On 20th April 2023, Suntec REIT held its AGM (Annual General Meeting) for FY22. I used to be a unit holder of Suntec REIT but I have divested Suntec REIT back some time ago.

Is it worth adding Suntec REIT back to my stock portfolio? I will like to take a look at its FY2022 results.

Overview of Suntec REIT’s Portfolio

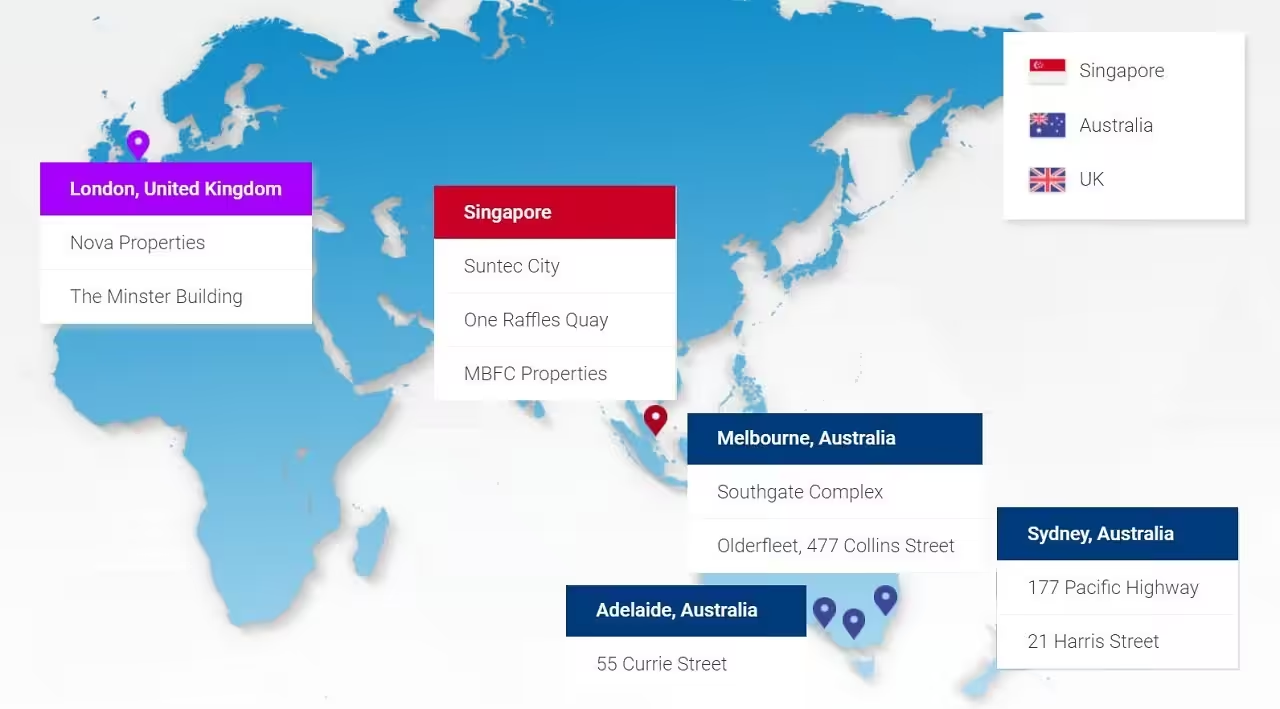

Before I start, let me take a look at the assets under Suntec REIT’s portfolio. As shown in the picture below, Suntec REIT has a total of 3 assets in Singapore, 2 assets in London United Kingdom and 5 assets in Australia.

FY22 Financial Performance

In FY22, Suntec REIT delivered S$255.5 million of distributable income to unit holders which was a 3.4% year on year increase. A full year Distribution Per Unit (DPU) of 8.884 cents was paid in FY22, representing a 2.5% year on year increase. The increase was due to higher NPI from better operating performance but these were offset by higher proportion of asset management fees in cash (50%) vs FY 21 (20%).

