The Hour Glass is in the simple business of selling luxury watches. They carry luxury brands like Patek Philippe, Rolex and Cartier etc. They have 41 boutiques in nine key cities throughout Asia. The Hour Glass has been accorded the ‘Best Watch Retail’ honours by Singapore Tatler in 2014.

Similar companies in the luxury watches business are Sincere Watch (Hong Kong) Ltd and Cortina Holdings Limited.

Market Capitalization

The Hour Glass has a large market capitalization of estimated 500 million.

Financials Over Last 5 Years

At a glance into The Hour Glass FY15 Annual report, the company has a financially strong balance sheet.

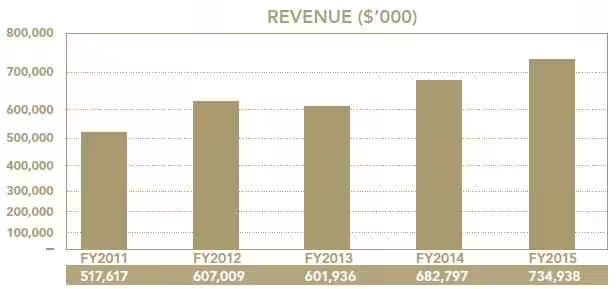

Increasing Revenue

The Hour Glass revenue has increased over the last 5 years.

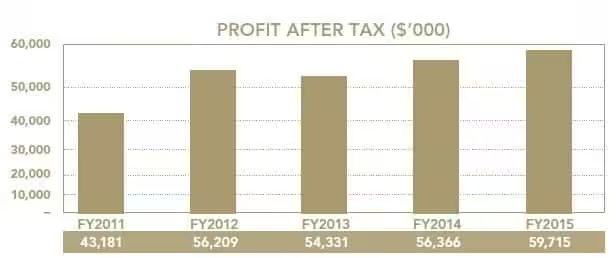

Increasing Profits

The Hour Glass profit after tax has increased over the last 5 years.

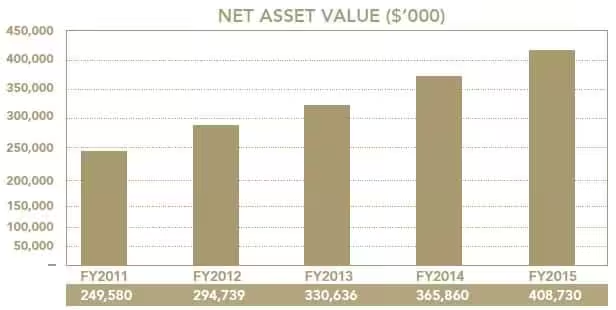

Increasing Net Asset Value

The Hour Glass Net Asset Value has also grown over the 5 years.

Dividends

The Hour Glass consistently pays dividends over the 6 years period.

Earnings per share has also increased consistently. It is worthy to note that in year 2014, The Hour Glass has a sub-division offer of 3 for 1 which causes the earnings per share to be reduced to 8.22 cents in year 2015.

If you look at the dividend payout ratio, it remains fairly consistent with a slight increase of 1%.

| Year | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 |

| Total dividend (cents) | 3.5 | 5 | 6 | 5.5 | 6 | 2.2 |

| Earnings per share (cents) | 14.08 | 18.10 | 23.33 | 22.49 | 23.38 | 8.22 |

| Dividend payout ratio (%) | 25 | 28 | 26 | 24 | 26 | 27 |

Debt

The Hour Glass has a low debt servicing ratio. This means that its debt can be easily paid off by its operating profits without running into cash flow issues.

| Year | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 |

| Net interest expense (SGD dollar in thousands) | 425 | 552 | 316 | 488 | 489 | 901 |

| Operating income (SGD dollar in thousands) | 20,624 | 20,647 | 28,865 | 12,939 | 64,337 | 37,145 |

| Debt service ratio (%) | 2.1% | 2.7% | 1.1% | 3.8% | 0.8% | 2.4% |

Challenges

Luxury Consumption vs State of Economy

The Hour Glass is in the luxury watch business and luxury consumption is led by the state of the economy. Under good times, people have more spending power and thus the ability to spend on luxury goods. The Hour Glass business is thus cylindrical.

“The Chinese Premium”

PRCs no longer prepared to pay “The Chinese Premium”. Sales dropped by 40% in Hong Kong as PRC shoppers bought less due to price imbalances against other shopping destinations such as Europe and Dubai.

Investment Strategy

Currently, The Hour Glass only makes up 3% of my portfolio. I liked this stock for its strong balance sheet. The shares currently trade at $0.70 on Singapore Exchange and may fell further in the short term given the overall current market weakness. The current P/E is 8.22.

Summary of my reasons to stay invested

- Simple luxury watch business

- Good management

- Consistent dividend

- Consistent profitability and performance (Revenue, Profits and NAV)

- Low debt servicing ratio