On 27th April 2023, Mapletree Pan Asia Commercial Trust (MPACT) released their 4Q FY22/23 financial results. To recap, Mapletree Pan Asia Commercial Trust is a merger between Mapletree Commercial Trust and Mapletree North Asia Commercial Trust to form one of the top 10 largest REIT in Asia.

Before I drill into the 4Q FY22/23 financial results, I will like to share the properties in Mapletree Pan Asia Commercial Trust’s portfolio. MPACT has a total of 18 properties across Singapore, China, Hong Kong, South Korea and Japan. As at 31 March 2023, MPACT’s total assets under management was S$16.6 billion.

MPACT 4Q FY22/23 Financial Results

In 4Q FY22/23, Gross Revenue and Net Property Income (NPI) increased 85.9% and 82.2% year-on-year respectively. This was boosted by the full-quarter contribution from properties acquired through the merger and higher contribution from the Singapore portfolio.

The Distribution Per Unit (DPU) declined by 17.3% from 2.72 cents to 2.25 cents quarter by quarter. This is because in 4Q FY21/22, the distribution included the release of S$15.7 million retained in 4Q FY19/20.

If we exclude the cash retention, the Distribution Per Unit (DPU) remains flat at 2.25 cents.

| 4Q FY22/23 (S$’000) |

4Q FY21/22 (S$’000) |

Change | |

| Gross Revenue | 233,271 | 125,476 | 85.9% |

| Net Property Income | 177,378 | 97,376 | 82.2% |

| Property expenses |

(55,893) | (28,100) | 98.9% |

| Amount Distributable To Unitholders | 117,590 | 90,179 | 30.4% |

| Distribution Per Unit (“DPU”) (cents)

Including the Release of Retained Cash |

2.25 | 2.72 | 17.3% |

| Distribution Per Unit (“DPU”) (cents)

Excluding the Release of Retained Cash |

2.25 | 2.25 | – |

MPACT FY22/23 Financial Results

In FY22/23, MPACT achieved year-on-year growth of 65.4% and 62.6% in Gross Revenue and Net Property Income (“NPI”), respectively, with both figures reaching S$826.2 million and S$631.9 million.

The increase was mainly driven by contribution from properties acquired through the merger. Higher earnings from MPACT’s core assets, VivoCity and MBC also contributed to the increase. These increases helped to cushion the increase in utility and finance costs.

Distribution per Unit (“DPU”) was up 6.1% year-on-year to 9.61 Singapore cents if we exclude the release of retained cash in FY21/22.

| FY22/23 (S$’000) |

FY21/22 (S$’000) |

Change | |

| Gross Revenue | 826,185 | 499,475 | 65.4% |

| Net Property Income | 631,942 | 388,681 | 62.6% |

| Property expenses |

(194,243) | (110,794) | 75.3% |

| Amount Distributable To Unitholders | 445,598 | 316,982 | 40.6% |

| Distribution Per Unit (“DPU”) (cents)

Including the Release of Retained Cash |

9.61 | 9.53 | 0.8% |

| Distribution Per Unit (“DPU”) (cents)

