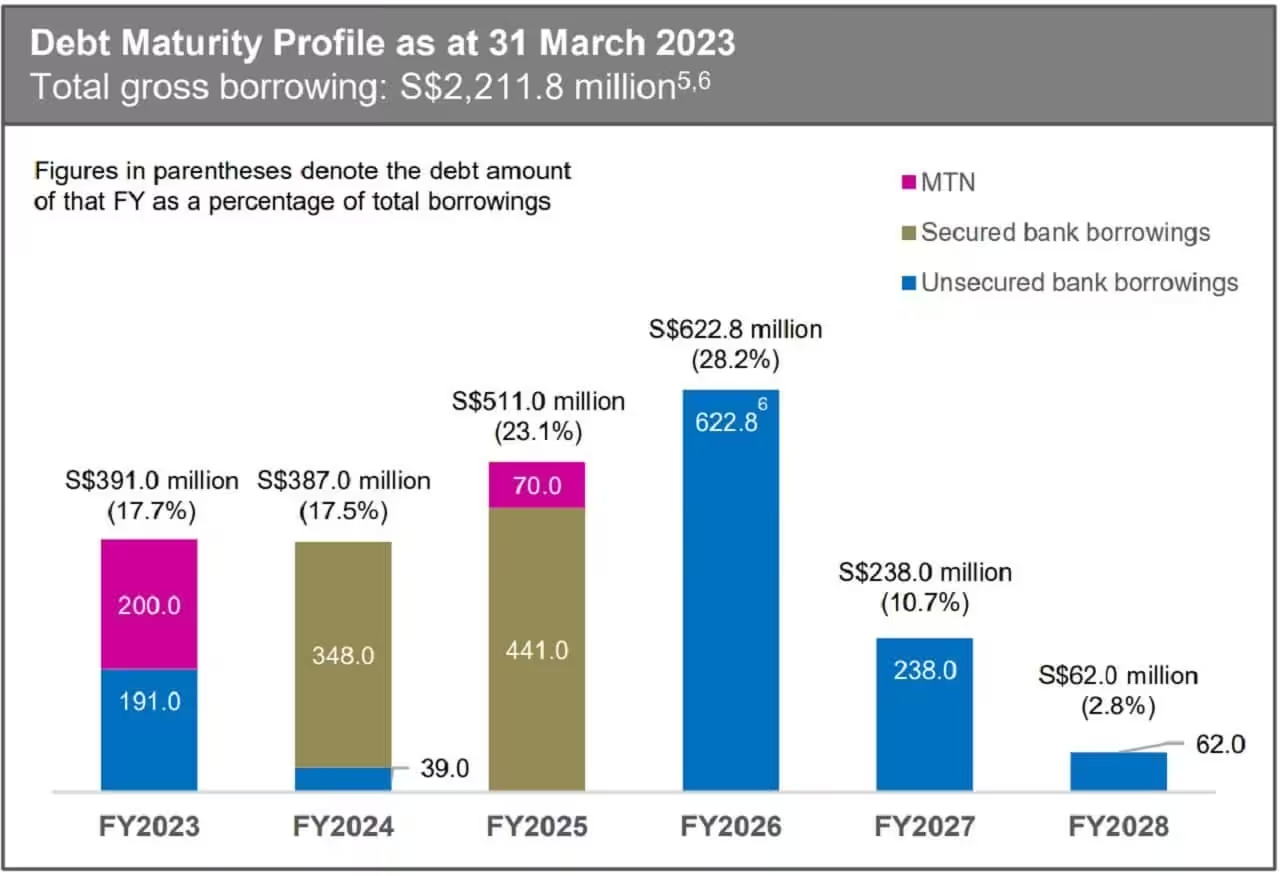

Debt

As of 31st March 2023, the gearing ratio stood at 39.6%. This was a significant increase from 33.9% as of 31st December 2022. The increase was due to the joint acquisition of NEX with Frasers Property.

Average debt maturity stood at 1.91 years with 76.4% of debt hedged to fixed rate interest.