In FY22, Gross Revenue and Net Property Income (NPI) increased 19.3% and 24% respectively. This was attributed to higher contributions from Suntec City Office, Suntec City Mall and Suntec Convention and The Minster

Building in London. The gains were offset by the lower occupancy and absence of surrender fee in FY22. Surrender fee was received in FY21 at 177 Pacific Highway in Sydney. The gains were also affected by the weaker AUD and GBP against SGD.

Joint Venture (JV) income increased 3.3%. This was mainly due to the absence of performance fees paid to fund manager for 9 Penang Road in FY21. Second, the higher contributions from One Raffles Quay, MBFC Properties and Nova Properties, London. Lower contributions from Southgate Complex, Melbourne offset the gains. The weaker AUD and GBP against SGD also affected the income.

Debt

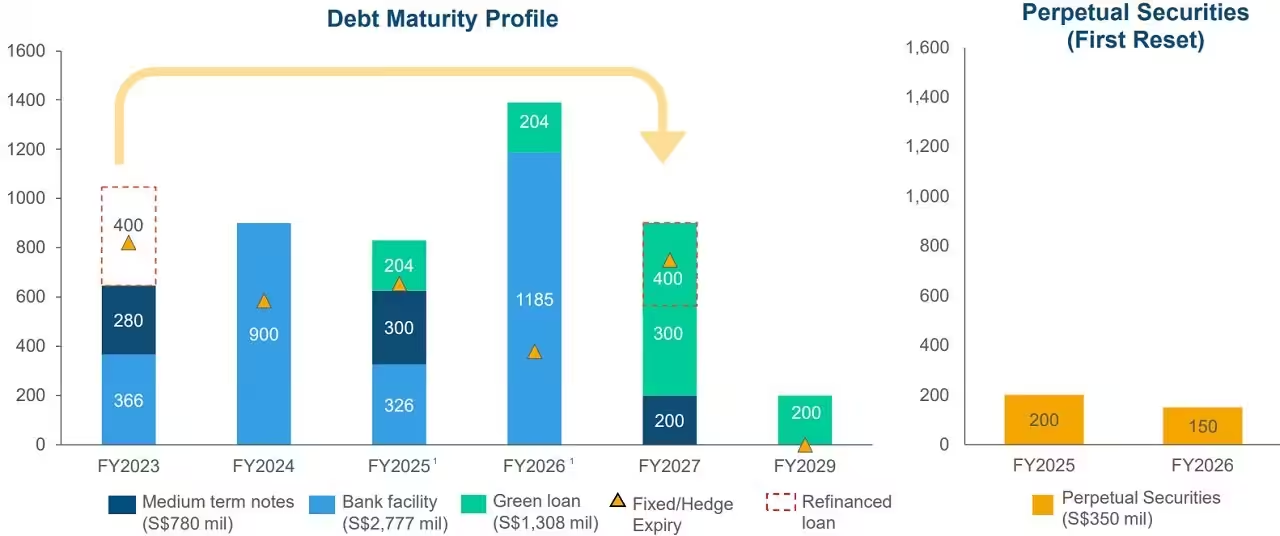

In this section, let us take a look at Suntec REIT’s debt. In the current economic situation, I prefer REITs with low debt due to the rising interest rates and foreign exchange risks.

As of 31st December 2022, the aggregate leverage ratio was high at 42.4%. Weighted Average Debt Maturity stood at 2.85 years.

As shown in the chart below, Suntec REIT has refinanced S$400 mil loan with Sustainability-Linked Loan.