Excluding the Release of Retained Cash |

9.61 | 9.06 | 6.1% |

Debt

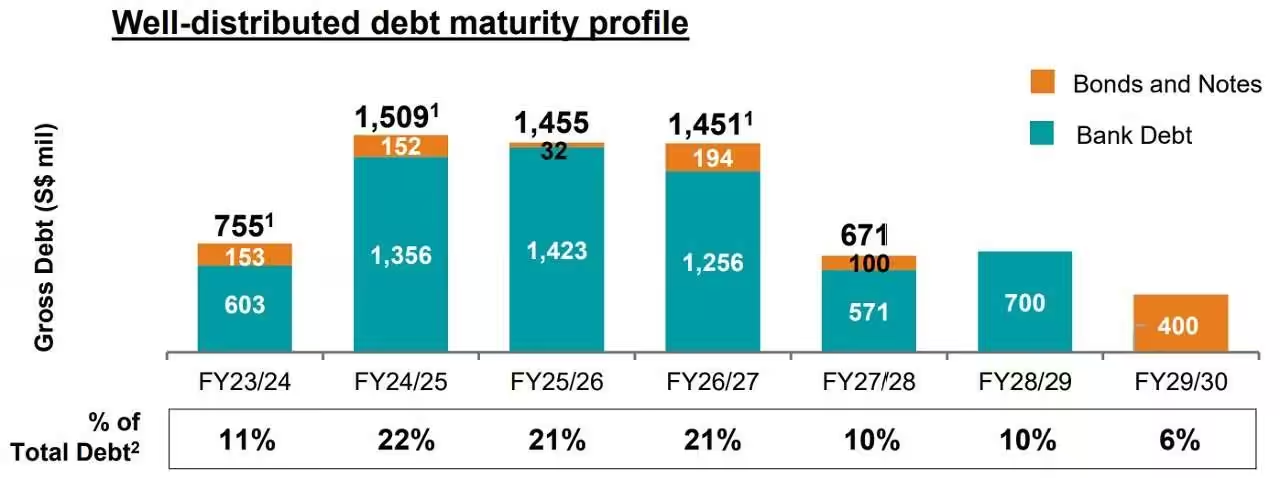

As of 31st March 2023, gearing ratio stood high at 40.9%. Average Term to Maturity of Debt stood at 3 years.

Debt Maturity Profile was well distributed with only 11% of total debt requiring refinancing in FY23/24.

75.5% of the debt was also hedged at fixed rate to mitigate against sudden interest rate hikes.

Occupancy

As at 31 March 2023, the portfolio committed occupancy was 95.4%.

All the markets achieved positive rental uplifts except Greater China.

The overall portfolio Weighted Average Lease Expiry (WALE) stood at 2.6 years. The WALE for MPACT’s retail and office/business park leases was 2.0 years and 3.0 years respectively.

As you can see from the chart below, the lease expiries are well staggered.

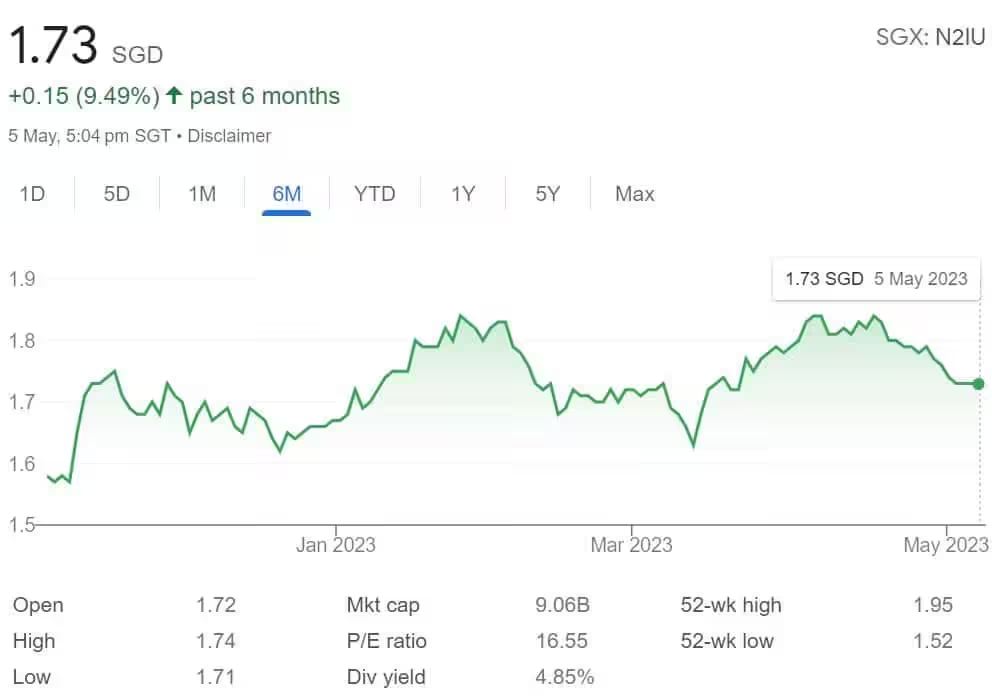

Current Dividend Yield

What price will give you a good dividend yield? Based on FY22/23 full year distribution of 9.61 cents and current share price of S$1.73, this translate to a current dividend yield of 5.55%.

Summary of MPACT 4Q FY22/23 Financial Results

Here are the pros and cons.

Pros:

- Gross Revenue and Net Property Income (“NPI”) grew 65.4% and 62.6% year-on-year respectively.

- Debt Maturity Profile was well distributed with only 11% of total debt requiring refinancing in FY23/24.

- 75.5% of the debt was hedged at fixed rate.

- Portfolio committed occupancy is healthy at 95.4%.

- Good current dividend yield at 5.55%.

- Distribution per Unit (“DPU”) was up 6.1% year-on-year to 9.61 Singapore cents.

Cons:

- Gearing ratio stood high at 40.9%.

- Rental for Greater China market remains negative.

To end it off, I would expect MPACT to perform better given any merger. The China and Hong Kong assets remain a drag to its overall portfolio.

Looking on the bright side, the reopening of China borders could inject some positivity or act as a catalyst to MPACT.