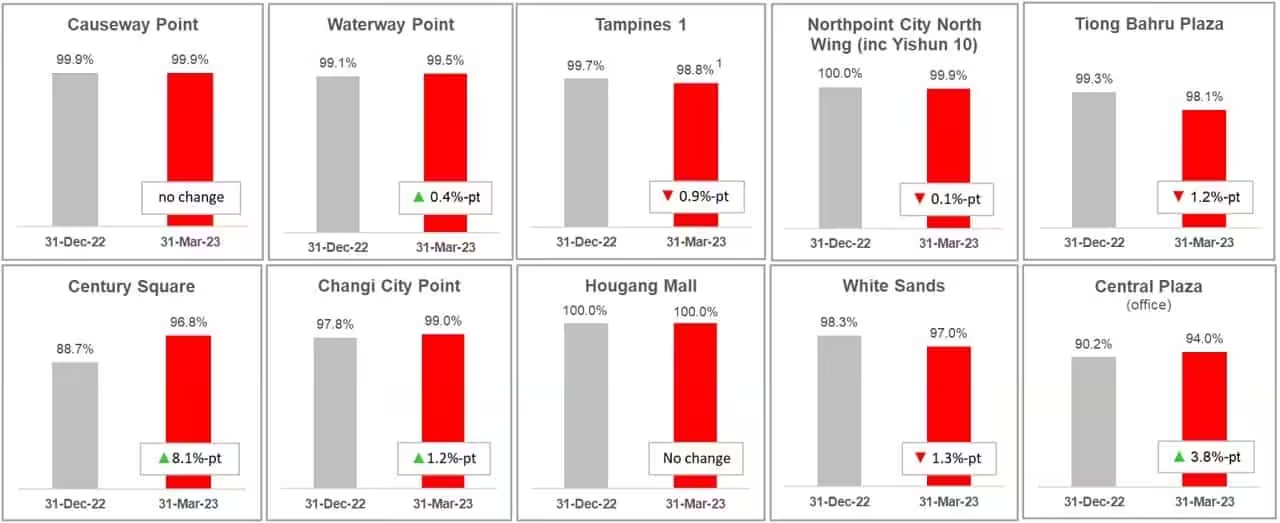

Occupancy

Frasers Centrepoint Trust’s retail portfolio committed occupancy hit a high of 99.2%. As shared previously, Frasers Centrepoint Trust has secured commitment for anchor cinema space at Century Square.