Occupancy

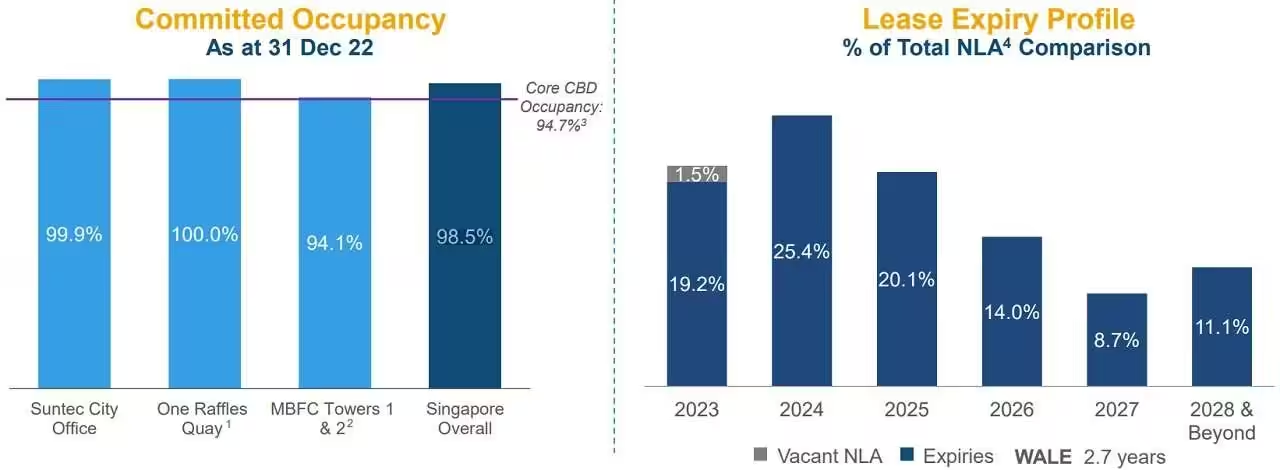

Suntec REIT’s portfolio comprises of offices and retail. Let us take a look at the Singapore Office Portfolio first.

Singapore Office Portfolio

As of 31st December 2022, Singapore office overall portfolio committed occupancy stood at 98.5%. Weighted Average Lease Expiry (WALE) stood at 2.7 years.

If you look at the lease expiry profile, 19.2% of the leases are expiring in 2023. Since this is FY22 data, investors might wish to keep a look out for Suntec REIT’s FY23 operational updates on the lease expiry numbers.

What was worth mentioning was Suntec REIT office portfolio achieved 18 quarters of positive rent reversion. A positive rent reversion refers to an increase in rental rates.

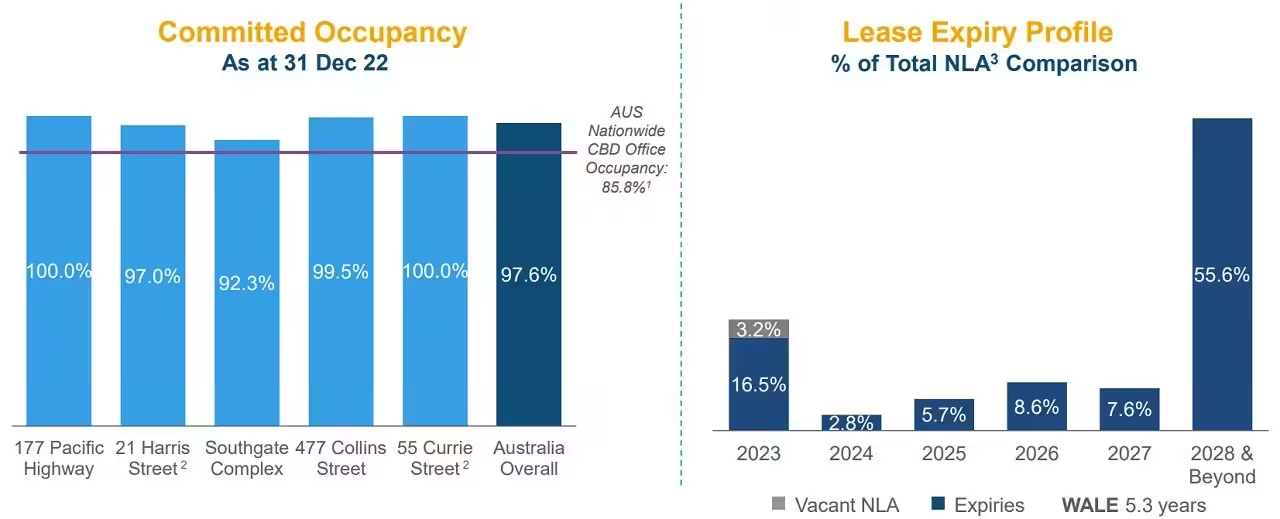

Australia Office Portfolio

As of 31st December 2022, Australia office overall portfolio committed occupancy stood at 97.6%. Weighted Average Lease Expiry (WALE) stood at 5.3 years.

