On 28th July 2022, Starhill Global REIT released their 2H FY21/22 Financial Results. A Distribution Per Unit (DPU) of 2.02 cents was announced which will be payable on 23rd September 2022.

The portfolio comprises of 10 mid-to high-end retail and commercial properties in six cities across the Asia Pacific.

Starhill Global REIT makes up 9% of my wife’s stock portfolio. How did Starhill Global REIT perform?

Let us take a look at its 2H FY21/22 financial results in more details below.

Starhill Global REIT 2H FY21/22 Financial Results

In 2H FY21/22, Net Property Income (NPI) rose 7.6% y-o-y to S$75.1 million largely due to the cessation of rental rebates in Malaysia and the completion of asset enhancement works at The Starhill, as well as lower expenses for the Group.

This was partially offset by the lower rental contribution from Wisma Atria Property (Retail) and the depreciation of the Australian dollar against the Singapore dollar.

Income available for distribution for 2H FY21/22 was up 4.9% y-o-y mainly due to higher NPI, as well as lower finance costs and other non-property items, partially offset by lower management fees paid/payable in units.

| 2H FY21/22 (S$’mil) |

2H FY20/21 (S$’mil) |

Change (%) | |

| Gross Revenue | 95.5 | 92.9 | 2.8% |

| Net Property Income | 75.1 | 69.8 | 7.6% |

| Distributable Income | 47.1 | 44.9 | 4.9% |

| Distribution Per Unit (“DPU”) (cents) (excluding effects of deferred amount) | 2.02 | 1.86 | 8.6% |

| Distribution Per Unit (“DPU”) (cents) (including effects of deferred amount) | 2.02 | 2.07 | (2.4%) |

If we exclude the deferred amount that was distributed in 2H FY20/21, the Distribution Per Unit (DPU) for 2H FY21/22 was 8.6% higher y-o-y at 2.02 cents.

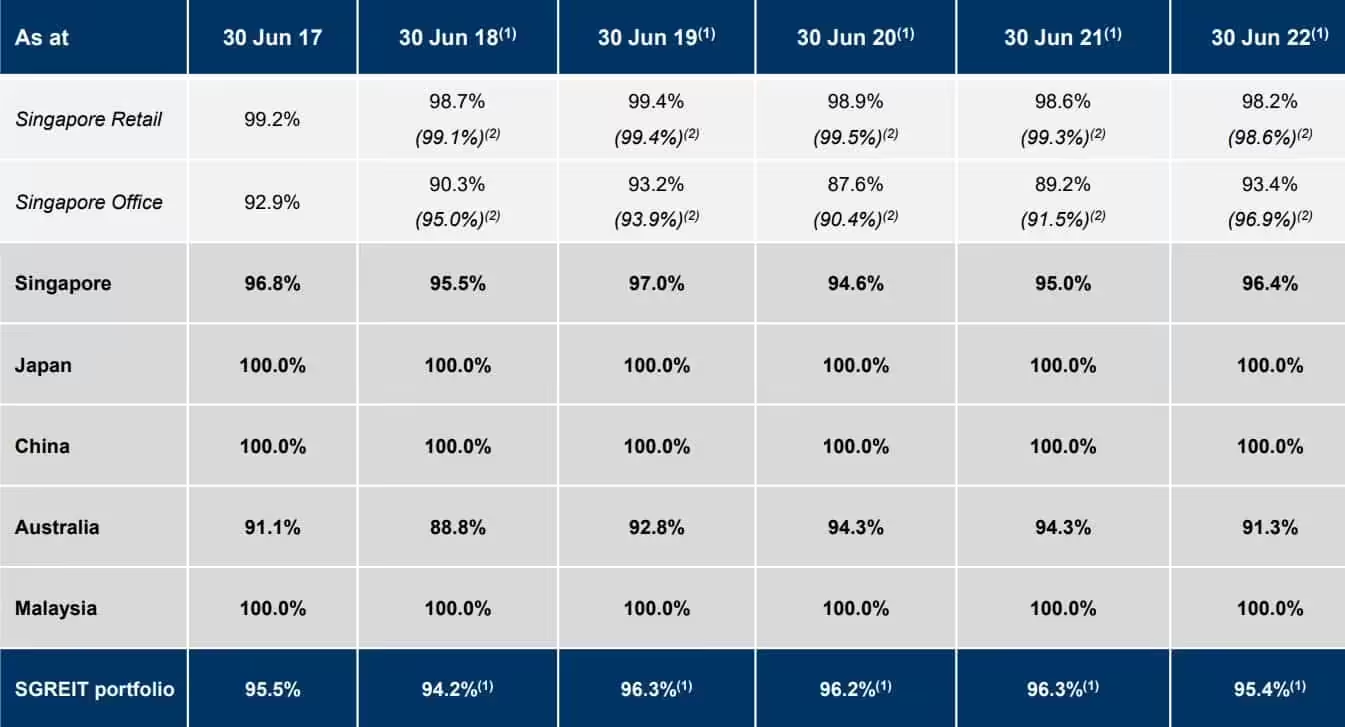

Occupancy

Overall portfolio occupancy stood at healthy at 95.4%.

