ISOTeam offers services related to building maintenance and estate upgrading industry. ISOTeam’s major customers include town councils, government bodies as well as private sector building owners.

The range of services ISOTeam offers are

- Upgrade and Retrofit Works

- Repairs and Decoration Works

- Reroofing and Waterproofing Works

- Facade Restoration and Cleaning Works

- Home Painting Services

- ISO Pest Management

- Access Rental Services

Management

ISOTeam has a total of 234 employees and 493 general workers. Mr David Ng Cheng Lian is current Chairman and the founder of ISOTeam. Mr Anthony Koh Thong Huat is one of the co-founder and current CEO for the group. Both of them currently holds 2.70% direct interest in the shares and 41.14% deemed interest in the shares of the company. Both of them have more than 30 years of experience in the building maintenance and estate upgrading industry.

Market Capitalization

As of 31st December 2016, the total number of shares stands at 281,122,956. At the closing price of S$0.38, the market capitalization is estimated at $106 million. Thus ISOTeam is classified as a small cap stock.

Revenue and Gross Profit

Revenue and Gross Profit has been increasing from FY12 to FY16.

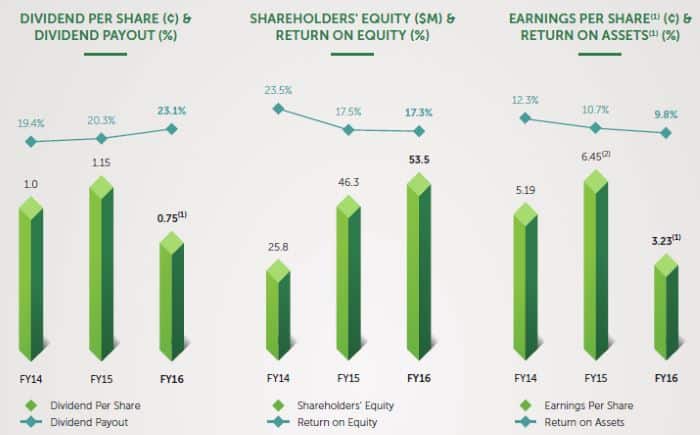

Return On Equity

Although, return on shareholders equity (ROE) has been declining, it remains above 15%.

Return on equity (ROE) is a measure of profitability that calculates how many dollars of profit a company generates with each dollar of shareholders’ equity.

The formula for ROE is: ROE = Net Income/Shareholders’ Equity. ROE is sometimes called “return on net worth. – InvestingAnswers”

Cash Flow

Cash flow has been improving except for a slight drop from FY2015 to FY2016. Earnings are expected to be lumpy for companies such as ISOTeam whereby they engage in project based work.

|

2013

$ ‘000 |

2014

$ ‘000 |

2015

$ ‘000 |

2016

$ ‘000 |

| Net cash generated from operating activities |

(211) |

6,747 |

17,063 |

15,607 |

Dividends

The company has been paying dividends over the past few years. For the past years, ISO Team does not have a fixed dividend policy, however on 4th October 2016, ISO Team has declared a 20% dividend policy moving forward.

|

2013 |

2014 |

2015 |

2016 |

| Total dividend (cents) |

1 |

1 |

1.15 |

0.75 |

| Earnings per share (cents) |

5.11 |

5.19 |

6.45 |

3.23 |

| Dividend payout ratio (%) |

19.57 |

19.27 |

17.83 |

23.33 |

Based on the total dividends paid in 2016 and current closing price of $0.405, the dividend yield is 1.85%. Thus, ISOTeam is definitely not a good stock to buy for its dividend.

Strength and Catalyst

1. Expansion into Myanmar

We all know that Myanmar is an emerging market where there are good business opportunities. ISOTeam has clinched its first painting job in Myanmar in August 2016 via a joint venture with Nippon Paint.

2. Expansion into Solar Energy Market

Solar Energy is the next upcoming trend in the energy market.

ISOTeam’s first renewable energy project was to install Grid-Tied Solar Photovoltaic Systems on the roofs of 33 blocks at Tampines worth approximately $1.8 million.

In August 2016, ISOTeam won its 2nd renewable energy project in Singapore (Emergency Fuel Cell Operating Power Systems). ISO Team was awarded a $0.20 million contract to install Emergency Fuel Cell Operating Power Systems as back-up power generators for lifts of a number of HDB blocks at Punggol, a green initiative which it believes may potentially be implemented in more public housing blocks in Singapore.

On 10th January 2017, ISOTeam won their third and single largest renewable energy installation project worth $6.3 million awarded by Sunseap Leasing Pte Ltd. The installation work involves solar leasing of grid-tied solar photovoltaic system for 150 HDB blocks and is expected to be completed between January 2017 and June 2018.

3. Expansion through Strategic Partnerships

ISOTeam seems to capture the essence of doing business which is to build good relationships with its partners. Through partnerships, ISOTeam is able to diversify and expand its business. Moving forward, I will think ISOTeam will continue to partner with other companies and expand its business. A good example is how ISOTeam partnering with Nippon to expand into the Myanmar market.

Investment Risks

1. Labour Intensive Nature

The nature of ISOTeam’s business is labour intensive. As such, there is high possibility of higher labour costs eroding away operating profits. Prudent management is very important to control growing labour costs as ISOTeam expands its business.

2. Over-reliance on few major customers

ISOTeam’s customer base concentrates around town councils and government bodies. Its projects are mostly upgrading and maintenance of Housing Development Buildings. However, we can see through strategic partnership such as TMS Alliances, ISOTeam is trying to diversify and offer a wider range of services such as home painting services and pest control.

3. Lumpy Earnings

As the business nature of ISOTeam is a project based business, earnings tend to be lumpy. The good news is that Singapore government has always been pro-actively maintaining and upgrading its estates and property.

Conclusion

I shall not be investing in ISOTeam for the following reasons

- Not a dividend stock

- Unpredictable earnings by the nature of its business

- Cannot tell if it is a growth stock. Looking at the financials, the ROE has been declining although revenue and gross profit are growing. Value investors can claim that ISOTeam is preserving capital to grow the company but at the moment, I cannot tell whether ISOTeam is concern about returning the value back to shareholders.

I agree, no clear sight forward and it is over price. I think centurion or cogent is a better choice. Take a look.