TSMC 2Q26 Earnings arrived at a time when global semiconductor demand continues to surge, yet the market reaction to the results was unexpectedly cautious. Despite the strength of the TSMC 2Q26 Earnings report, the TSMC share price fell 8.20 percent over the five trading days surrounding the announcement, closing at 398.37 USD on 17 July 2026. For investors who closely monitor the taiwan semiconductor manufacturing share price or track TSMC share price NYSE movements, this decline stood in contrast to the company’s impressive financial performance.

The market’s reaction highlights a recurring theme in semiconductor investing: strong fundamentals do not always translate into immediate share price gains. In the case of TSMC 2Q26 Earnings, the company delivered substantial year-over-year and quarter-over-quarter growth across revenue, net income, and margins. Yet broader market sentiment, valuation concerns, and profit-taking appear to have overshadowed the positive results.

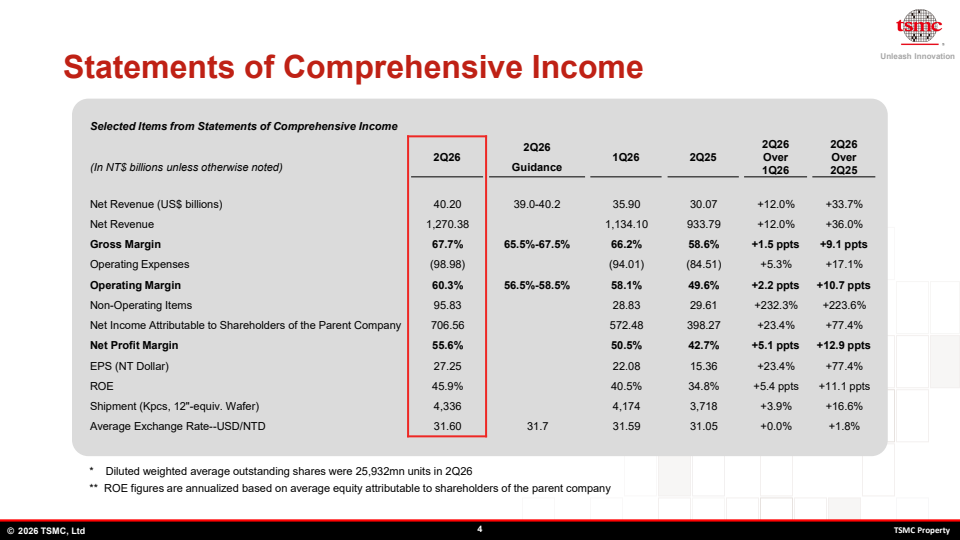

TSMC 2Q26 Earnings reported consolidated revenue of NT$1,270.38 billion, net income of NT$706.56 billion, and diluted EPS of NT$27.25. These figures reflect the company’s continued leadership in advanced semiconductor manufacturing and its ability to scale cutting-edge technologies at a pace unmatched by competitors.

Revenue Growth Driven by Advanced Technologies

One of the most notable aspects of TSMC 2Q26 Earnings is the strength of its advanced technology portfolio. In US dollar terms, revenue reached 40.20 billion, marking a 33.7 percent increase year-over-year and a 12 percent increase from the previous quarter. This growth was driven primarily by the company’s leading-edge nodes, which continue to dominate its revenue mix.

The 3nm and 5nm families remained the core contributors to TSMC 2Q26 Earnings. Together, they accounted for more than 60 percent of total wafer revenue. The early ramp of 2nm technology added another layer of momentum, contributing 3 percent of wafer revenue in its initial phase. Meanwhile, 7nm contributed 11 percent, reinforcing TSMC’s dominance in advanced semiconductor production.

This revenue mix reflects the global shift toward AI-centric and performance-intensive computing. As cloud providers, device manufacturers, and AI developers push for higher efficiency and processing power, TSMC’s advanced nodes remain central to the industry’s evolution. The company’s ability to scale these technologies ahead of competitors continues to be a defining advantage, and TSMC 2Q26 Earnings demonstrate that this leadership position remains intact.

Profitability Strengthens Across All Metrics

TSMC 2Q26 Earnings also showcased exceptional profitability. Gross margin reached 67.7 percent, operating margin climbed to 60.3 percent, and net profit margin expanded to 55.6 percent. These figures highlight the company’s ability to maintain high efficiency even as it invests heavily in next-generation technologies.

Net income rose to NT$706.56 billion, a 77.4 percent increase compared to 2Q25 and a 23.4 percent increase from the previous quarter. Diluted earnings per share reached NT$27.25, reflecting strong operating leverage and disciplined cost management. TSMC 2Q26 Earnings reinforce the company’s reputation as one of the most profitable semiconductor manufacturers globally.

