ESR-REIT 3Q2020 Financial Results have been released on 30th October 2020. The financial results are always in a sea of red. However, I will still continue to monitor this REIT as 100% of its portfolio is unencumbered.

Can the manager turn around the financial results of ESR-REIT? Let us take a look at ESR-REIT 3Q2020 financial results.

In 3Q2020, Gross Revenue and Net Property Income (“NPI”) fell 8.1% to S$56.9 million and 10.94% to S$40.4 million respectively.

Distribution per Unit (“DPU”) for 3Q2020 is 0.798 Singapore cents including the payment of S$3.5 million distributable income from 1Q2020 which was previously retained in view of

COVID-19 uncertainties.

ESR-REIT 3QFY20 Financial Results

| 3QFY20 (S$’000) |

3QFY19 (S$’000) |

YoY(%) | |

| Gross Revenue | 56,946 | 61,965 | (8.1)% |

| Net Property Income | 40,375 | 45,336 | (10.94)% |

| Distributable Amount | 28,276 | 33,824 | (16.40)% |

| Distribution Per Unit (“DPU”) (cents) | 0.798 | 1.000 | (20.2)% |

Occupancy

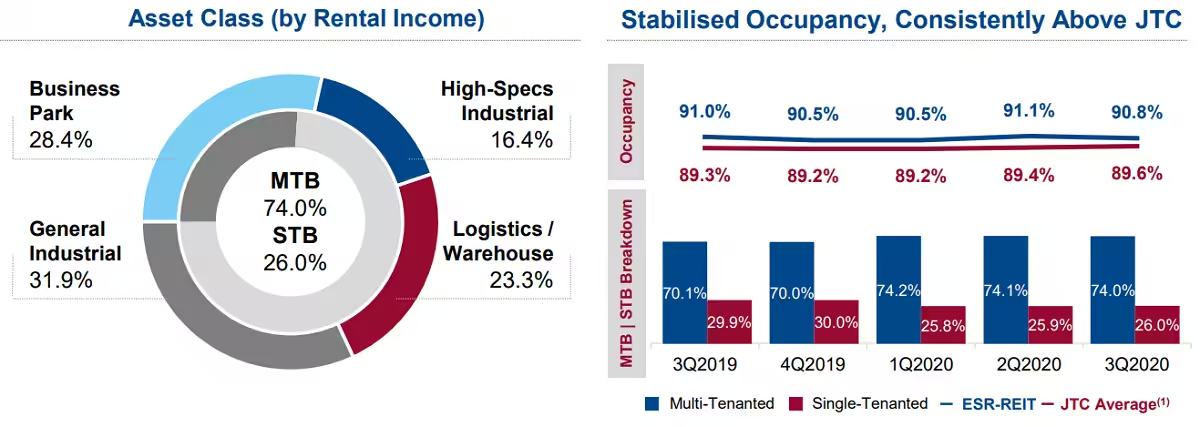

Portfolio occupancy stood at 90.8%. This was above JTC’s average of 89.6%. The tenant retention rate was 85.0%.

The Weighted Average Lease Expiry (WALE) was reduced to 3.0 years.

As highlighted previously, ESR-REIT is trying to convert single-tenanted into multi-tenancy. I guess there is still much work to be done as I do see single-tenant makes up 26% of the occupancy as shown in the bar chart below.

Debt

Gearing (Debt to Total Assets) stood at 41.6%. The gearing for industrial REITs are usually high above 40%. In my opinion, I do feel uncomfortable with the gearing of 41.6% in view of the poor economical outlook due to the COVID-19 pandemic.

Having said that, it was mentioned that all-in cost of debt reduced was to 3.5% p.a. I do hope to see more aggressive reduction of debt in the next quarter to below 40%.

On a positive note, there is also no debt refinancing requirements till June 2021.

As of 30th September 2020, the Weighted Average Debt Expiry was 2.5 years.

Current Dividend Yield

Based on FY19 full year dividend DPU of 4.011 cents and current share price of S$0.36, this translate to a current dividend yield of 11.14%.

It is unlikely ESR-REIT is able to maintain the same DPU payout of 4.011 cents in FY20. Year to Date (“YTD”) 9M2020, only 1.960 cents had been paid as compared to 3.011 cents a year ago.

If we estimate 2.66 cents (0.70 cents in Q4) to be paid in FY20, this will translate to an estimated dividend yield of 7.39% for FY20.

Summary

ESR-REIT is worth taking a look as 100% of its portfolio remains unencumbered.

External demand conditions and the softening labour market will pose a drag on economic recovery. The ongoing US-China trade standoff has also disrupted the recovery pace.

Despite signs of gradual stabilisation, the industrial outlook remains uncertain with pressures from the staggered openings of international borders and potential resurgence of COVID-19 in some countries having impeded global trade and production volumes.

Industrial property rents and prices continue to slide in 3Q2020. In addition, the delay in construction of industrial space is expected to push new-supply completion into 2021.

Industrial rents are expected to remain muted due to pandemic pressures and current weak trade conditions which prevent industrialists from committing to long term space needs while local industrialists are looking at short-term expansion to meet stockpiling requirements.

With more negative factors as compared to the positives, it is no wonder ESR-REIT is facing headwinds. The manager might need to do more to turn the financial results around.

The very last thing is that you may have heard about the proposed merger with Sabana REIT which will form an enlarge REIT. This is expected to be NAV and DPU accreditive to ESR-REIT unit holders.

If you decided to invest into ESR-REIT, this is probably a recovery play and be prepared to hold long term until value emerges.