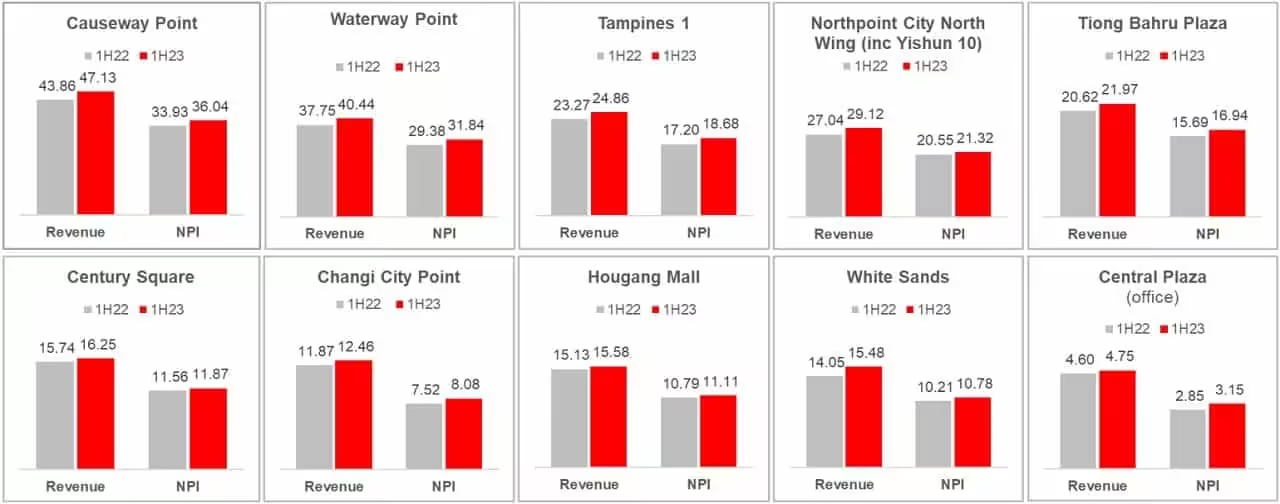

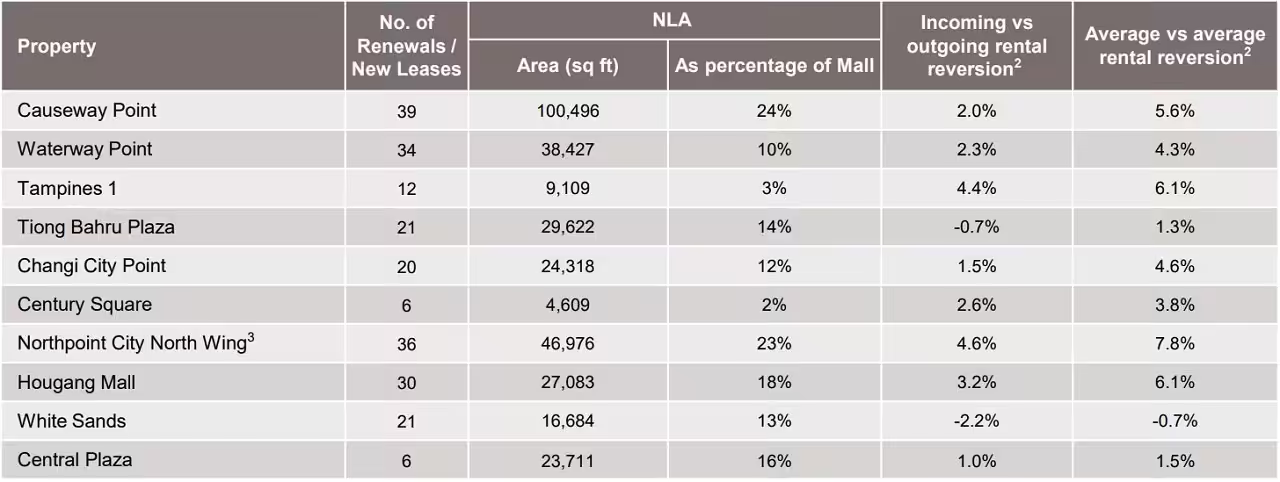

I really like the way Frasers Centrepoint Trust show the Revenue and Net Property Income (NPI) contribution and growth for each of their malls. I hope the other retail REITs could do the same way too in their presentation slides.

In 1H2023, the retail portfolio rental reversions were +1.9% (income vs outgoing) and +4.3% (average vs average). A positive rent reversion refers to an increase in rental rates.

Current Dividend Yield

Based on the current share price of S$2.21 and FY22 full year distribution of 12.227 cents, the current dividend yield for Frasers Centrepoint Trust works out to be 5.53%. I am satisfied with any dividend yield above 5%.

Summary Frasers Centrepoint Trust 1HFY23 Financial Results

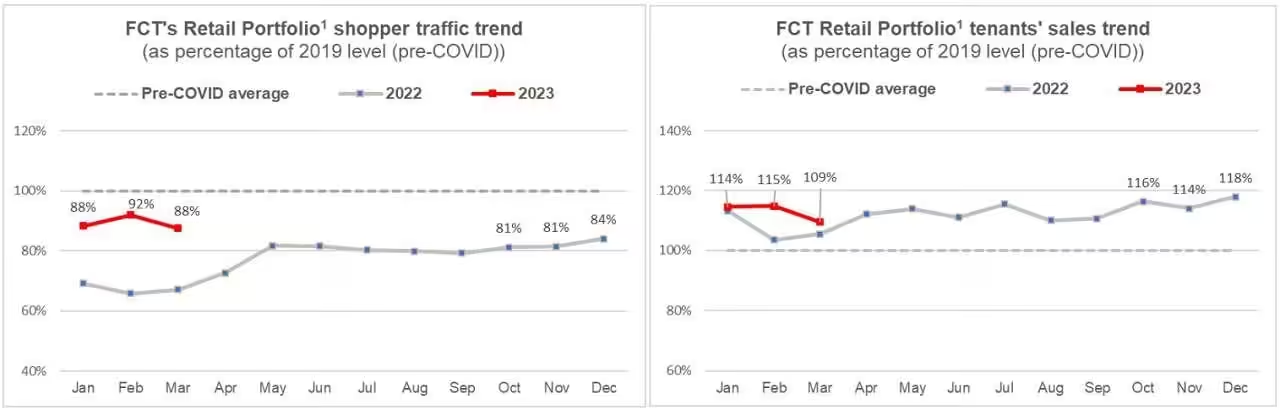

Similar to other retail REITs, Frasers Centrepoint Trust enjoyed strong recovery in shopper traffic and robust tenants’ sales growth. In 1H2023, tenants’ sales is 9.2% higher y-o-y and shopper traffic is 35.3% higher y-o-y.

Here are the pros and cons.

Pros

- Gross Revenue and Net Property Income (NPI) increased by 6.5% and 5.7% respectively, driven by higher atrium income and rent growth.

- Committed occupancy hit a high of 99.2%.

- Satisfactory current dividend yield of 5.53%.

- Positive rental reversions.

- Strong recovery in shopper traffic and robust tenants’ sales growth.

Cons

- High gearing ratio at 39.6%.

Good compamy