Even with rising capital expenditures associated with 2nm and future nodes, TSMC continues to deliver strong returns. The company’s ability to balance investment-heavy growth with margin expansion is a key reason why long-term investors remain confident in its trajectory.

Platform Performance: HPC and Smartphone Lead Growth

A deeper look into TSMC 2Q26 Earnings reveals where demand was strongest. High performance computing (HPC) posted a remarkable 66 percent quarter-over-quarter increase, driven by AI accelerators, data center processors, and advanced compute architectures. This segment has become the backbone of TSMC’s growth, reflecting global investment in AI infrastructure and cloud computing.

Smartphone revenue also saw a healthy 22 percent sequential increase. With flagship device launches and rising silicon content per device, smartphone manufacturers continue to rely heavily on TSMC’s advanced nodes. The combination of performance, efficiency, and integration offered by 3nm and 5nm technologies remains a key differentiator.

Other segments such as IoT, automotive, and digital consumer electronics posted modest growth. While these areas are important for diversification, the clear momentum remains in HPC and premium mobile platforms. TSMC 2Q26 Earnings align with broader industry trends where AI and advanced mobile computing drive the majority of semiconductor innovation.

Balance Sheet Strength and Cash Flow Resilience

TSMC 2Q26 Earnings also highlight the company’s exceptional balance sheet strength. Cash and marketable securities increased to NT$3,518.01 billion, providing ample liquidity for future investments. Total assets reached NT$9,375.65 billion, reflecting ongoing expansion in manufacturing capacity and technology development.

Operating cash flow for the quarter came in at NT$783.36 billion, while capital expenditures totaled NT$496.00 billion. Free cash flow reached NT$287.36 billion, demonstrating the company’s ability to fund growth initiatives while maintaining financial flexibility. TSMC 2Q26 Earnings show that the company remains well-positioned to support future node development, global expansion, and strategic partnerships.

The company’s continued investment in advanced nodes, including the steep ramp-up of 2nm technology, underscores its commitment to staying ahead of global demand. These investments are capital-intensive but essential for maintaining leadership in a rapidly evolving industry.

3Q26 Guidance: Continued Momentum Expected

Looking ahead, TSMC expects strong performance in the third quarter of 2026. TSMC 2Q26 Earnings guidance forecasts revenue between 44.6 billion and 45.8 billion USD, supported by ongoing demand for leading-edge technologies. Gross margin is expected to remain between 65 and 67 percent, while operating margin is projected to fall between 56 and 58 percent.

The company anticipates continued strength in HPC and smartphone demand, along with accelerating adoption of 2nm technology. TSMC 2Q26 Earnings reinforce the view that fundamentals remain solid despite recent volatility in the taiwan semiconductor manufacturing share price.

Why the Share Price Fell Despite Strong Results

The decline in the TSMC share price following the earnings release may seem counterintuitive, but several factors likely contributed. Semiconductor stocks often react not only to current results but also to expectations for future growth, valuation concerns, and broader market sentiment. With TSMC’s shares having rallied significantly earlier in the year, some investors may have taken profits ahead of the earnings announcement.

Additionally, concerns around supply chain normalization, geopolitical risks, and competitive dynamics may have weighed on sentiment. The taiwan semiconductor manufacturing share price has been sensitive to global macroeconomic conditions, and TSMC 2Q26 Earnings were released during a period of heightened market caution.

It is also possible that investors expected even stronger guidance or more aggressive expansion plans. When expectations are high, even strong results can lead to a temporary pullback. For long-term investors tracking TSMC share price NYSE trends, such volatility is not unusual in high-growth technology sectors.

Strong Fundamentals Amid Market Volatility

TSMC 2Q26 Earnings highlight exceptional execution, strong demand for advanced nodes, and industry-leading profitability. While the TSMC share price experienced a temporary pullback, the company’s financial strength and strategic positioning continue to reinforce its long-term investment appeal.

With 2nm ramping up, HPC demand accelerating, and margins expanding, TSMC remains at the forefront of global semiconductor innovation. TSMC 2Q26 Earnings indicate that the recent share price decline may represent a period of consolidation rather than a reflection of weakening fundamentals.

Summary of TSMC 2Q2026 Earnings

- Revenue: NT$1,270.38 billion

- Net income: NT$706.56 billion

- EPS: NT$27.25

- Gross margin: 67.7 percent

- Operating margin: 60.3 percent

- Net profit margin: 55.6 percent

- Advanced technologies: 77 percent of wafer revenue

- 2nm contribution: 3 percent of wafer revenue

- 3nm contribution: 30 percent of wafer revenue

- 5nm contribution: 33 percent of wafer revenue

- Free cash flow: NT$287.36 billion

- 3Q26 revenue guidance: 44.6 to 45.8 billion USD