There was a trading halt for OUE Hospitality Trust on 8th April 2019 and investors like me who are vested in OUE Hospitality Trust smell something fishy. The announcement came shortly. The respective managers of OUE Commercial REIT (“OUE C-REIT”) and OUE Hospitality Trust (“OUE H-Trust”) jointly announced the proposed merger of OUE C-REIT and OUE H-Trust (the “Proposed Merger”).

With the merger, the total assets will increase to approximately S$6.8 billion, making it one of the largest diversified S-REITs (Office and Hospitality).

The managers cited the following reasons for the proposed merger:

- Creation of one of the largest diversified S-REITs

- Larger capital base and broadened investment mandate provide flexibility and capability to drive long-term growth

- Enhanced portfolio diversification and resilience

- DPU accretive transaction

New Structure

With the merger, OUE Hospitality Trust investors get to own OUE Bayfront, One Raffles Place, OUE Downtown Office and Lippo Plaza which I deemed are quality assets to me.

OUE Hospitality Trust Security Holders

Currently, OUE Hospitality Trust makes up 4% of my stock portfolio.

Based on the announcement, stapled security holders of OUE Hospitality Trust (the “Stapled Security holders”) will receive the following under the scheme consideration:

- S$0.04075 in cash per Stapled Security (“Cash Consideration”); and

- 1.3583 new OUE C-REIT units per Stapled Security (the “Consideration Units”).

Distribution Per Unit

The total DPU paid out by OUE Hospitality Trust in FY18 was 4.99 cents.

The Proposed Merger will be distribution per unit (“DPU”) accretive on a historical pro forma basis for both OUE C-REIT unitholders and OUE H-Trust Stapled Securityholders by 2.1% and 1.4% respectively, for the 12-month period ended 31 December 2018.

If the DPU for the new combined REIT is 5 cents, this is only 1 cent more than the current 4.99 cents paid out by OUE Hospitality Trust. I can be wrong but the accretion is actually 0.2%.

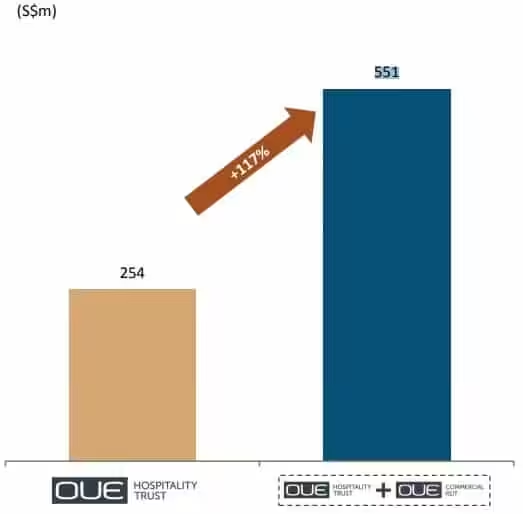

Debt

Based on the presentation slides, the enlarged REIT’s larger capital base will also enhance its funding capacity and flexibility, with (i) debt headroom increasing from approximately S$254 million (for H-Trust) to approximately S$551 million as at 31 December 2018.

The gearing for OUE Hospitality Trust and OUE Commercial Trust is 38.8% and 39.3% respectively. Gearing is expected to increase to 40.3% after the merger. This is currently very near the cap of 45%.

My Thoughts

As a dividend investor, I am very concern on the DPU accretion which after the merger does not seem so fantastic and in fact the post merger DPU seems flat to me. However, the cash consideration of S$0.04075 in cash per stapled security does appeal to me.

Gearing ratio has increased to 40.3% which I deemed as high and leaves little headroom for further acquisition.

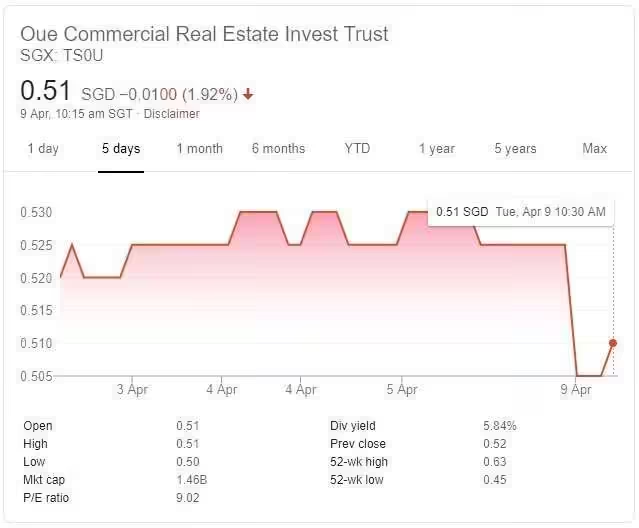

As you can see below, the stock market also does not support this merger. Share price declines slightly from S$0.735 to S$0.72.

Here is the share price of OUE Commercial REIT which declines from S$0.53 to S$0.51.

As an existing OUE Hospitality Trust investor, I probably will hold on for the cash per stapled security and continued flat DPU. If I am not yet vested, I will try to avoid OUE Hospitality Trust and OUE Commercial REIT in view of the high gearing after the merger.

Regarding the DPU, note that the management fees in the new REIT will be taken as 90% in units and the rest in charges. Formerly OUE H trust took 100% in units.

This accounts for the disparity of the DPU increase of the visible 0.2% versus the back calculated 1.4%.

I think it is better for longterm holders, such as me, for the management fees to be taken out of free cash flow. Otherwise there is a constant dilution of DPU due to the increasing number of units issued. However, others might prefer to have the higher DPU now to reinvest or for retirees the daily expenses.

I’m also a bit confused by how they calculated the 5 cents as if you take 3.48 cents (Combined REIT dpu) x 1.3583 you get 4.73 cents. In the notes, it was also mentioned that the 5 cents was derived based on investors taking their 4 cents in cash and reinvesting into C-Reit at 51 cents, but i was unable to get 5 cents when i did that.

To be conservative you can assume the dpu is actually 4.73.