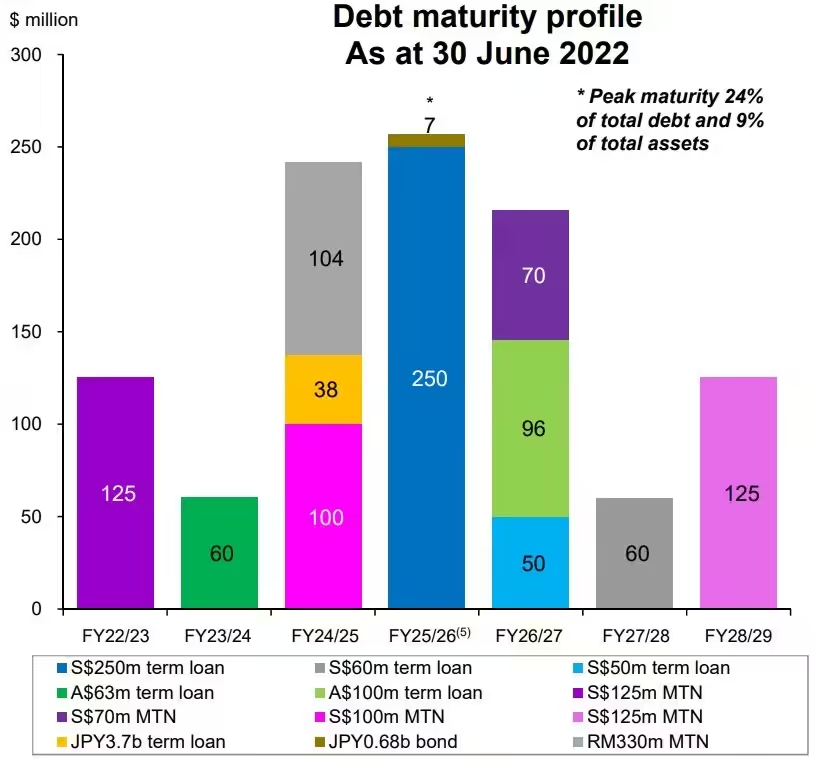

Debt

As of 30 June 2022, gearing ratio is healthy at 36.2%. Weighted Average Debt Maturity (WALE) stood at 3.5 years.

About 93% of the borrowings are fixed/hedged to mitigate against interest rates fluctuations. No refinancing requirement is required until May 2023.

Starhill Global REIT is rated “BBB” credit rating with stable outlook by Fitch Ratings.

Current Dividend Yield

The full year Distribution Per Unit (DPU) for FY21/22 was 3.80 cents. Based on the current share price of S$0.58, this translate to an attractive current dividend yield of 6.55%.

Summary of Starhill Global REIT 2H FY21/22 Financial Results

The positives are

- Net Property Income (NPI) rose 7.6% y-o-y to S$75.1 million.

- Income available for distribution for 2H FY21/22 was up 4.9% y-o-y mainly due to higher NPI.

- Distribution Per Unit (DPU) for 2H FY21/22 was 8.6% higher y-o-y at 2.02 cents.

- Overall portfolio occupancy stood at healthy at 95.4%.

- Gearing ratio is healthy at 36.2%.

- 93% of the borrowings are fixed/hedged.

- No refinancing requirement is required until May 2023.

- “BBB” credit rating with stable outlook by Fitch Ratings.

- Attractive current dividend yield of 6.55%.

The negatives are

- Lower rental contribution from Wisma Atria Property (Retail).

- Depreciation of the Australian dollar against the Singapore dollar.

I am happy to know there are more positives as compared to negatives.

Many years after I added Starhill Global REIT into my wife’s stock portfolio, the REIT now has a more diversified assets.

With the continued rejuvenation (Asset Enhancements) of the shopping malls, I believe Starhill Global REIT will do well. For example, Wisma Atria is undergoing rejuvenation works. The Main retail area works are on schedule for completion in December 2022 which is the month of Christmas. This will attract more shoppers.