In FY22, the Australia Office Portfolio achieved a positive rental reversion of 24.3%.

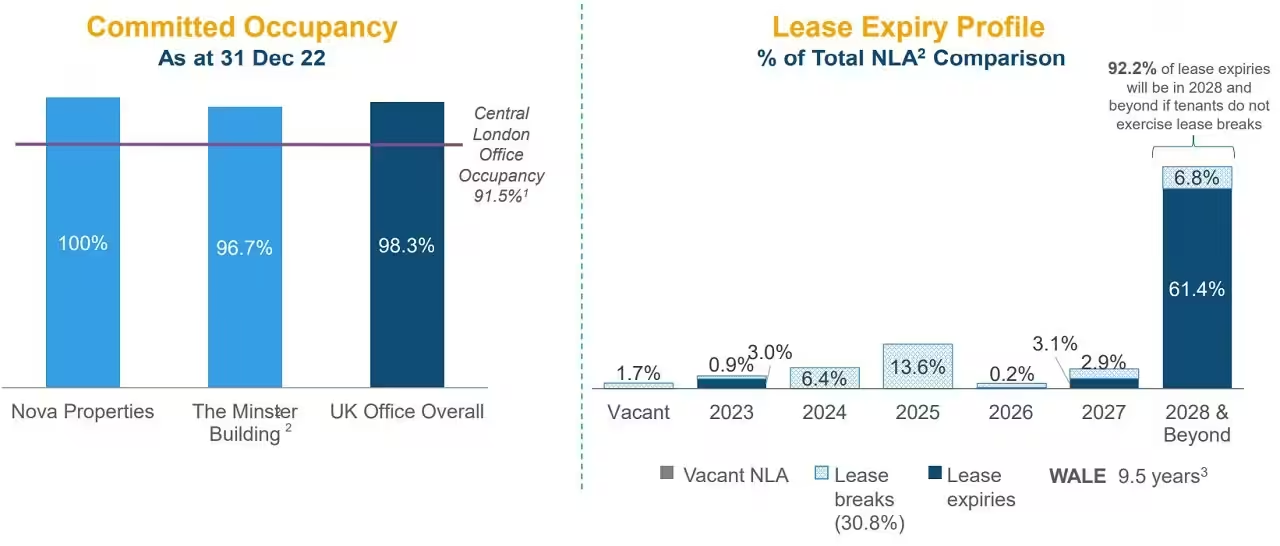

United Kingdom Office Portfolio

Suntec REIT’s UK portfolio has a rather long WALE of 9.5 years. The overall UK office occupancy stood at 98.3%. Unless the tenants break the lease, there is nothing to be concern about here.

Singapore Retail Portfolio

Singapore retail overall portfolio committed occupancy stood at 98.1%. Weighted Average Lease Expiry (WALE) stood at 2.3 years.

In FY22, the retail portfolio achieved a positive rental reversion of 4.4%. With the relaxing of COVID-19 restrictions and reopening of borders, the flagship Suntec City Mall has achieved 3 quarters of positive rental reversion. Events and roadshows have also recovered to 2019 levels.

Looking at the chart above, shopper traffic and tenant sales are on the uptrend which reflects the recovery from the impact of COVID-19.

Current Dividend Yield

Now that we have gone through the financial performance, debt and occupancy, we probably will ask if this is the right time to buy?

Let us take a look at the current dividend yield. Based on the closing share price of S$1.43 on 21st April 2023 and FY22 full year distribution of 8.884 cents, this works out to be 6.21%.

Summary of Suntec REIT AGM for FY22

We have came to the summary section. As usual, let me summarize the pros and cons.

Pros

- Distributable income and Distribution Per Unit (DPU) increased 3.4% and 2.5% year on year respectively.

- Both office and retail overall occupancy stood strong.

- Recovering shopper traffic and tenant sales. Events are also returning to Suntec Convention even though I never mention in this article.

- High current dividend yield of 6.21% based on the current share price of S$1.43.

Cons

- Gross revenue and distribution eroded by the weaker AUD and GBP against SGD.

- Aggregate leverage ratio was high at 42.4%.

Have I missed out anything? Please feel free to comment below.