I am currently fifty percent invested in stocks and REITs. Historically, I always like to check my cash I have on hand versus my stock investment. This is because one of the money management tip I learnt is to count your money because you cannot manage what you don’t know.

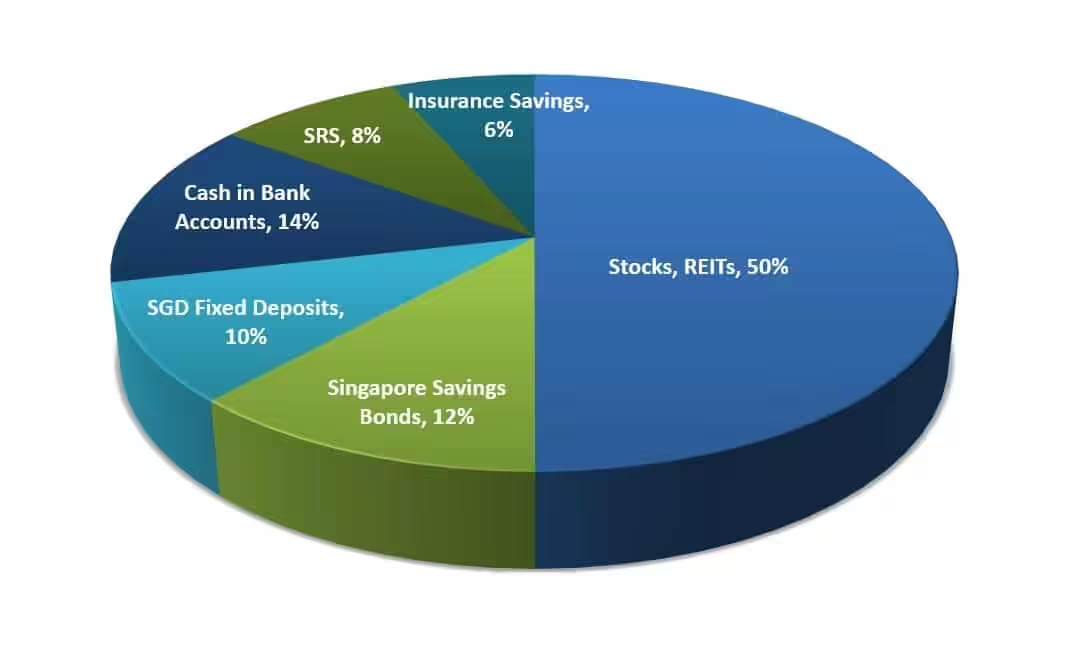

As you can see from the pie chart above, I am 50 percent invested in stocks and REITs, 12 percent in Singapore Savings Bonds, 10 percent in SGD Fixed Deposits and 6 percent in Insurance Savings Plans. I have 14 percent cash on hand and 8 percent contributed to Supplementary Retirement Scheme which is meant for my retirement.

The guidance I have for myself is to remain 70 percent invested and have 30 percent cash on hand. When I am 70 percent invested, this is where I felt my wallet gets tighter and uncomfortable to spend money on daily necessities. My comfortable ratio is 60 percent invested and 40 percent cash on hand.

So How Much Should You Invest?

My answer still remains the same as what I wrote in year 2020. There is actually no right or wrong answer on how much money should you keep on hand and how much money should you put into the stock market.

If you are an aggressive investor with higher risk appetite, you can have a higher ratio invested in the stock market. But if you cannot sleep well when you have less cash in your bank account, then you should allocate more cash in your bank account or put them into SGD Fixed Deposits as these are safer assets.

Why I Lock My Money in Supplementary Retirement Scheme (SRS) Account?

Many investors and friends I knew did not like to contribute their money to Supplementary Retirement Scheme (SRS) because of the low interest rate as compared to other financial instruments which provide higher returns.

For myself, I wanted to build a retirement account and I believe SRS is a good scheme to do so. Thus, I instilled a discipline to contribute money to my SRS account monthly. In fact, I have maxed out my SRS contribution this year.

I plan to withdraw the money from my SRS for the subsequent 10 years after my retirement age of 62.

By the way, you can purchase Singapore Savings Bonds using your monies in SRS for higher returns.