On 24th July 2024, Mapletree Logistics Trust released their 1QFY24/25 financial results. As you can see from above, Mapletree Logistics Trust has been divesting their assets with older specifications and of limited redevelopment potential as part of portfolio rejuvenation. In 1QFY24/25, Mapletree Logistics Trust also completed the acquisitions from its Sponsor of three modern, Grade A assets in Malaysia and Vietnam.

Previously, the manager of Mapletree Logistics Trust shared that they expect negative rental reversions in China over the next few quarters as the expiring rental rates are marked to market. Can its diversified portfolio across other countries mitigate the weaker performance in China? Let us find out more below.

Mapletree Logistics Trust 1QFY24/25 Financial Results

In 1QFY24/25, Mapletree Logistics Trust’s gross revenue was 0.3% lower year-on-year. This was due to lower contribution from China, absence of revenue contribution from divested properties and currency weakness (mainly JPY and CNY). The loss was mitigated by higher contribution from Singapore and Hong Kong SAR, and contributions from acquisitions completed in 1Q FY24/25 and FY23/24. Net property income (“NPI”) also fell 0.9% year-on-year to S$156.7 million.

I wanted to highlight that 78% of amount distributable in the next 12 months is hedged into or derived in SGD to mitigate against Forex weakness.

Higher borrowing costs continue to plague the financial performance of Mapletree Logistics Trust. Borrowing costs rose 9.4% year-on-year to S$38.5 million.

Amount distributable to Unitholders declined by 7.4% year-on-year to S$103.7 million. As a result, distribution per unit (“DPU”) fell 8.9% year-on-year to 2.068 cents.

| 1QFY24/25 (S$’000) |

1QFY23/24 (S$’000) |

% Change | |

| Gross Revenue | 181,696 | 182,194 | (0.3) |

| Property Expenses |

(25,001) | (24,051) | 3.9% |

| Net Property Income | 156,695 | 158,143 | (0.9) |

| Borrowing Costs | (38,453) | (35,137) | 9.4 |

| Amount Distributable | 103,733 | 111,972 | (7.4) |

| Distribution Per Unit (“DPU”) (cents) | 2.068 | 2.271 | (8.9%) |

Debt

As of 30th June 2024, Mapletree Logistics Trust’s aggregate leverage ratio stood high at 39.6%. The higher gearing was because net debt increased by S$179 million. Additional loans were drawn to fund

acquisitions in Malaysia and Vietnam completed during the quarter. The increase in debt was partly offset by loan repayments with proceeds from the recent divestments.

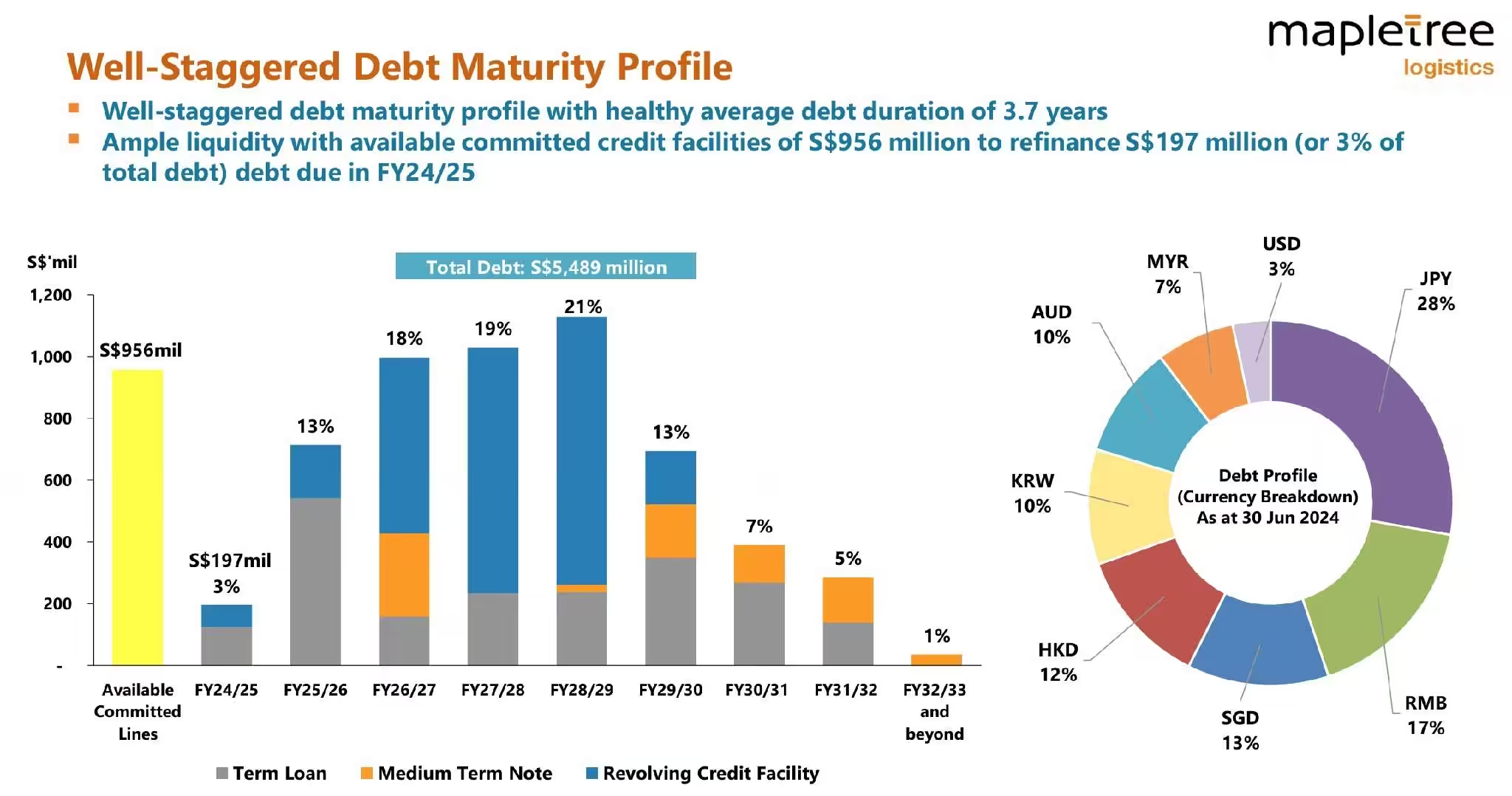

The high gearing of 39.6% sounds a bit worrying for investors. However, the manager of Mapletree Logistics Trust shared in their presentation slides that they have ample liquidity with available committed credit facilities of S$956 million to refinance S$197 million (or 3% of total debt) debt due in FY24/25. From the bar chart above, you can also see that it has a well-staggered debt maturity profile with healthy average debt duration of 3.7 years.

83% of total debt is hedged or drawn in fixed rates to mitigate against interest rate hikes.

Occupancy

Mapletree Logistics Trust’s portfolio occupancy fell from 96.0% in 4QFY23/24 to 95.7% in 1QFY24/25. The lower occupancy rates in Singapore and Vietnam were due to leasing downtime which is expected to backfill by 2QFY24/25. Malaysia’s lower occupancy rate was mainly due to lease expiries at 2 properties slated for redevelopment. Excluding these properties, Malaysia’s occupancy rate was 99.7%.

Despite a lower occupancy, Mapletree Logistics Trust’s portfolio achieved an average positive 2.6% rental reversions for leases renewed in 1QFY24/25. 51% of the lease expiries in 1QFY24/25 came from China, which recorded a negative reversion rate of 11.3%. Excluding China, Mapletree Logistics Trust’s portfolio rental reversion was positive +4.6%.

Do you know what is rental reversion? Rental reversion refers to the change in rental rates when leases are renewed. A positive rental reversion means the new rental rate is higher than the previous rate. A negative rental reversion happens when the new rental rate is lower than the previous rate. Whether the rental reversion is positive or negative depends on the market demand and supply.

Lease Expiry

Weighted average lease expiry for the portfolio stood at approximately 2.9 years. As this is just the first quarter of FY24/25, we need to closely monitor the lease expiries in subsequent quarters as 24.5% of leases still need to be renewed.

As you can see from the chart above, overall lease expiry is well staggered.

Mapletree Logistics Trust Share Price and Dividend Yield

As you can see from the above chart, Mapletree Logistics Trust share price has been on the downtrend over the past 6 months. Mapletree Logistics Trust share price currently stood at S$1.28 on Wednesday, 31st July 2024. Based on the Mapletree Logistics Trust dividend of 9.003 cents in FY23, Mapletree Logistics Trust’s current dividend yield is 7.03%.

Do you know how to calculate the current dividend yield? The formula for calculating the current dividend yield is straightforward. It is calculated by dividing the annual dividends per share by the current market price per share. Here is the formula in mathematical terms:

Summary of Mapletree Logistics Trust 1QFY24/25 Financial Results

We have come to the end of this post and let me summarize the pro and cons based on its financial results.

The pros are:

- 78% of amount distributable in the next 12 months is hedged into or derived in SGD to mitigate against Forex weakness.

- Ample liquidity with available committed credit facilities of S$956 million to refinance S$197 million (or 3% of total debt) debt due in FY24/25.

- Well-staggered debt maturity profile with healthy average debt duration of 3.7 years.

- Overall lease expiry is well staggered.

- Achieved positive rental reversions of 2.6% for leases renewed in 1QFY24/25.

- High current dividend yield of 7.03%.

The cons are:

- Gross revenue was 0.3% lower year-on-year.

- Net property income (“NPI”) also fell 0.9% year-on-year to S$156.7 million.

- Distribution per unit (“DPU”) fell 8.9% year-on-year to 2.068 cents.

- Aggregate leverage ratio stood high at 39.6%.

- Net debt increased by S$179 million.

- 51% of the lease expiries in 1QFY24/25 came from China, which recorded a negative reversion rate of 11.3%.

In my opinion, the negative rental reversions in China will continue to be a drag to its portfolio in subsequent quarters. In terms of gross revenue, China market makes up 18.3%. The good news is that the manager is self-aware and kicked start its portfolio rejuvenation. If the Fed reduce interest rates in upcoming September, this will benefit Mapletree Logistics Trust in terms of lowering financial costs in the longer run.

We may not see positive results in the near term, but I am positive about Mapletree Logistics Trust in the longer term given that the management is not a sitting duck.

Last but not least, I am using Stocks Café to management my stocks in my portfolio. Read more about Stocks Cafe if you are interested.